9. Matters Requiring a

Determination of Committee

Item: 9.1

Financial Management Review Update

|

Author/s

|

Beth O'Callaghan

|

Manager Financial Services

|

|

Authorisor/s

|

Shane Burge

|

Director Corporate Resources

|

File Ref: D18/22533

Applicant

Internal

Location/Address

Corporate Resources

Executive Summary

To advise the Audit Committee with an update of actions

implemented in response to the recommendations from Butler Settineri’s

Financial Management Review of the Shire’s policies, procedures and

practices.

Recommendation in Brief

That the Audit Committee receives the report providing an

update on actions implemented in response to Butler Settineri’s Financial

Management Review of the Shire’s policies, procedures and practices.

Background

In April 2016 Butler Settineri were engaged by the Shire to

perform a review of the policies, procedures and practices of the Shire of

Esperance. Their report received in June 2016 provided recommendations

for the Shire to implement.

At the request of the Audit Committee a report was presented

to them in November 2016 of the actions that will be implemented in response to

the recommendations.

The purpose of this report is to provide an update on the

implemented recommendations.

Officer’s Comment

Two years ago a report was presented to the Audit Committee

with the actions that will be implemented in response to Butler

Settineri’s review of the policies, procedures and practices of the Shire

of Esperance.

Attached is the same report with another column headed as

“November 2018 Update” in which a comment has been made for each

recommendation.

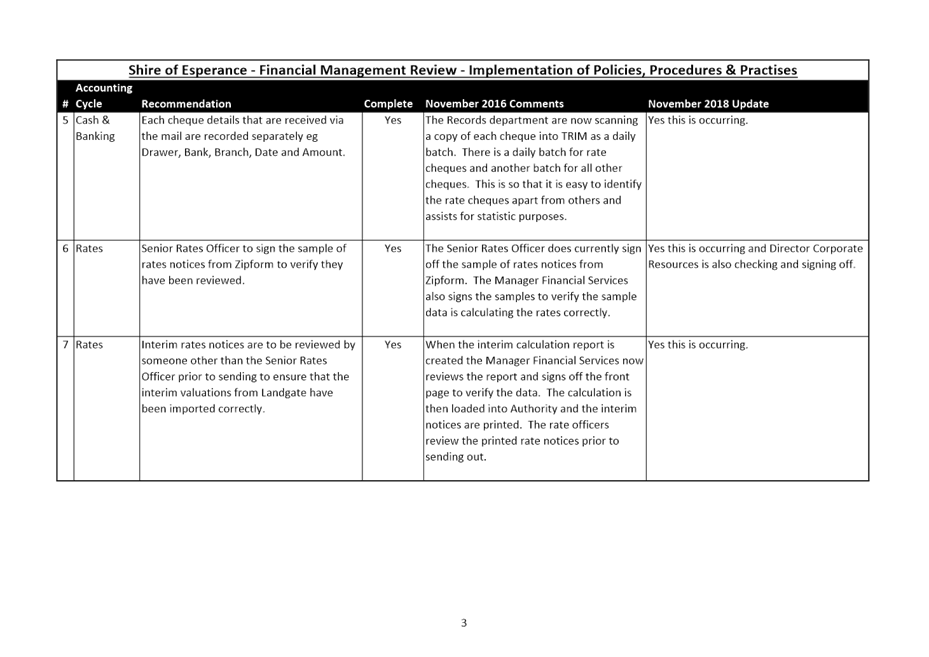

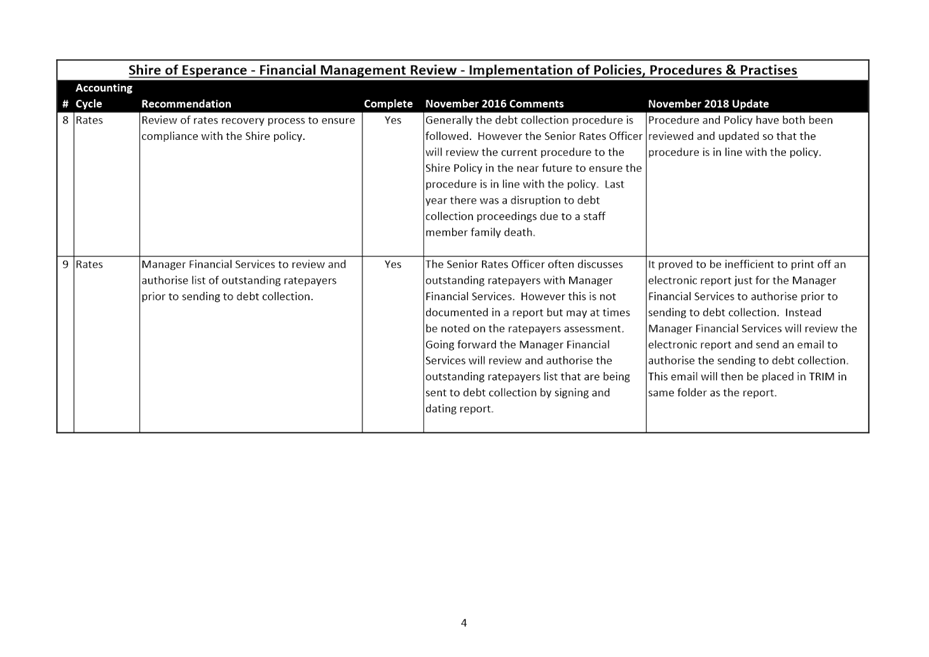

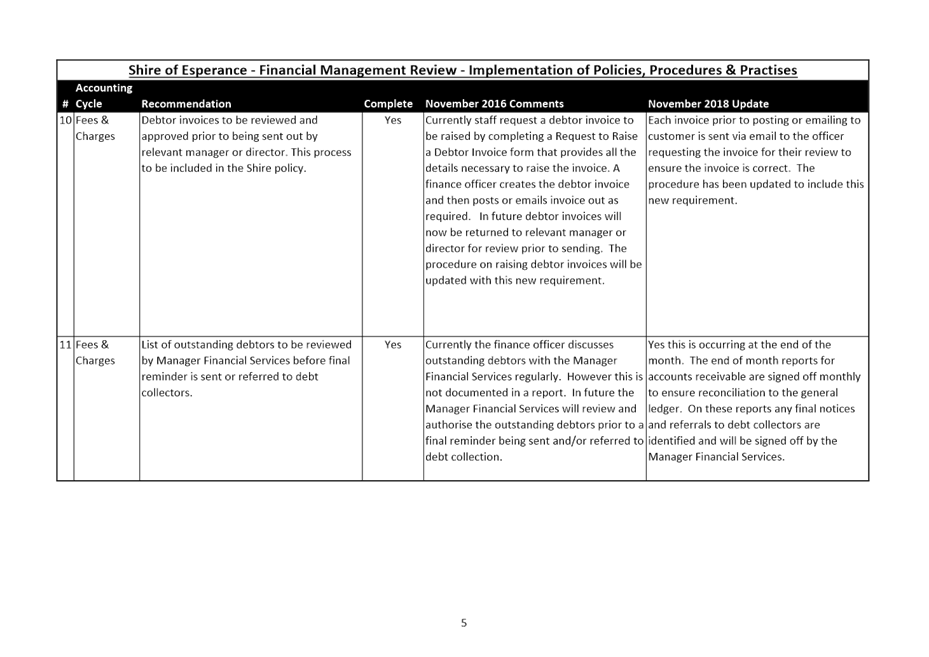

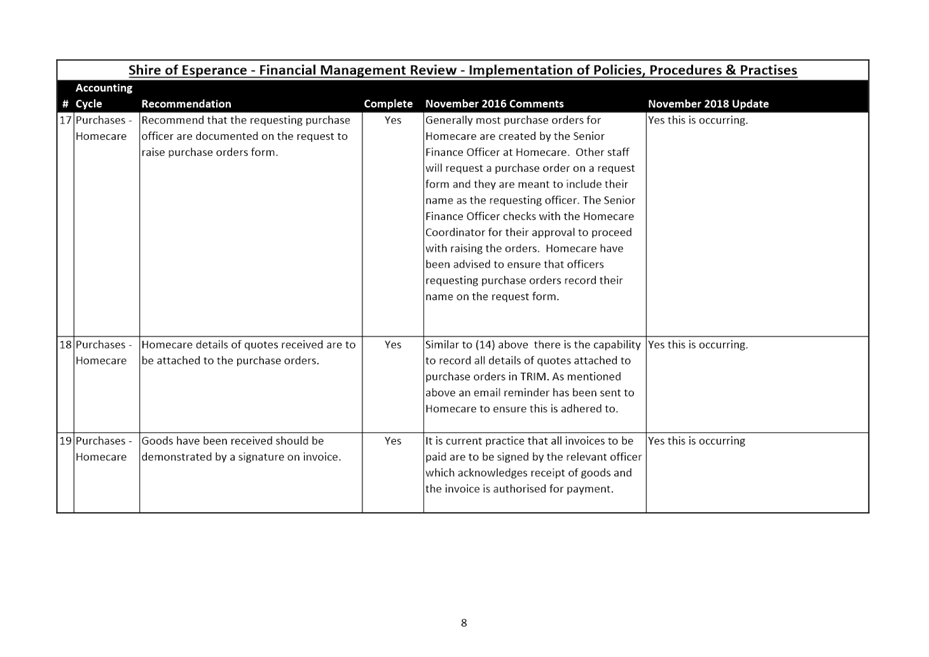

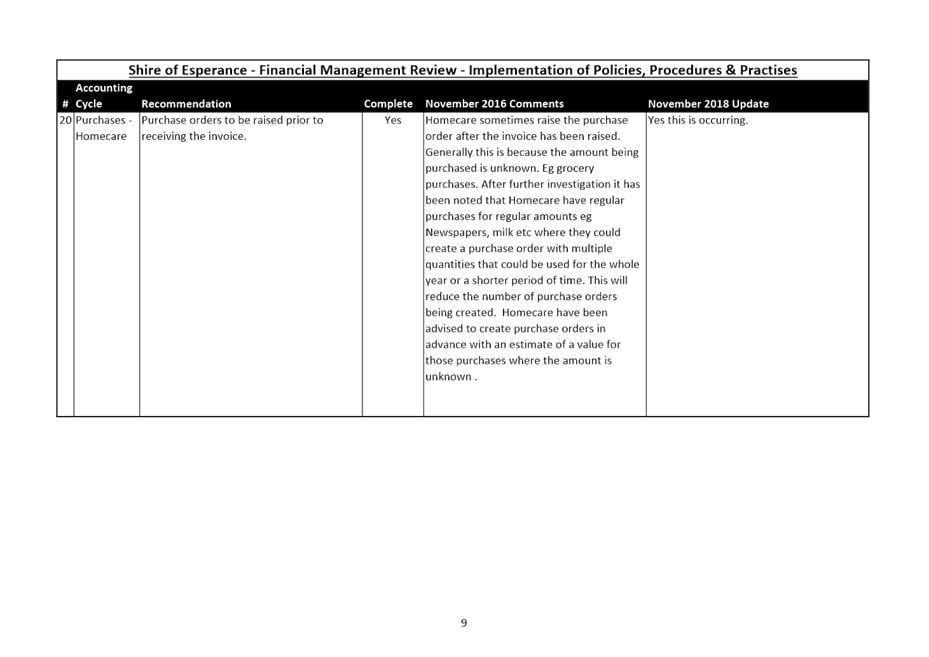

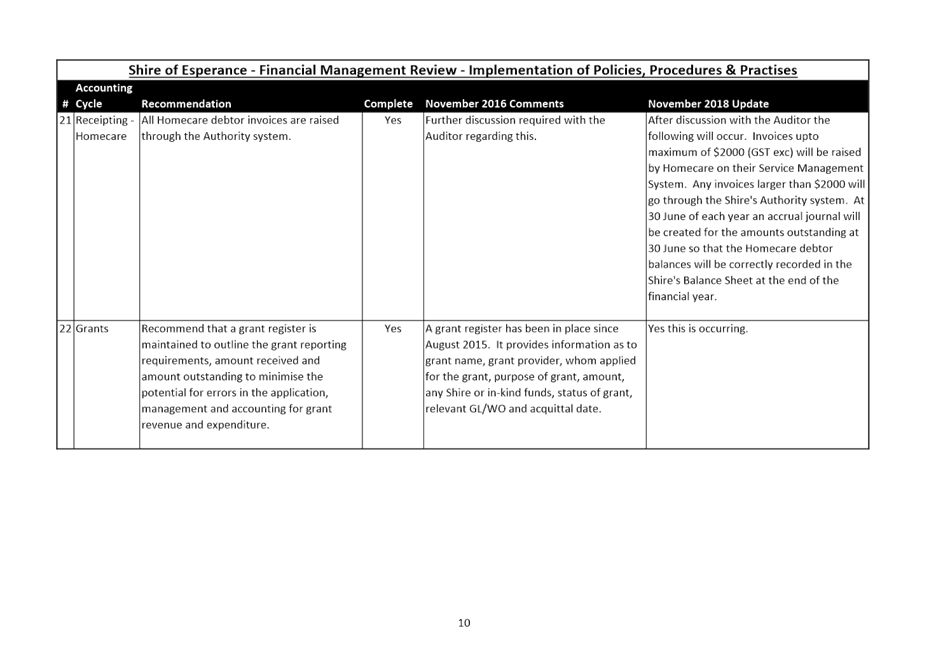

There were 7 accounting cycles addressed by Butler

Settineri. They are

· Cash and Banking

· Rates

· Fees and Charges

· Purchases and Expenses

· Payroll

· Homecare

· Grants

Generally speaking most of the actions have been successfully

implemented and have been continually actioned.

However the following have not been fully implemented or

require periodical staff reminders:

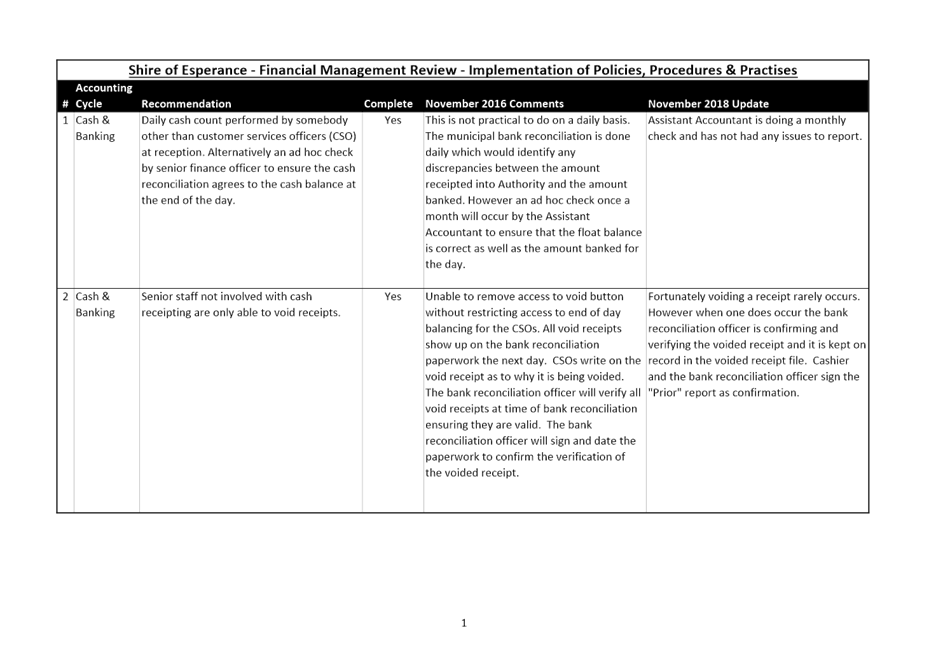

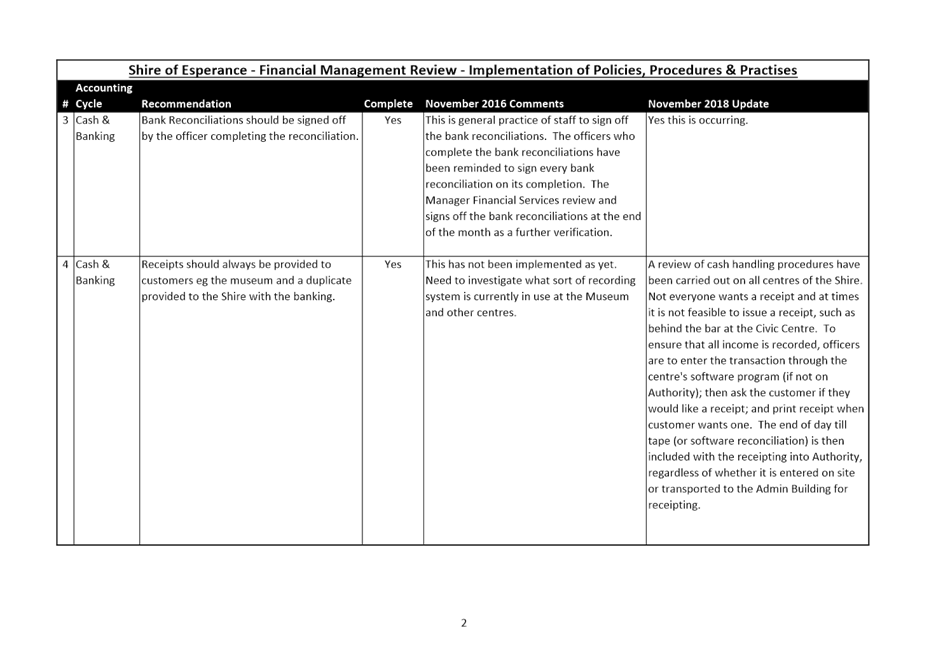

Cash and Banking

Since the last report to Council a review of the cash

handling procedures has been carried out on all areas of the Shire. This

includes Administration Building, Leisure Centre, Civic Centre, Visitor Centre,

Volunteer Centre, Homecare, Museum, Library, Wylie Bay and Caravan Park.

All areas have good cash handling procedures that took into account daily

reconciliations, security of cash and separation of duties where

possible.

One of Butler Settineri’s recommendations is that every

transaction should have a receipt provided to the customer. In some

centres this is done; other centres will offer a receipt; and one centre only

provides receipts on request from the customer.

In reality many customers do not want a receipt and to print

one is a waste of paper and time. However, it is important that every

receipt of cash is recorded and put through the register or computer software

of the centre. As a compromise it the procedure for all centres is that all

transactions are entered into the register and/or software program, then the

customer is asked if they would like a receipt. This way the transaction

is recorded and receipt is only printed when customer says yes.

Refer to the “November 2018 Update” column for

point 4 of the attachment for the comment regarding this.

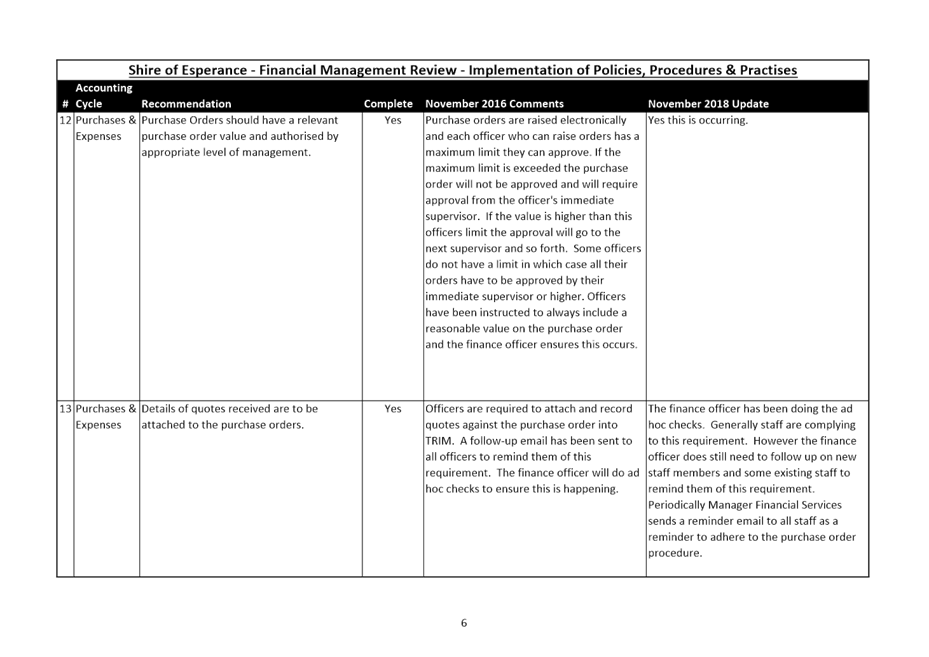

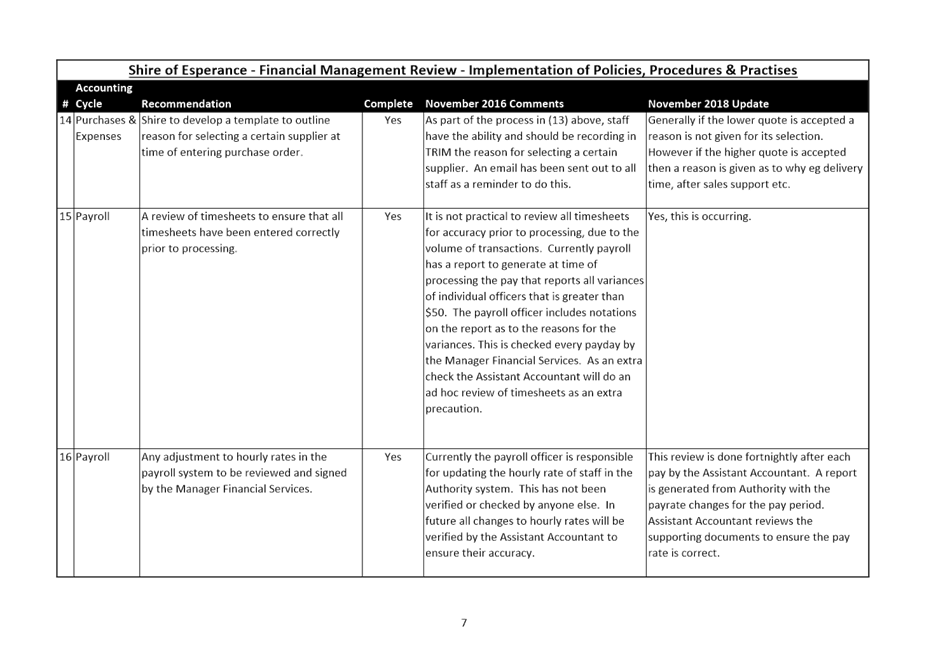

Purchases and Expenses

Raising of purchase orders and providing/recording quotes by

all staff is generally done well. However, the periodical email reminder

to all staff to do so assists with this good practice. Additionally, when

an officer chooses between two quotes a reason as why one is chosen over the

other is to be recorded. Generally, officers are not providing a reason

if the cheapest quote is chosen, however when the higher quote is accepted a

reason is provided as to why. This could be a number of reasons eg after

sales support, timeframe for the goods to arrive, availability etc.

Consultation

Nil

Financial Implications

Nil

Asset Management Implications

Nil

Statutory Implications

Local Government (Financial Management) Regulation

1996 5(2)

Policy Implications

Nil

Strategic Implications

Strategic Community Plan 2017 - 2027

Community

Leadership

A financially

sustainable and supportive organisation achieving operational excellence

Corporate Business Plan 2017/2018

– 2020/2021

Provide

responsible resource and planning management for now and the future

Environmental Considerations

Nil

Attachments

|

a⇩.

|

Financial Management

Review Implementation 2018

|

|

|

Officer’s

Recommendation

That the Audit Committee receive the report providing an

update on actions implemented in response to Butler Settineri’s

Financial Management Review of the Shire’s policies, procedures and

practices.

Voting Requirement Simple Majority

|

Item: 9.2

Audit Report 2017/18

|

Author/s

|

Beth O'Callaghan

|

Manager Financial Services

|

|

Authorisor/s

|

Shane Burge

|

Director Corporate Resources

|

File Ref: D18/26177

Applicant

Corporate Resources

Location/Address

Internal

Executive Summary

To present to the Audit Committee the 2017/18 audit report

and management letter prepared by the Council’s Auditor, Mr Marius Van

Der Merwe from Butler Settineri.

Recommendation in Brief

That the Audit Committee

1. Receive the

2017/18 Annual Financial Report incorporating the Audit Report as attached at

Attachment A.

2. Receive the

Management Letter for the 2017/18 financial year as attached at Attachment B.

3. Recommends

the Annual Financial Report, Audit Report and Management Letter for the 2017/18

financial year to Council for adoption.

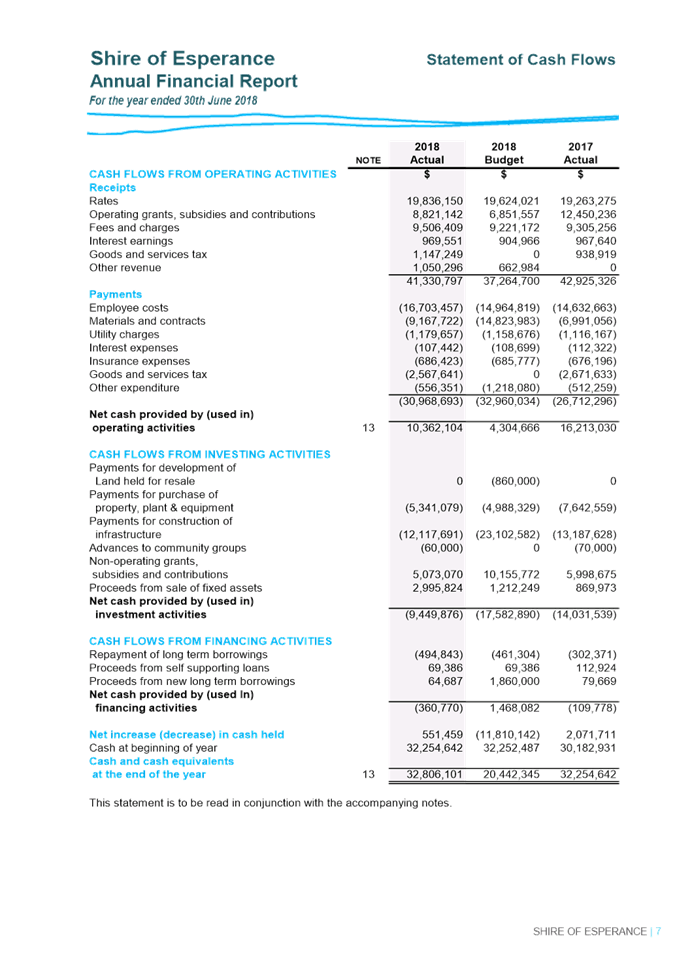

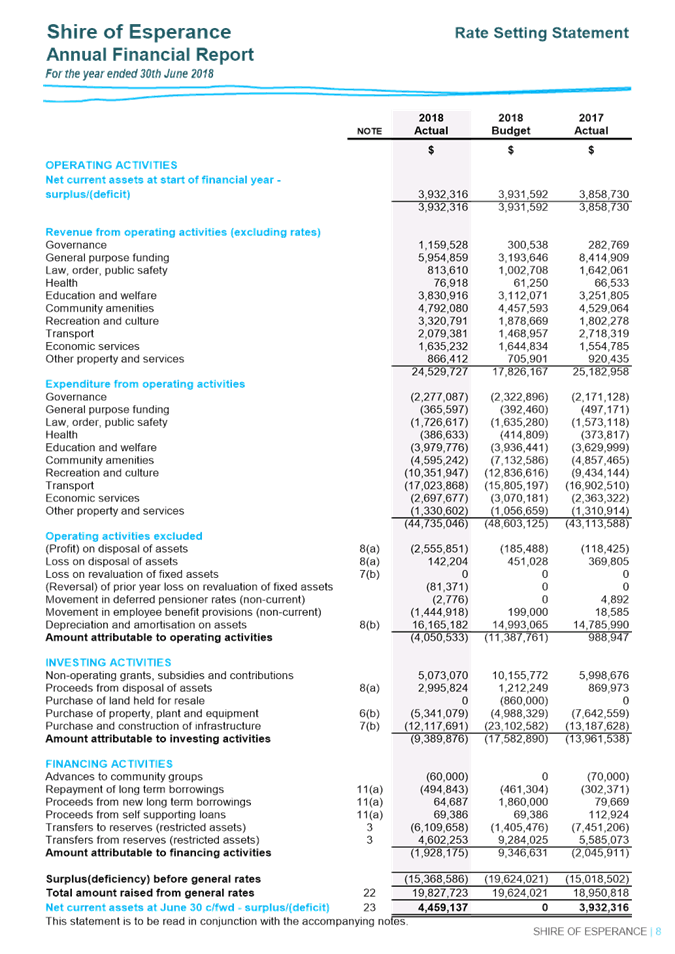

Background

Council is required to prepare a financial report and present

it to Council’s Auditor by 30 September each year. This has been

completed and the Audit Report, Management Letter and Annual Financial Report

are presented at Attachment A and B.

The Local Government Act (1995) requires that the

audit report and any management letter be examined by the local government to

determine if any matters raised in the report(s) require action to be

taken. After considering the audit report the local government is to

prepare a report on any actions to be taken in response to the audit report and

is to forward a copy of that report to the Minister for Local Government.

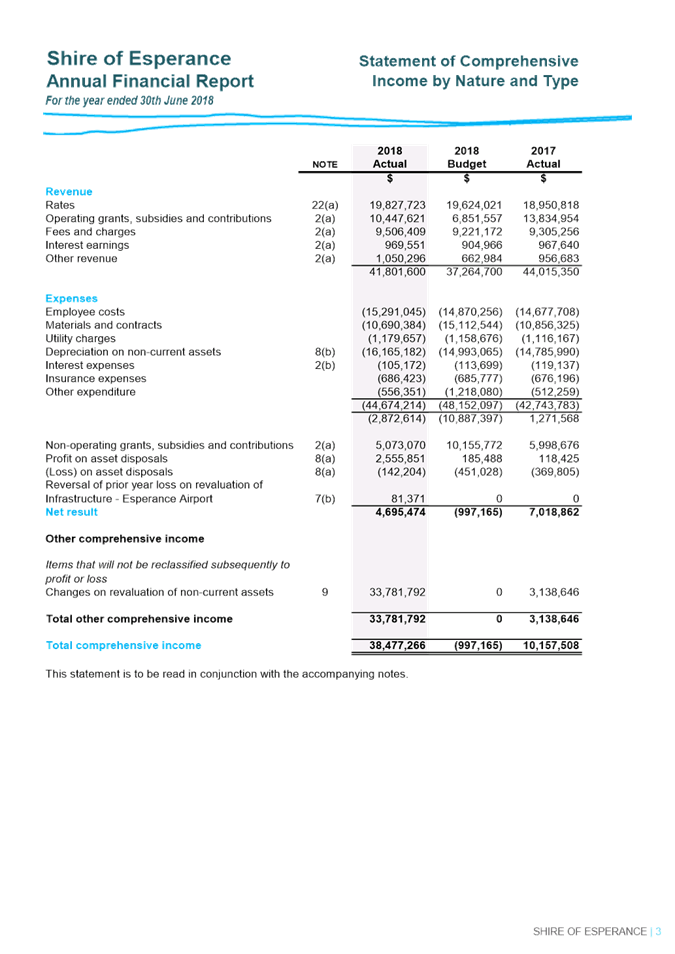

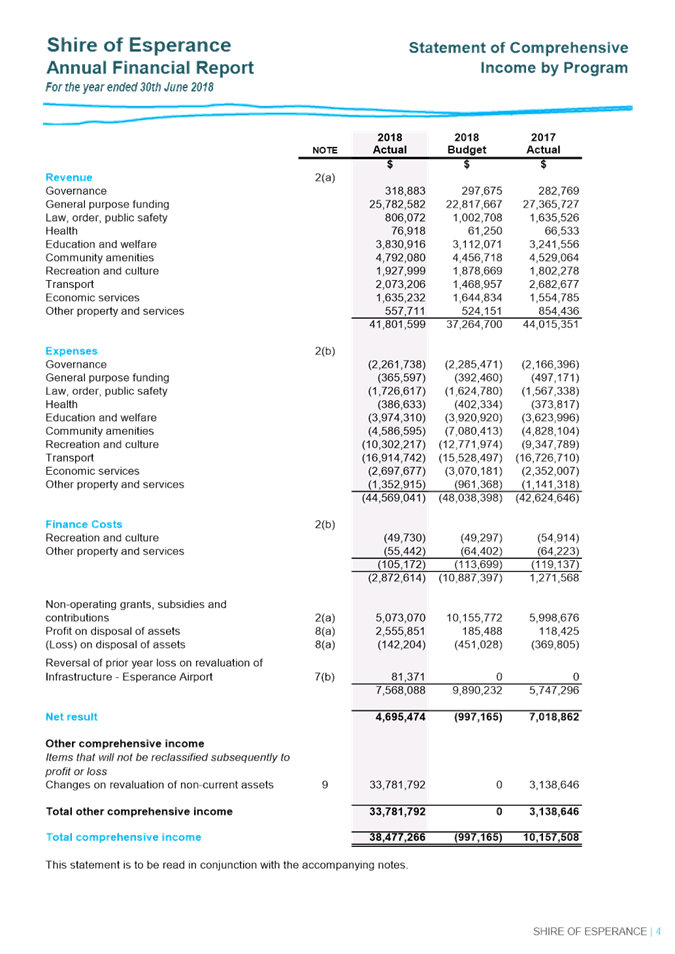

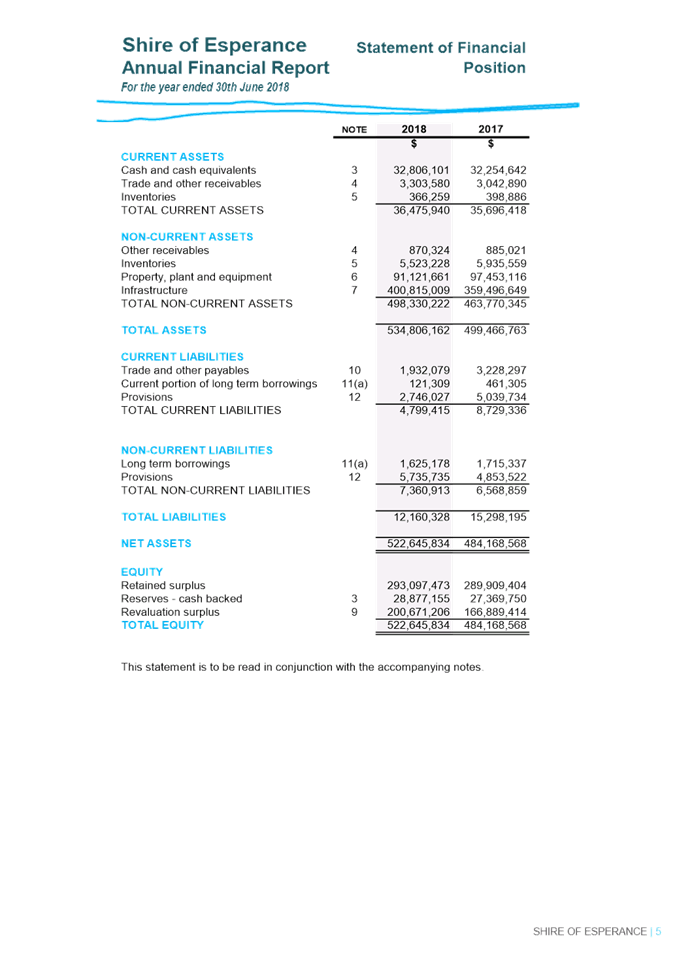

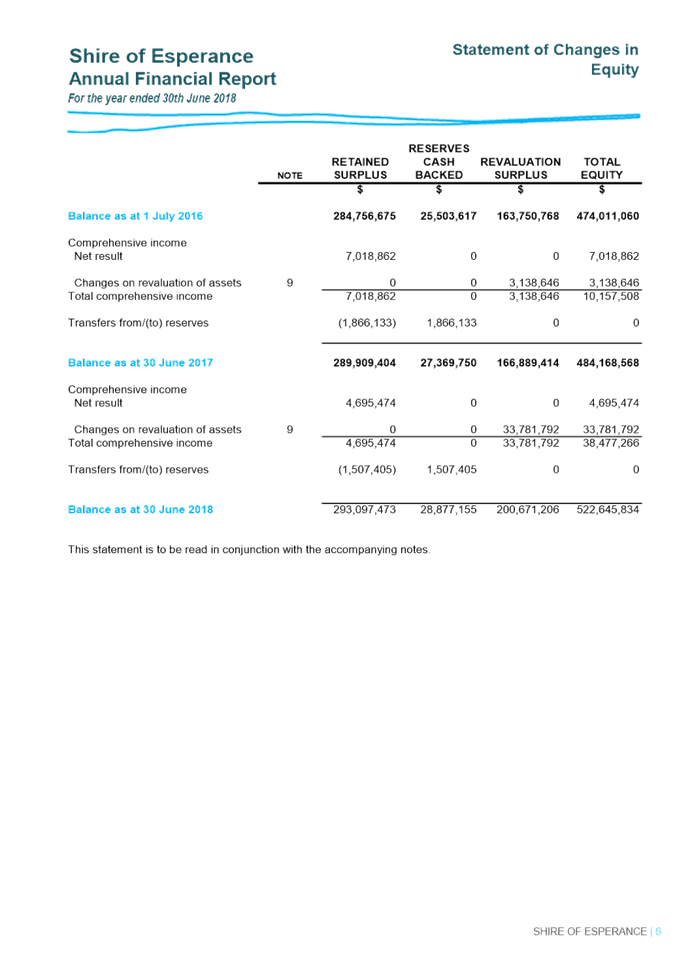

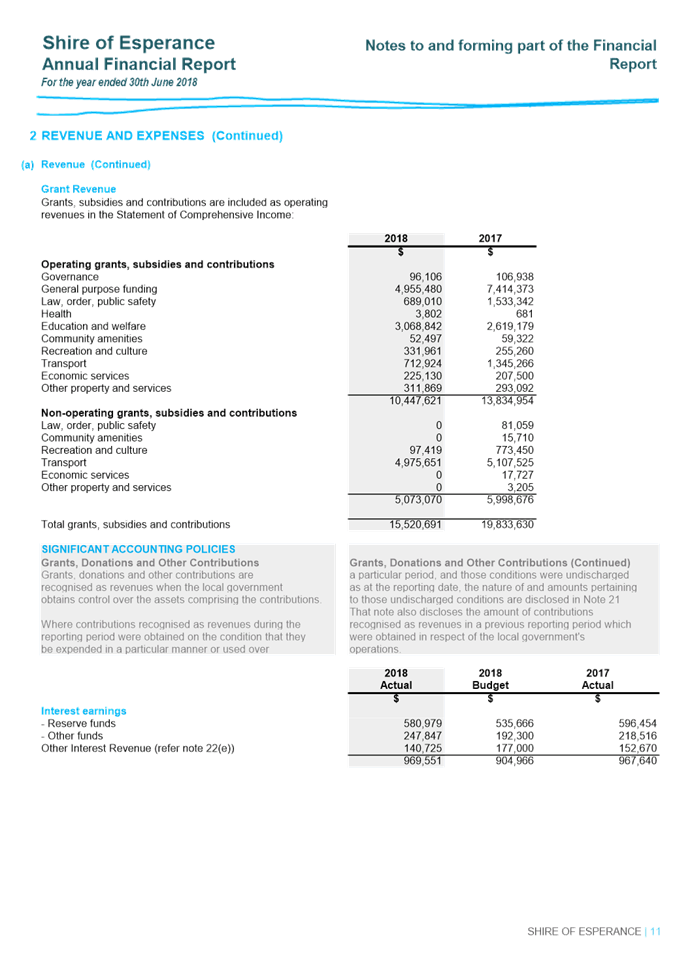

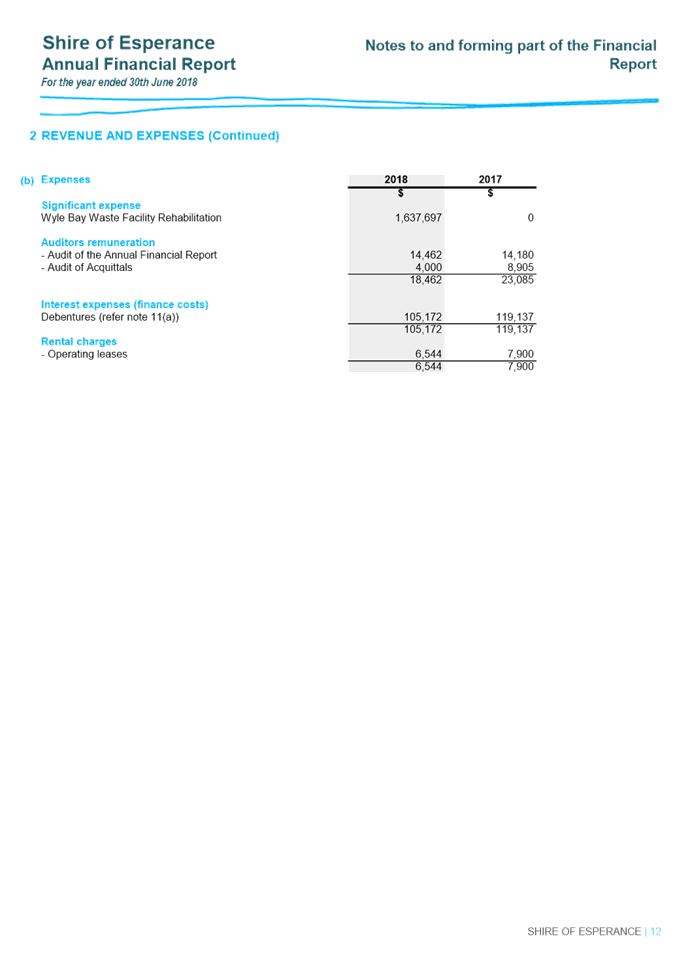

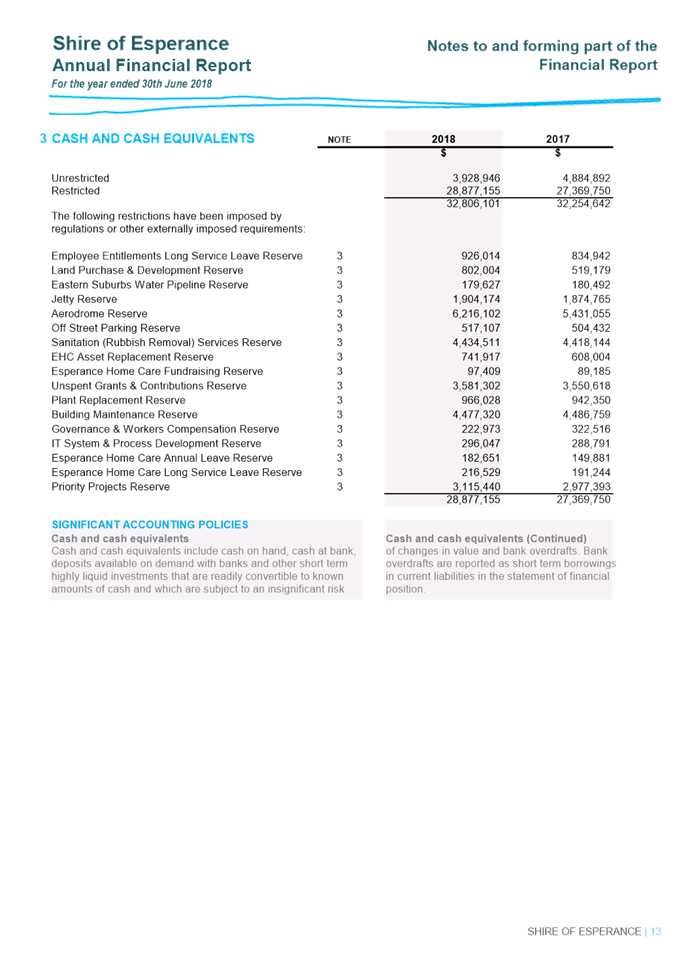

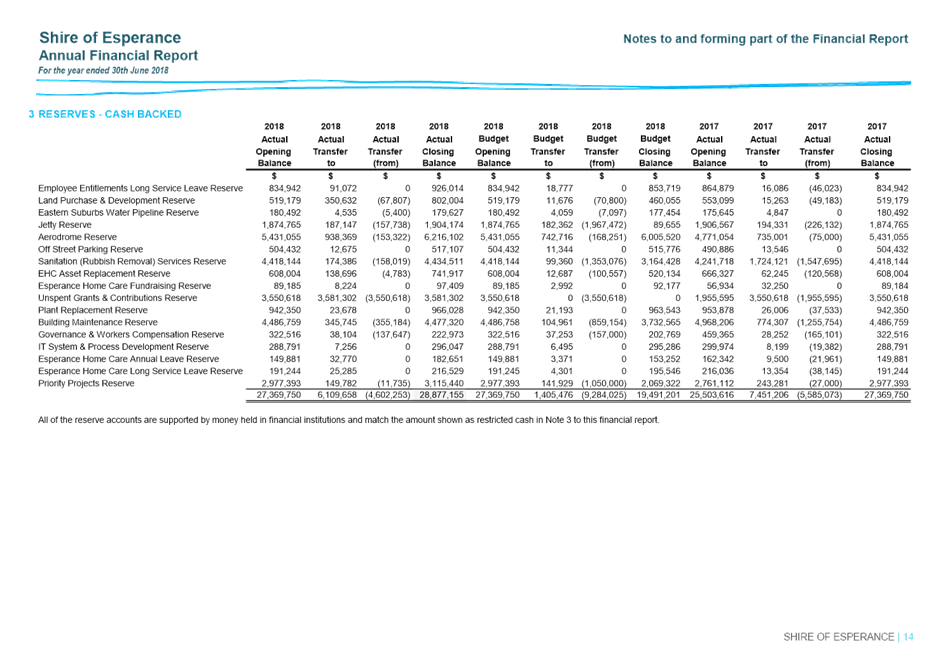

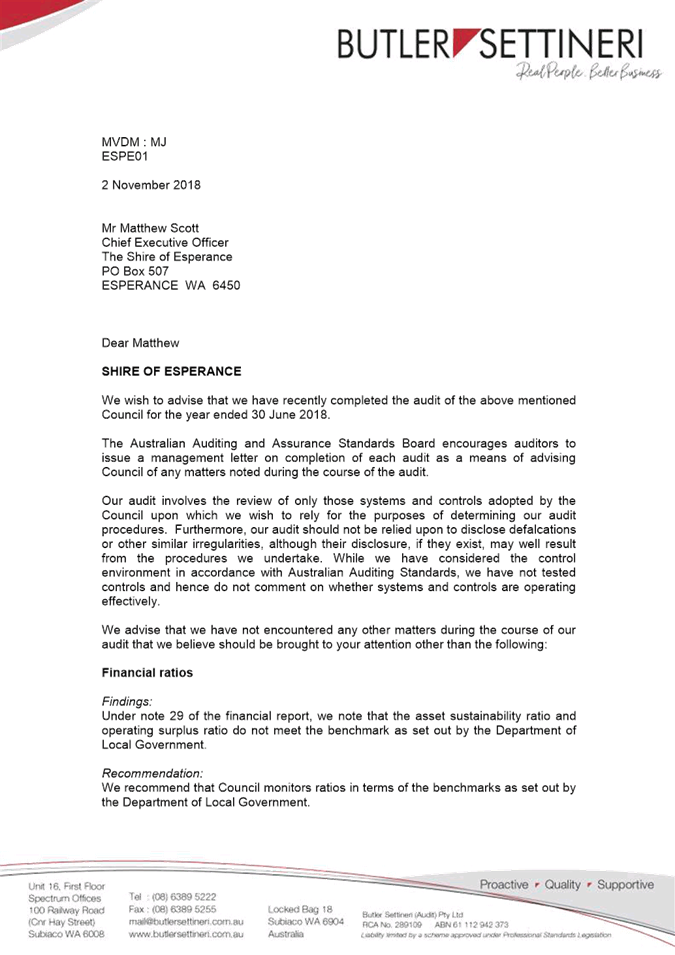

Officer’s Comment

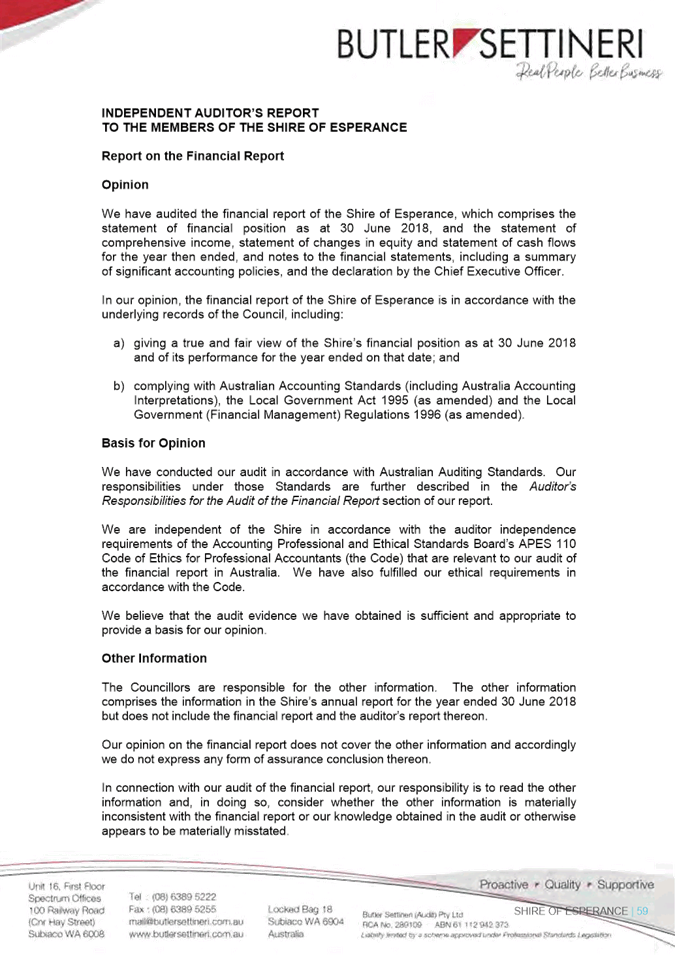

The Council has received an unqualified or

“clean” audit report from Mr Van Der Merwe. The auditors

opinion states that “In our opinion, the financial report of the Shire of

Esperance is in accordance with the underlying records of the Council,

including:

a. giving a

true and fair view of the Shire’s financial position as at 30 June 2018

and of its performance for the year ended on that date; and

b. complying

with Australian Accounting Standards (including Australia Accounting

Interpretations), the Local Government Act 1995 (as amended) and the Local

Government (Financial Management) Regulations 1996 (as amended).”

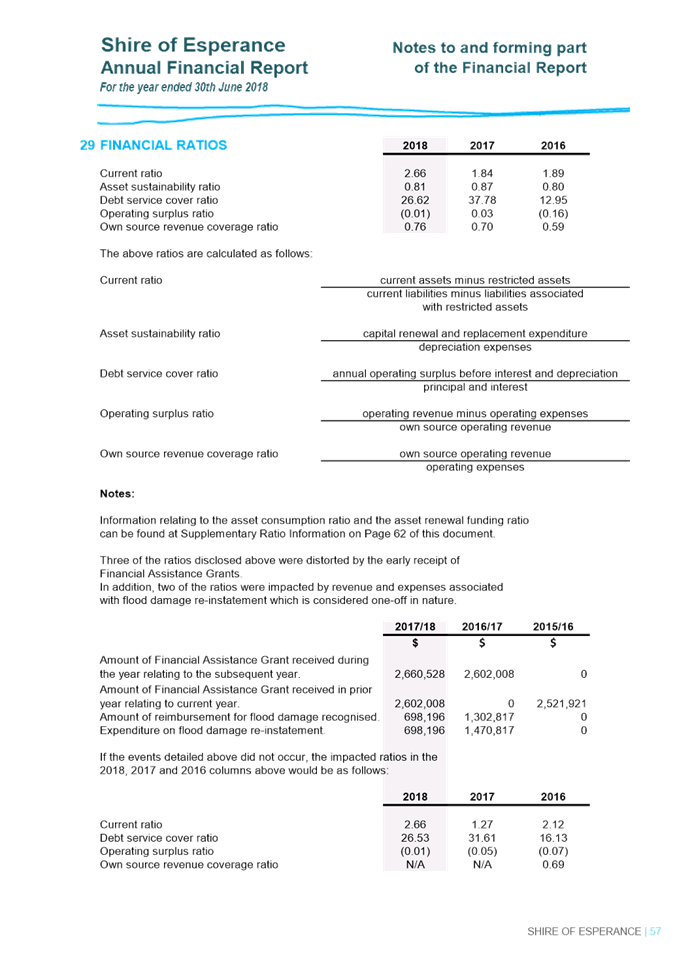

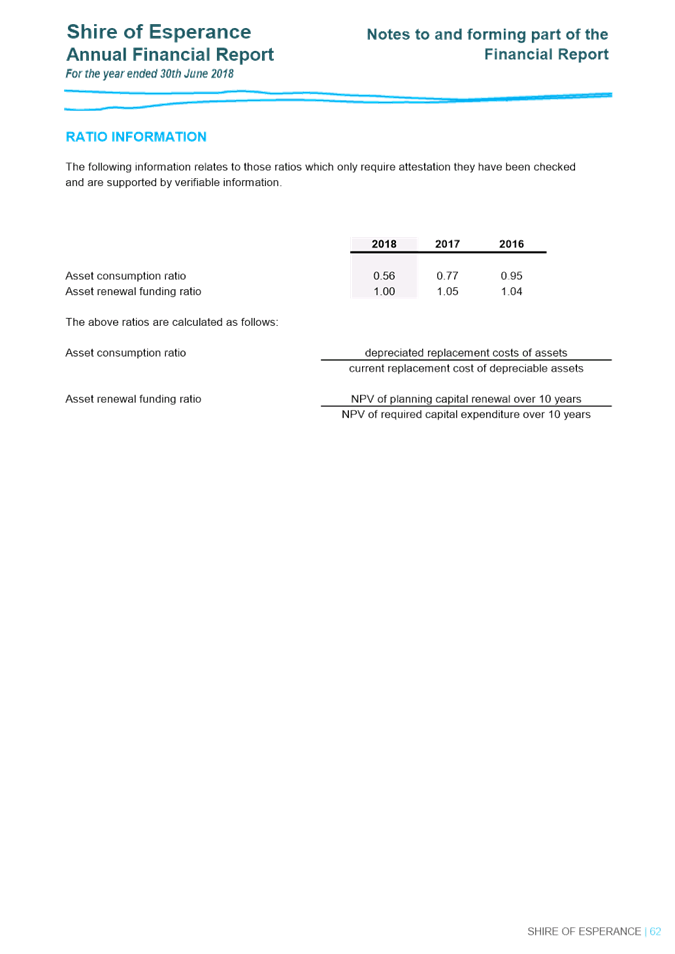

The audit did not note any adverse trends apart from two

ratio’s not meeting the minimum benchmark as determined by the Department

of Local Government guidelines.

The two ratios in question is the Operating Surplus ratio and

Asset Sustainability ratio. This is something Council has been addressing

over the past few years and will be continuing to do so over the next five

years. Strategies to achieve this are identified in the Long Term Financial

Plan. This should see a gradual improvement in both of these ratios.

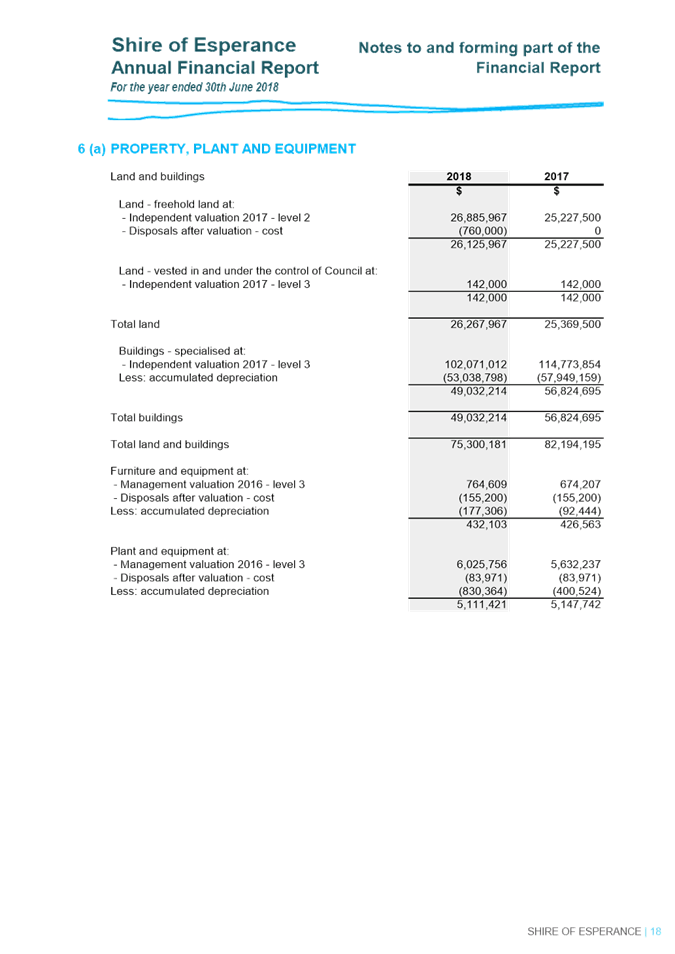

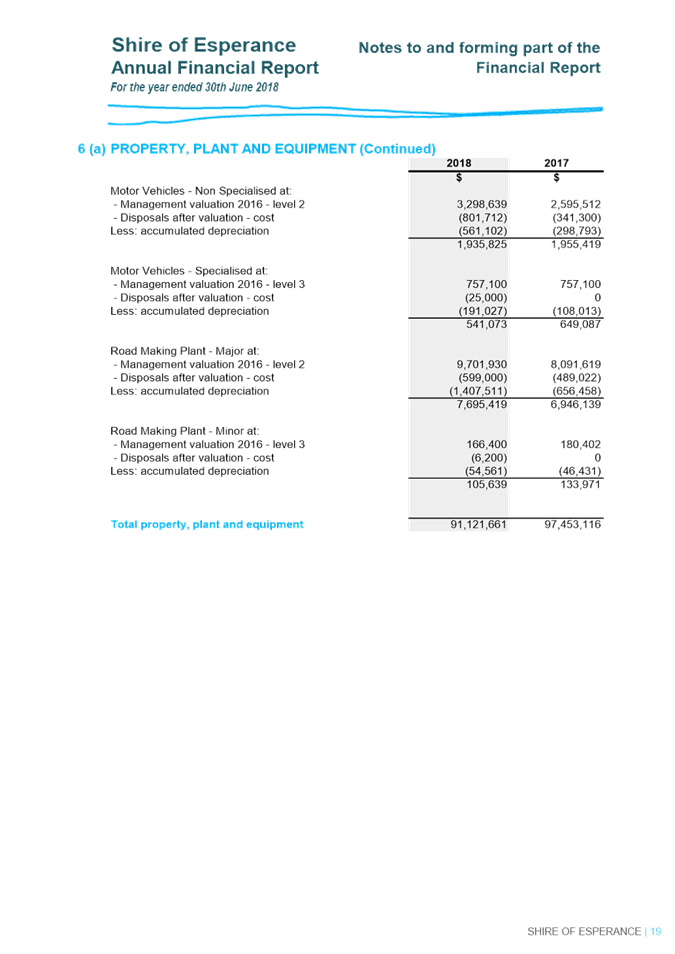

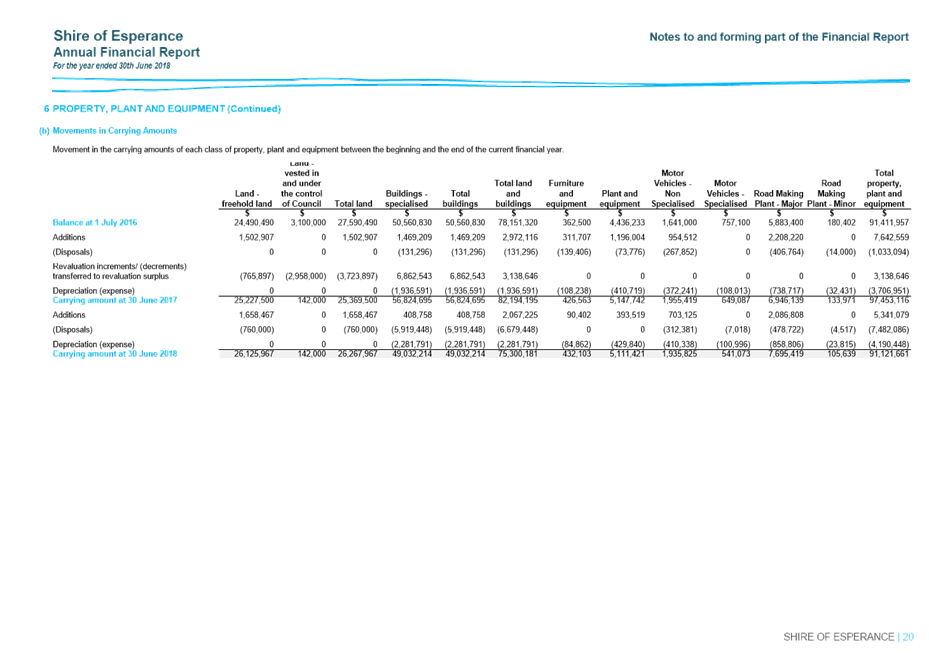

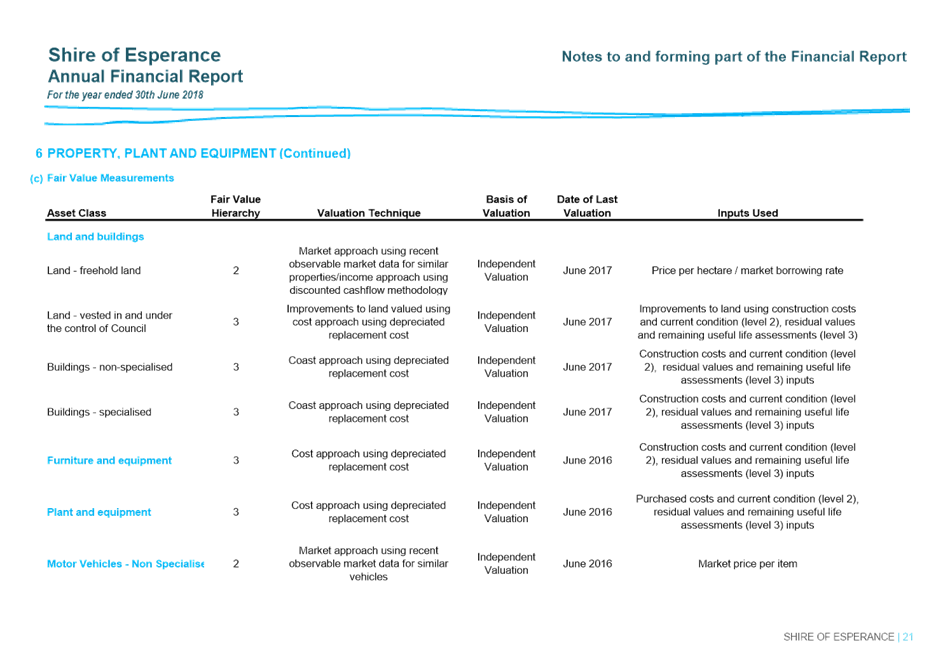

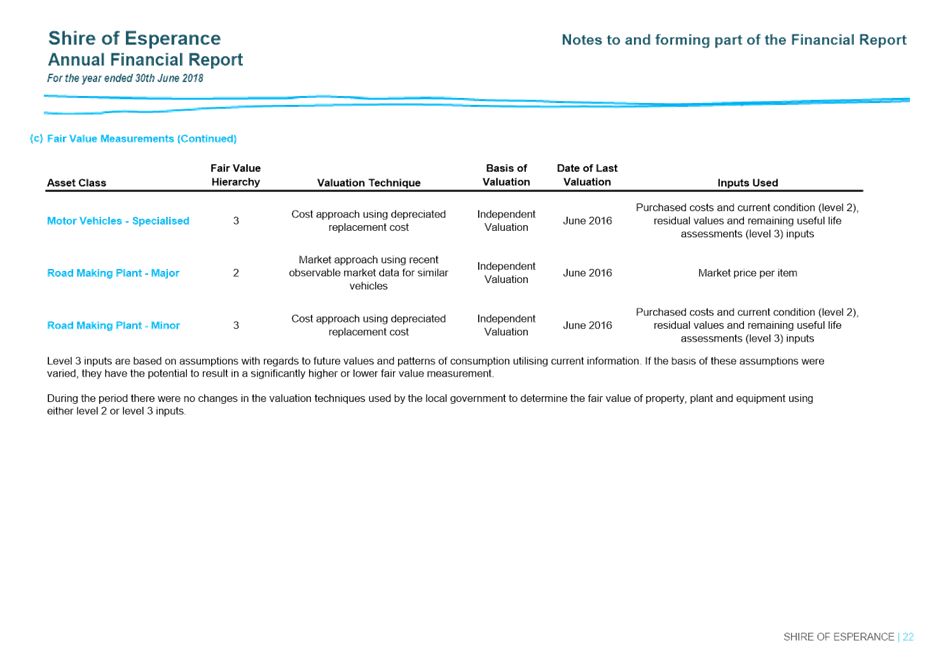

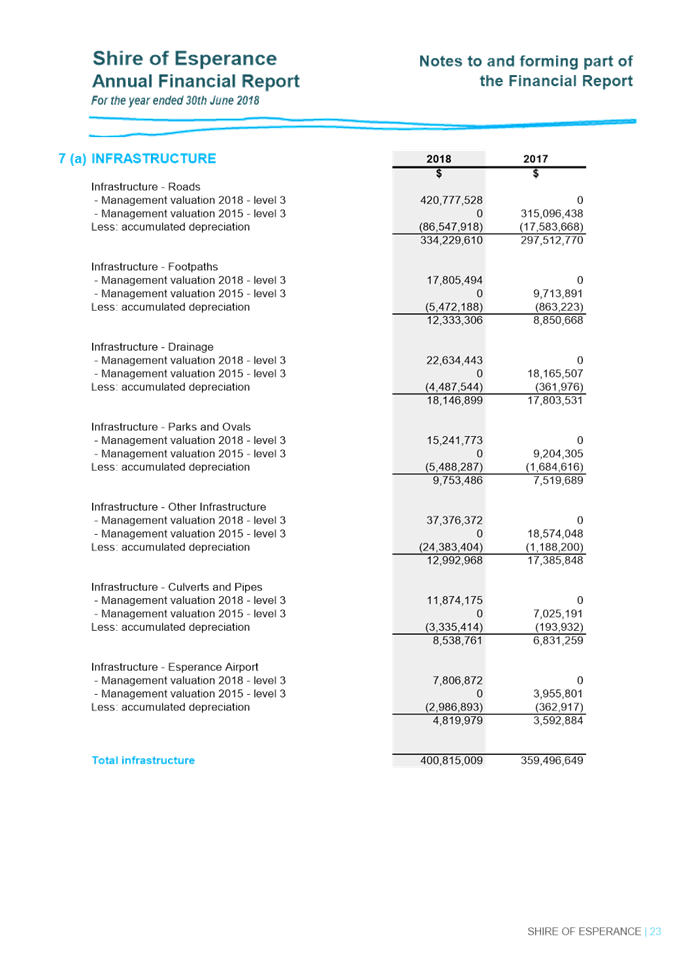

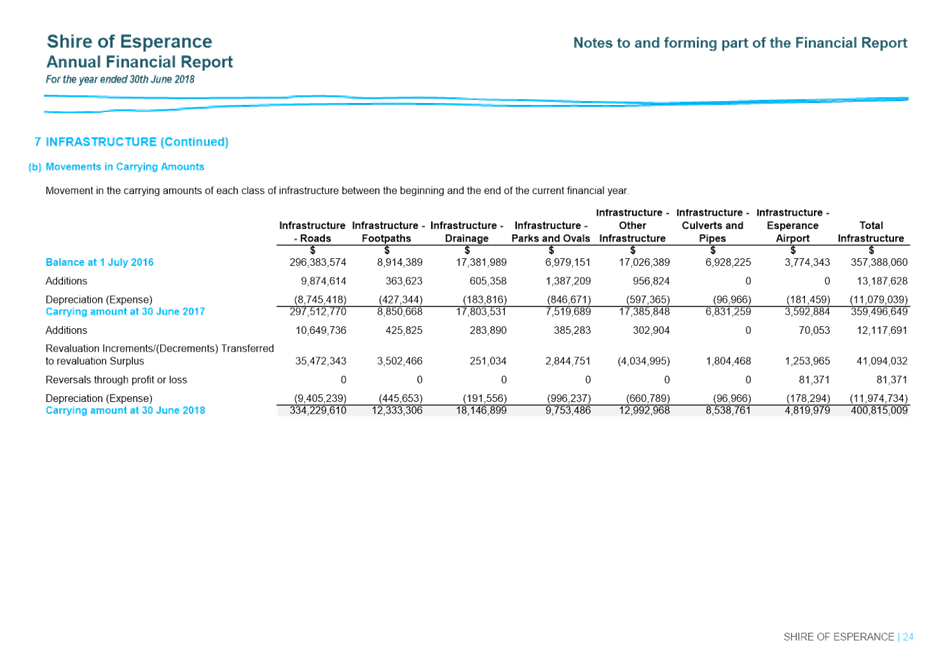

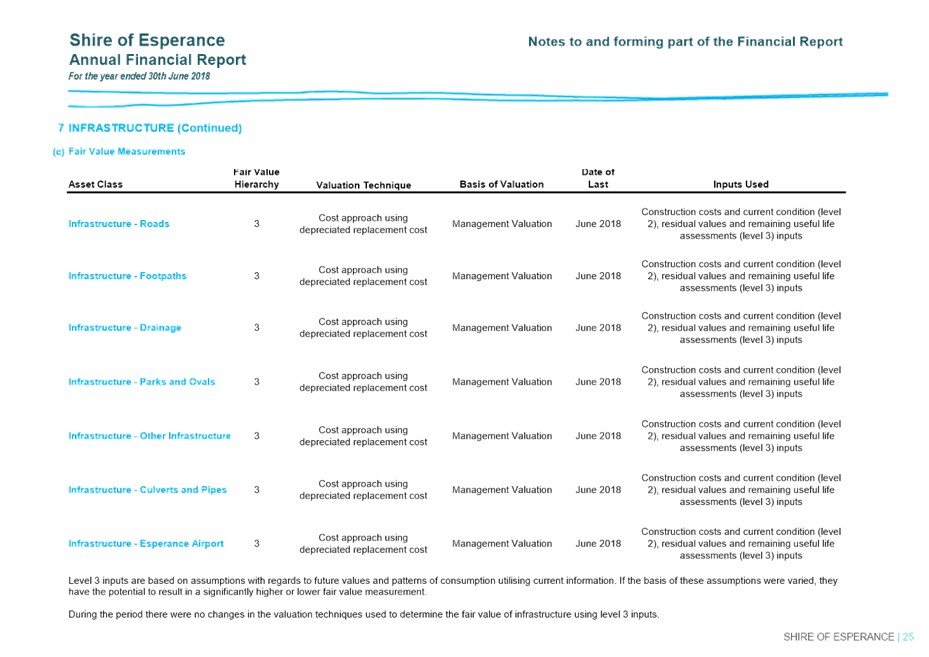

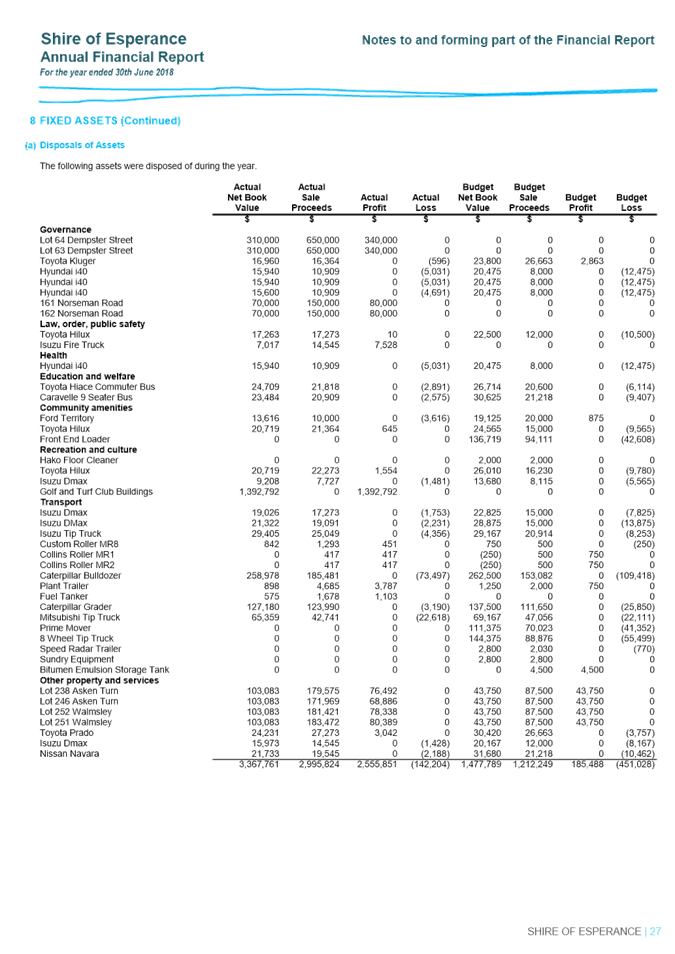

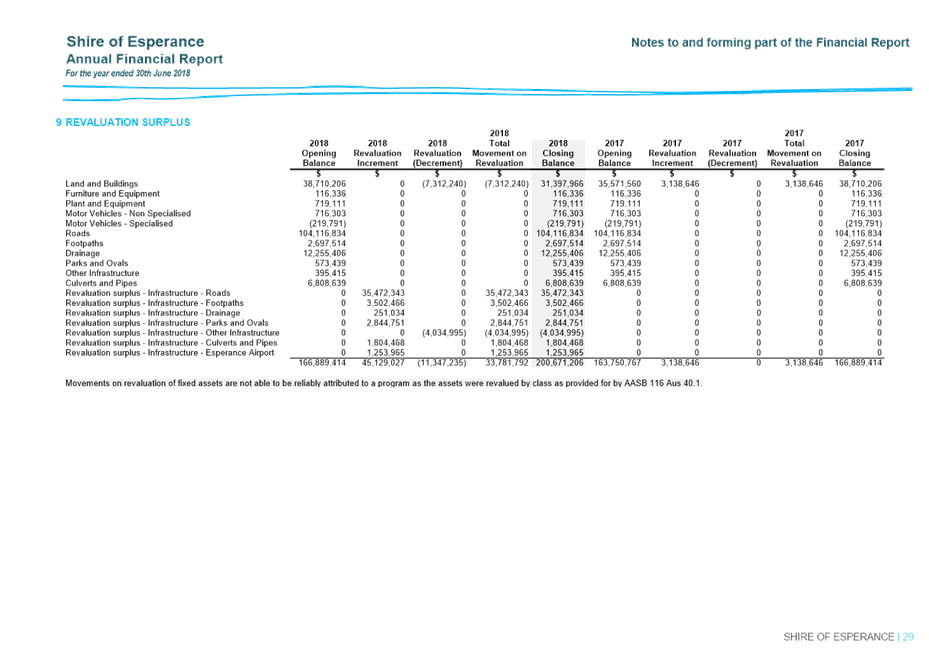

Revaluation of Infrastructure occurred during 2018 resulting

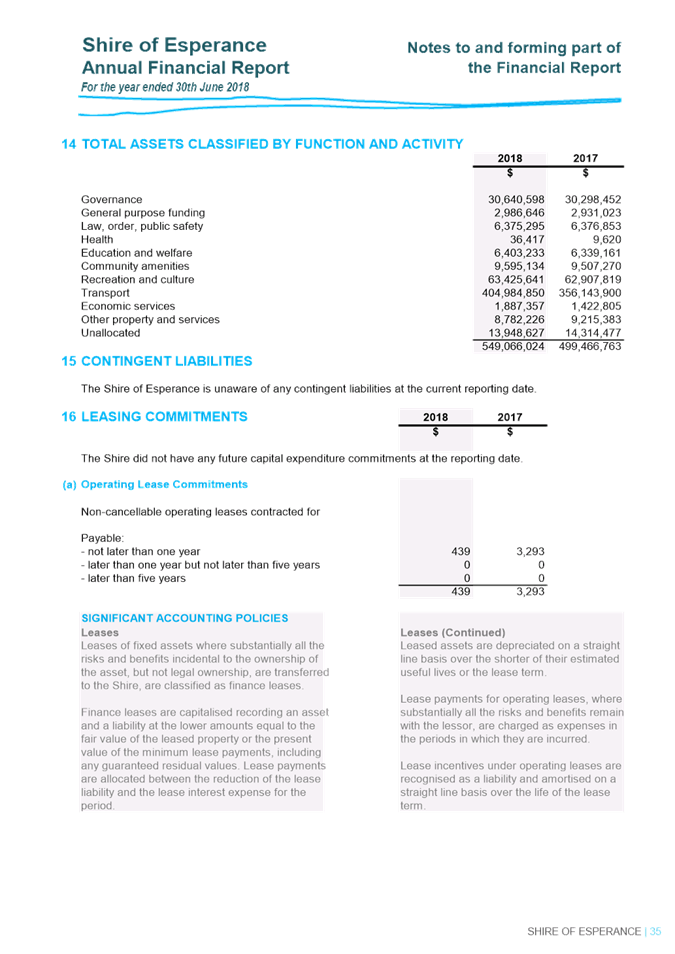

in a net increase of nearly $34m. At the same time the five golf courses

and their assets were removed from the Shire’s asset register as they are

not owned or in the control of the Shire. However the golf courses’ land

still remains on the asset register as the land is Shire owned.

There was a slight reduction to the 2018 surplus closing

position of $4,928 to what was presented to Council at Budget adoption.

This was due to end of year processing that had not been completed when the

budget was presented to Council.

Consultation

Nil

Financial Implications

As per the 2018/19 Budget.

Asset Management Implications

Nil

Statutory Implications

The statutory implications associated with this item

are Local Government Act (1995) Section 7.12A which details duties with respect

to audits.

Policy Implications

Nil

Strategic Implications

Strategic Community Plan 2017 - 2027

Community

Leadership

A financially

sustainable and supportive organisation achieving operational excellence

Provide

responsible resource and planning management for now and the future

Environmental Considerations

Nil

Attachments

|

a⇩.

|

Annual Financial Report

2017/18

|

|

|

b⇩.

|

Management Letter

2017/18

|

|

|

Officer’s Recommendation

That the Audit Committee

1. Receive

the 2017/18 Annual Financial Report incorporating the Audit Report as

attached at Attachment A.

2. Receive

the Management Letter for the 2017/18 financial year as attached at

Attachment B.

3. Recommends

the Annual Financial Report, Audit Report and Management Letter for the

2017/18 financial year to Council for adoption.

Voting Requirement Simple Majority

|

Item: 9.3

CEO Review of Systems and Procedures

|

Author/s

|

Sarah Walsh

|

Coordinator Corporate Support

|

|

Authorisor/s

|

Shane Burge

|

Director Corporate Resources

|

File Ref: D18/26571

Applicant

Internal

Location/Address

Shire of Esperance

Executive Summary

For the Audit Committee to consider the report from the CEO

on the appropriateness and effectiveness of the Shire of Esperance systems and

procedures in relation to risk management, internal control and legislative

requirements.

Recommendation in Brief

That the Audit Committee accept the report from the CEO on

the appropriateness and effectiveness of the Shire of Esperance systems and

procedures in relation to risk management, internal control and legislative

requirements and recommend the review to Council for endorsement.

Background

In accordance with Regulation 17 of the Local

Government (Audit) Regulations 1996, the CEO is required to review the

appropriateness and effectiveness of the Shire of Esperance’s systems and

procedures in relation to risk management, internal control and legislative

requirements not less than once every three years.

The review process was developed along with Local Government

Insurance Service (LGIS) during 2014 in regards to risk, internal control and

legislative compliance. The Department of Local Government has developed

guidelines to assist Local Governments in determining the issues that should be

considered in any review process -

Risk Management

Internal control and risk management systems and

programs are a key expression of a local government’s attitude to

effective controls. Good audit committee practices in monitoring internal

control and risk management programs typically include:

· Reviewing whether the local

government has an effective risk management system and that material operating

risks to the local government are appropriately considered;

· Reviewing whether the local

government has a current and effective business continuity plan (including

disaster recovery) which is tested from time to time;

· Assessing the internal processes for

determining and managing material operating risks in accordance with the local

government’s identified tolerance for risk, particularly in the following

areas;

–

Potential non-compliance with legislation, regulations, standards and local

government’s policies;

– Important

accounting judgements or estimates that prove to be wrong;

– Litigation and

claims;

– Misconduct, fraud

and theft;

– Significant

business risks, recognising responsibility for general or specific risk areas.

For example, environmental, occupational health and safety risk, and how they

are managed by the local government;

· Obtaining regular risk reports, which

identify key risks, the status and the effectiveness of the risk management

systems, to ensure that identified risks are monitored and new risks are

identified, mitigated and reported;

· Assessing the adequacy of local

government processes to manage insurable risks and ensure the adequacy of

insurance cover, and if applicable, the level of self-insurance;

· Reviewing the effectiveness of the

local government’s internal control system with management and the

internal and external auditors;

· Assessing whether management has

controls in place for unusual types of transactions and/or any potential

transactions that might carry more than an acceptable degree of risk;

· Assessing the local

government’s procurement framework with a focus on the probity and

transparency of policies and procedures/processes and whether these are being

applied;

· Should the need arise, meeting

periodically with key management, internal and external auditors, and

compliance staff, to understand and discuss any changes in the local

government’s control environment;

· Ascertaining whether fraud and

misconduct risks have been identified, analysed, evaluated and have an

appropriate treatment plan which has been implemented, communicated, monitored

and there is regular reporting and ongoing management of fraud and misconduct

risks.

Internal Control

Internal control is a key component of a sound

governance framework, in addition to leadership, long-term planning,

compliance, resource allocation, accountability and transparency. Strategies to

maintain sound internal controls are based on risk analysis of the internal

operations of a local government.

An effective and transparent internal control

environment is built on the following key areas:

· integrity and ethics;

· policies and delegated authority;

· levels of responsibilities and

authorities;

· audit practices;

· information system access and

security;

· management operating style; and

· human resource management and

practices.

Internal control systems involve policies and

procedures that safeguard assets, ensure accurate and reliable financial

reporting, promote compliance with legislation and achieve effective and

efficient operations and may vary depending on the size and nature of the local

government.

Aspects of an effective control framework will

include:

· delegation of authority;

· documented policies and procedures;

· trained and qualified employees;

· system controls;

· effective policy and process review;

· regular internal audits;

· documentation of risk identification

and assessment; and

· regular liaison with auditor and

legal advisors.

The following are examples of controls that are

typically reviewed:

· separation of roles and functions,

processing and authorisation;

· control of approval of documents,

letters and financial records;

· comparison of internal data with

other or external sources of information;

· limit of direct physical access to

assets and records;

· control of computer applications and

information system standards;

· limit access to make changes in data

files and systems;

· regular maintenance and review of

financial control accounts and trial balances;

· comparison and analysis of financial

results with budgeted amounts;

· the arithmetical accuracy and content

of records;

· report, review and approval of

financial payments and reconciliations; and

· comparison of the result of physical

cash and inventory counts with accounting records.

Legislative Compliance

The compliance programs of a local government are a

strong indication of attitude towards meeting legislative requirements. Audit

committee practices in regard to monitoring compliance programs typically

include:

· Monitoring compliance with

legislation and regulations;

· Reviewing the annual Compliance Audit

Return and reporting to Council the results of that review;

· Staying informed about how management

is monitoring the effectiveness of its compliance and making recommendations

for change as necessary;

· Reviewing whether the local

government has procedures for it to receive, retain and treat complaints,

including confidential and anonymous employee complaints;

· Obtaining assurance that adverse

trends are identified and review management’s plans to deal with these;

· Reviewing management disclosures in

financial reports of the effect of significant compliance issues;

· Reviewing whether the internal and/or

external auditors have regard to compliance and ethics risks in the development

of their audit plan and in the conduct of audit projects, and report compliance

and ethics issues to the audit committee;

· Considering the internal

auditor’s role in assessing compliance and ethics risks in their plan;

· Monitoring the local

government’s compliance frameworks dealing with relevant external

legislation and regulatory requirements; and

· Complying with legislative and

regulatory requirements imposed on audit committee members, including not

misusing their position to gain an advantage for themselves or another or to

cause detriment to the local government and disclosing conflicts of interest.

The last review was undertaken in November 2016 and

the review recently undertaken by the CEO is now to be considered.

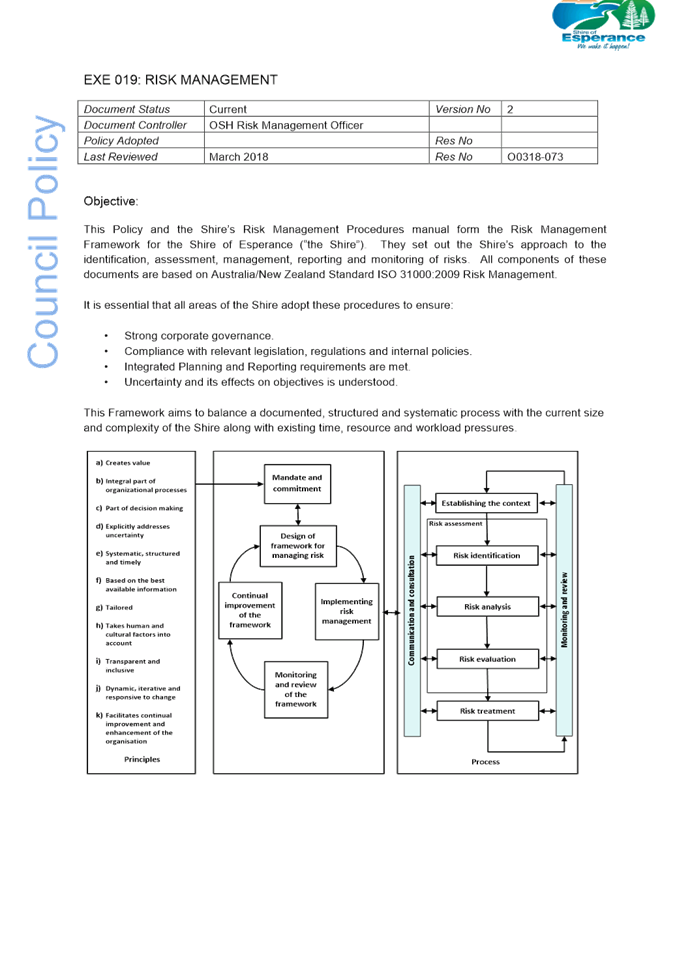

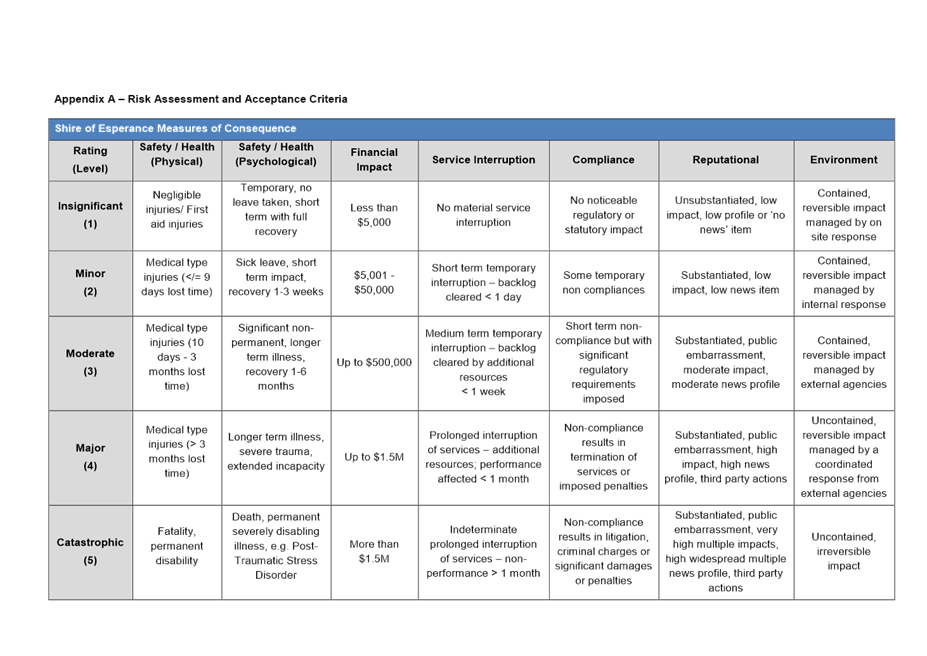

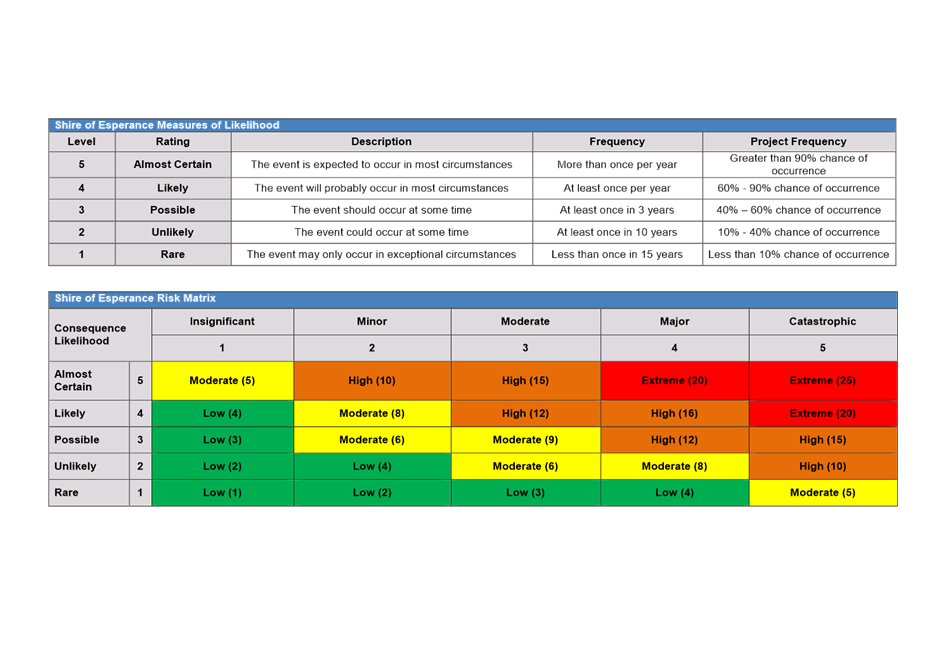

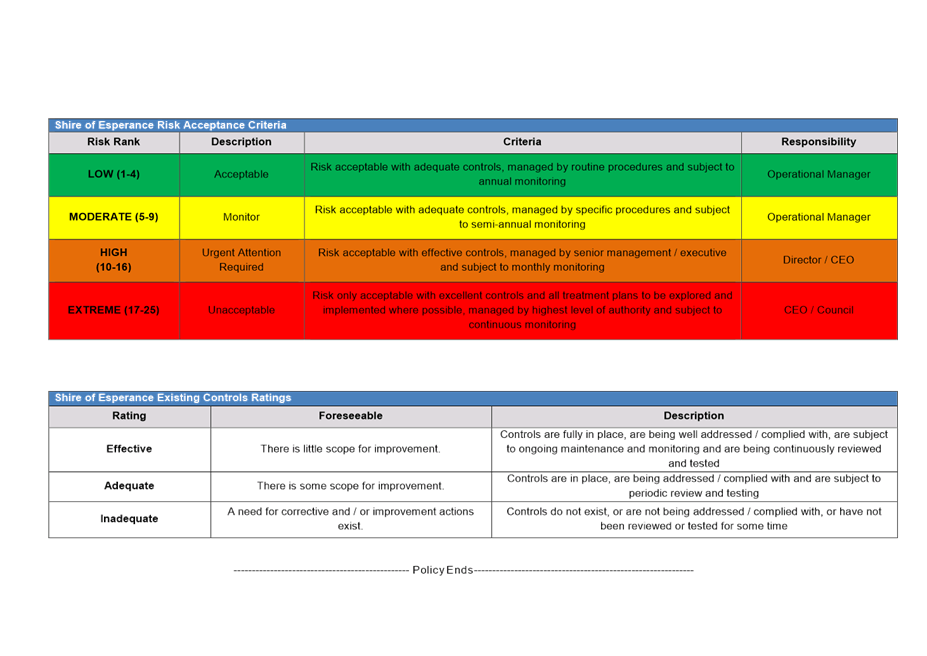

The Shire’s Risk Management Policy (Attachment

A) provides guidance and direction in relation to risk management and

determines the Shire’s risk appetite with regard to the measures of

consequence and likelihood of each risk.

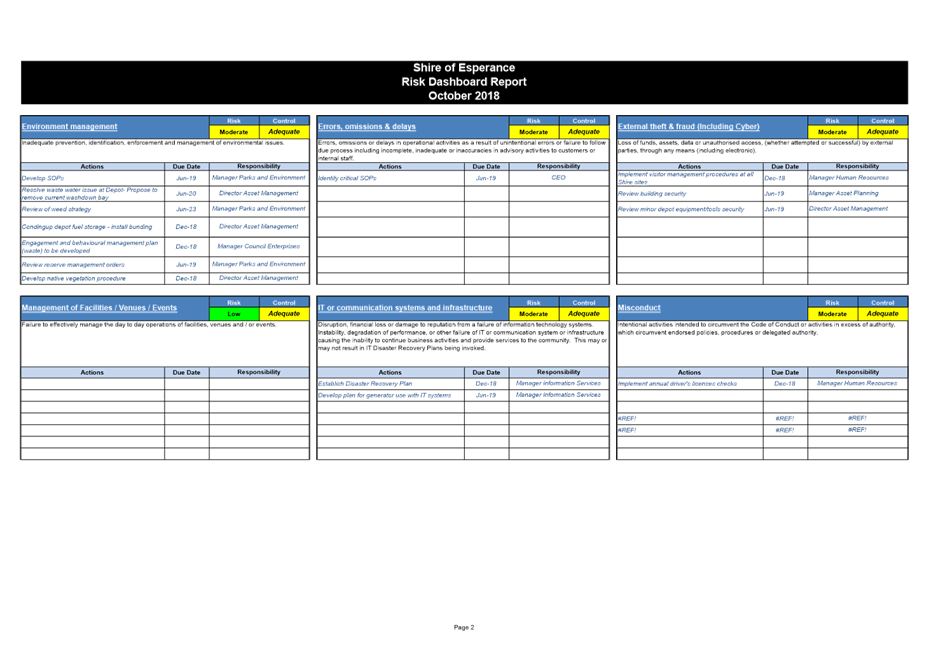

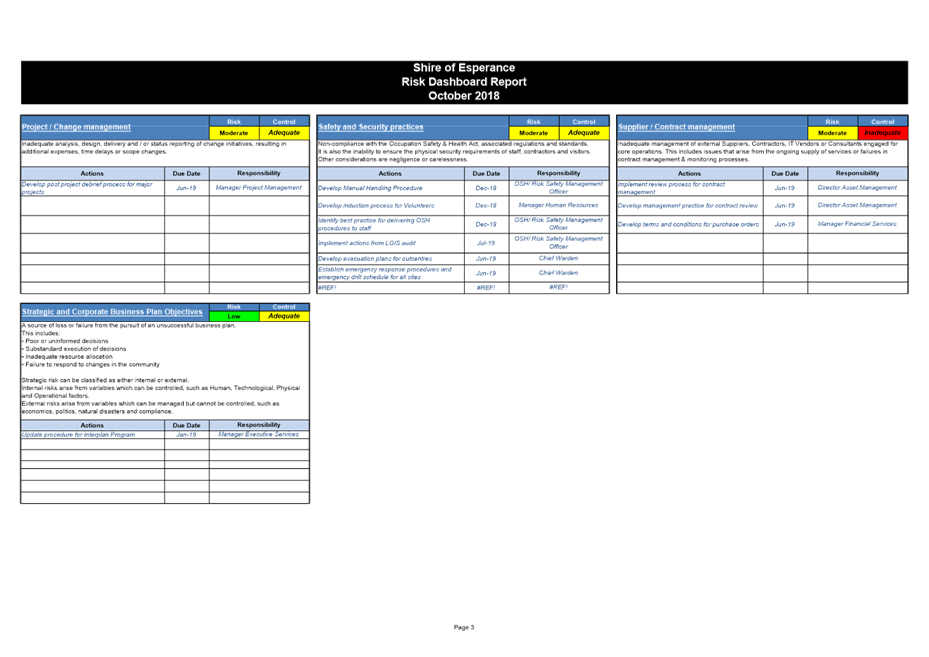

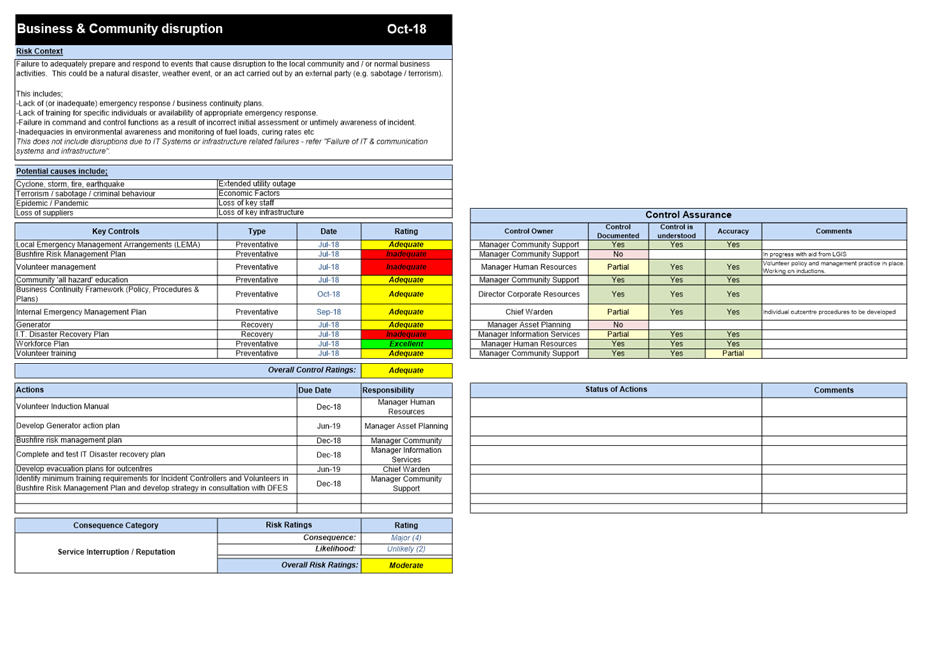

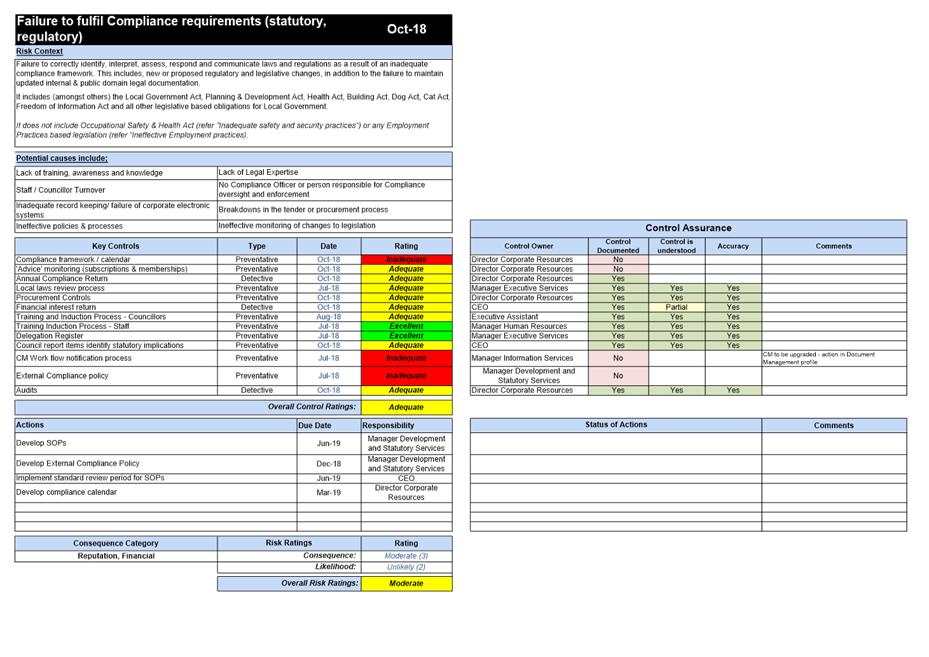

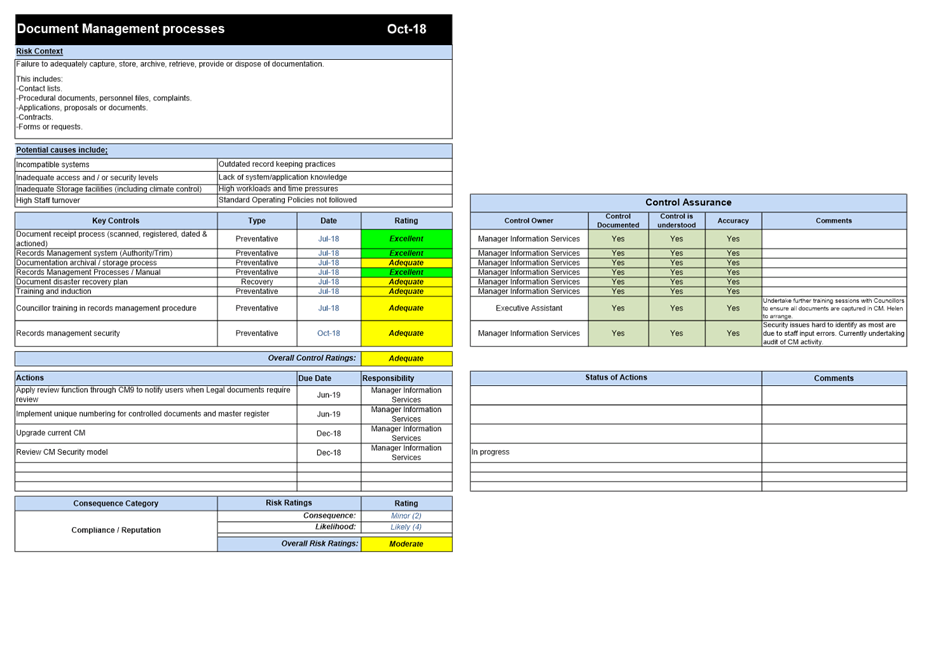

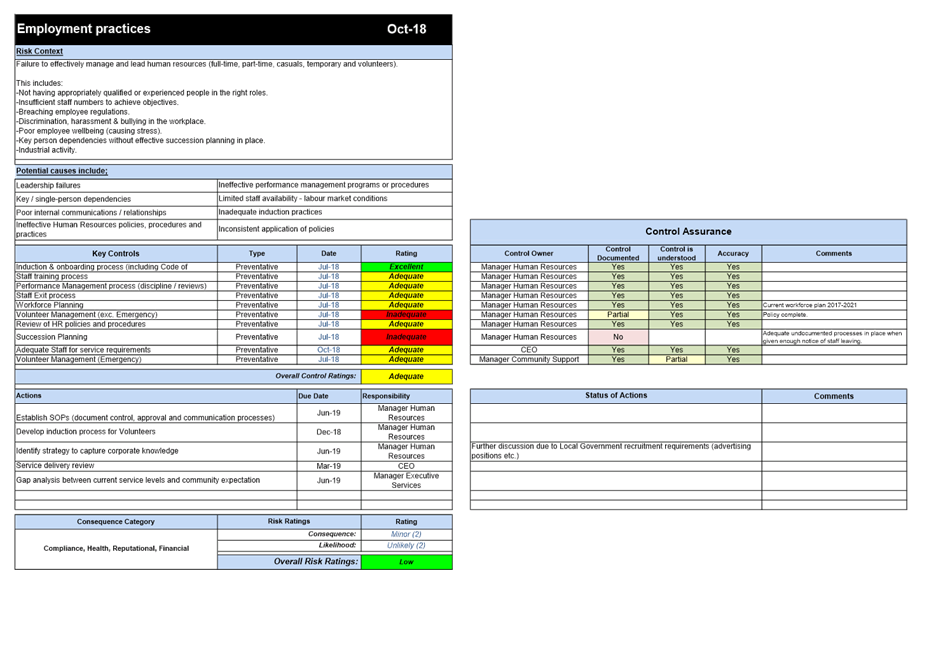

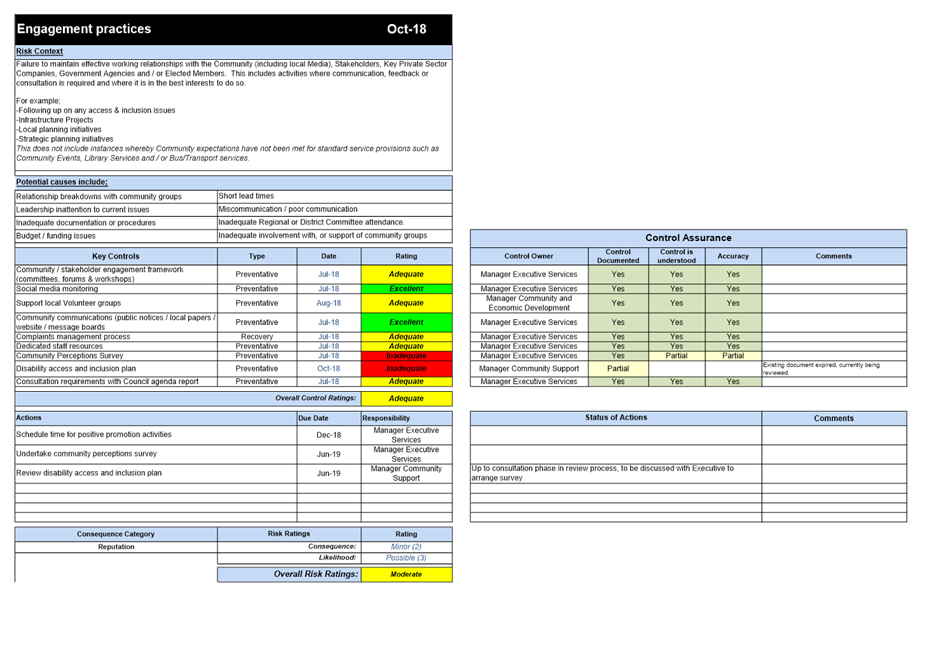

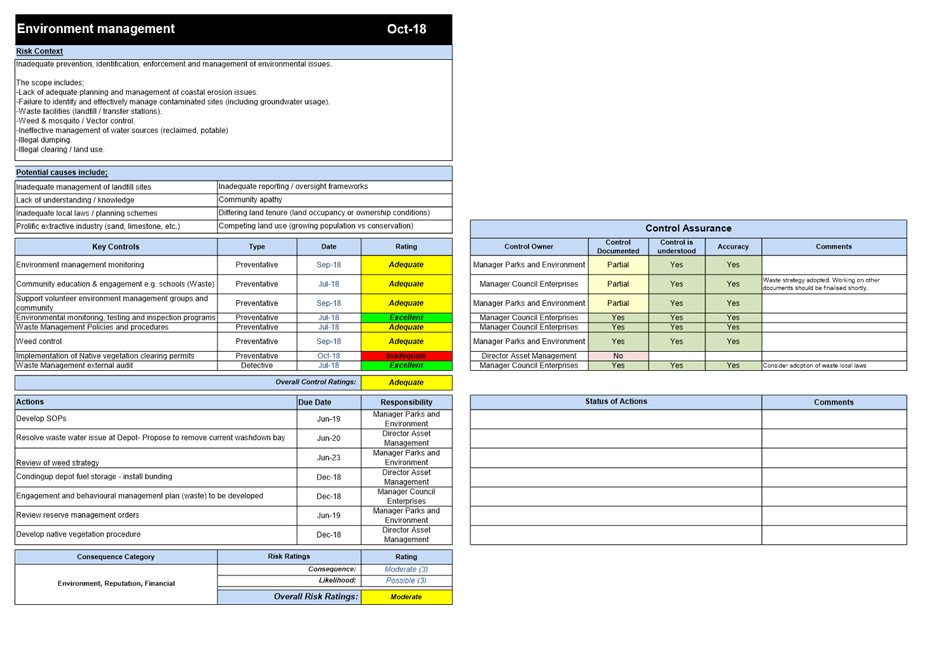

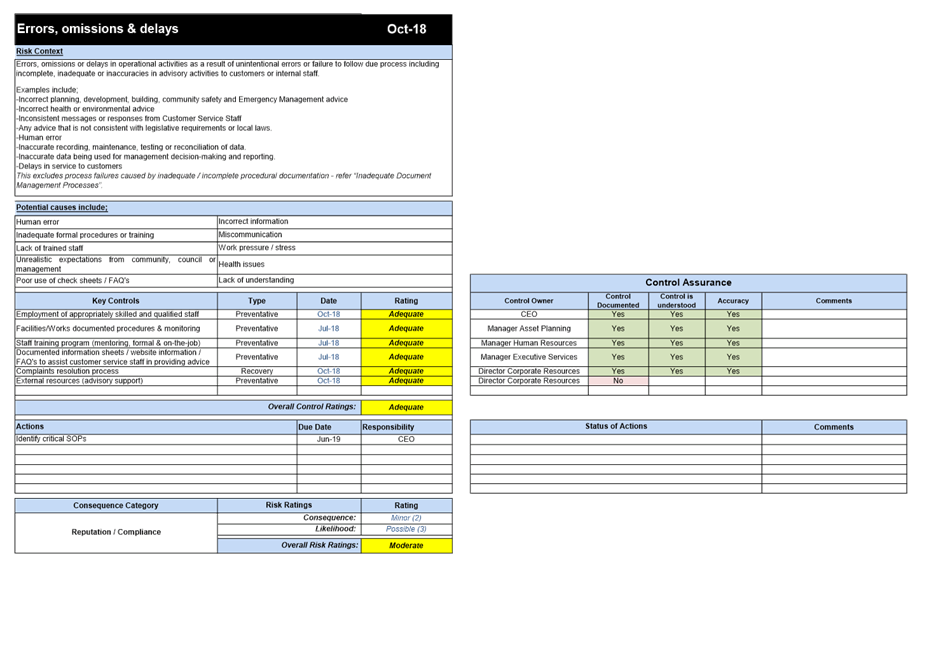

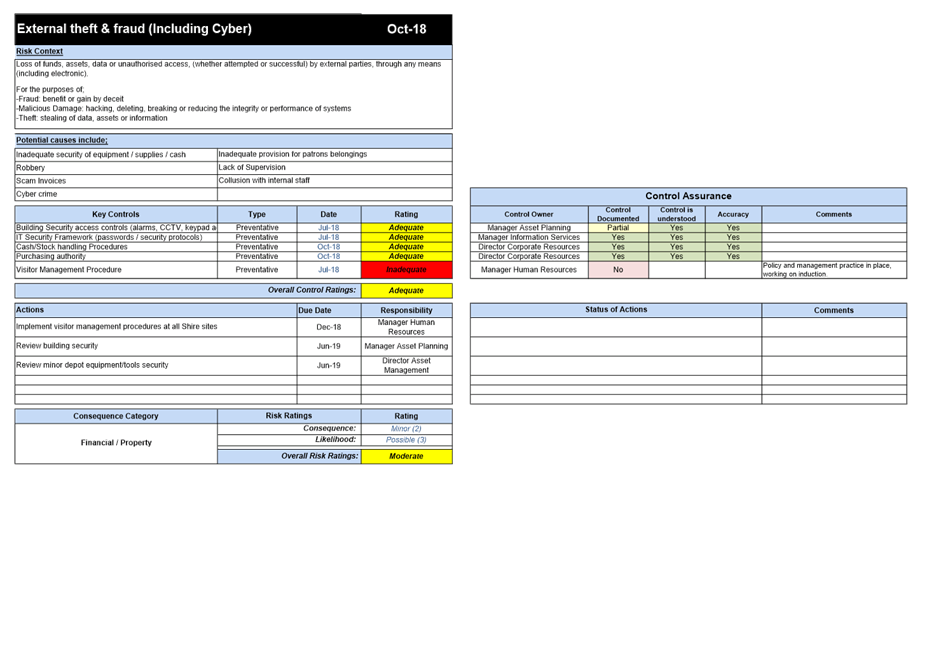

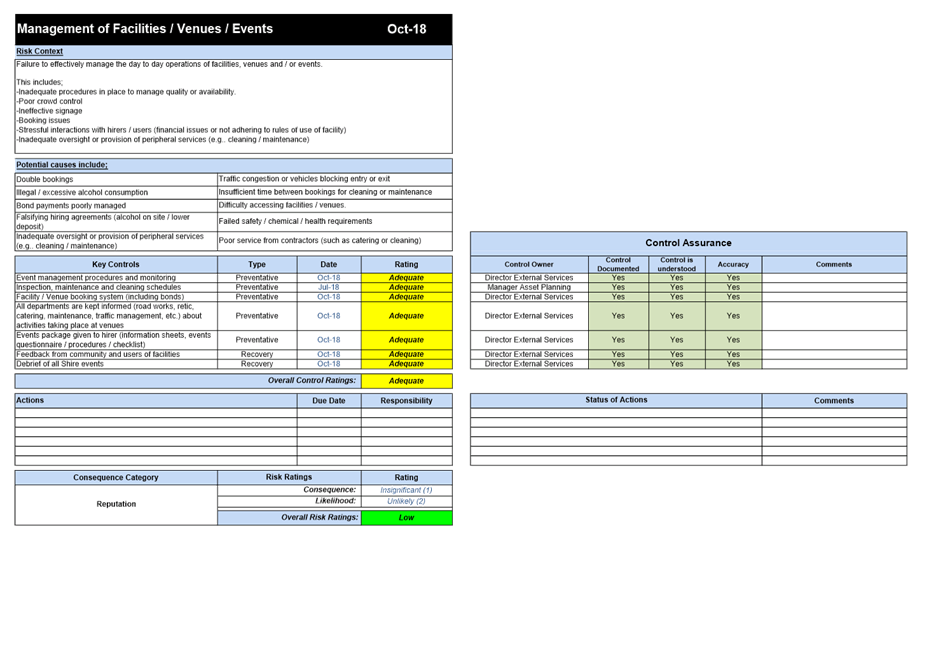

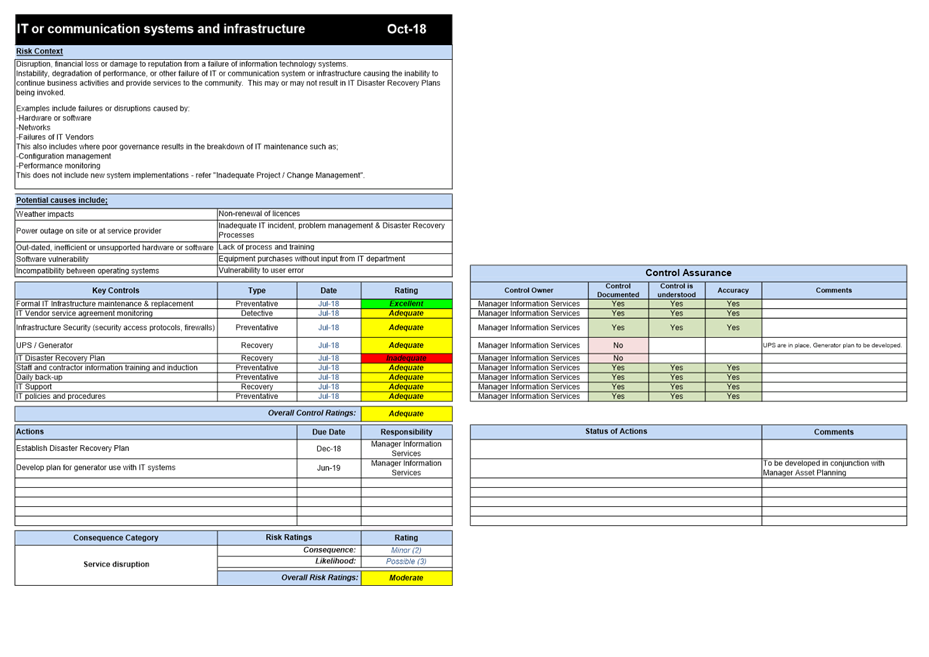

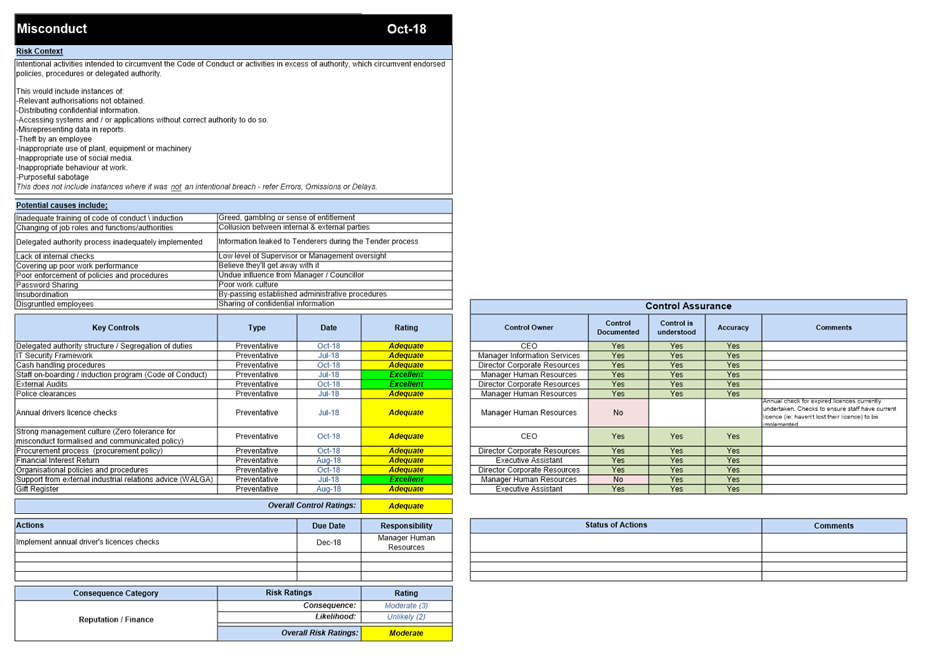

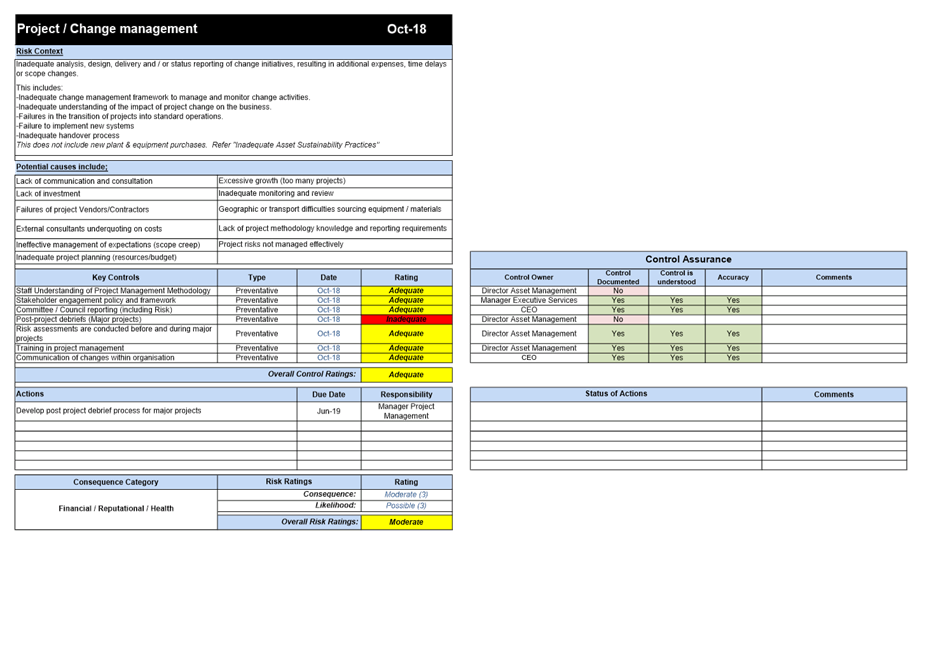

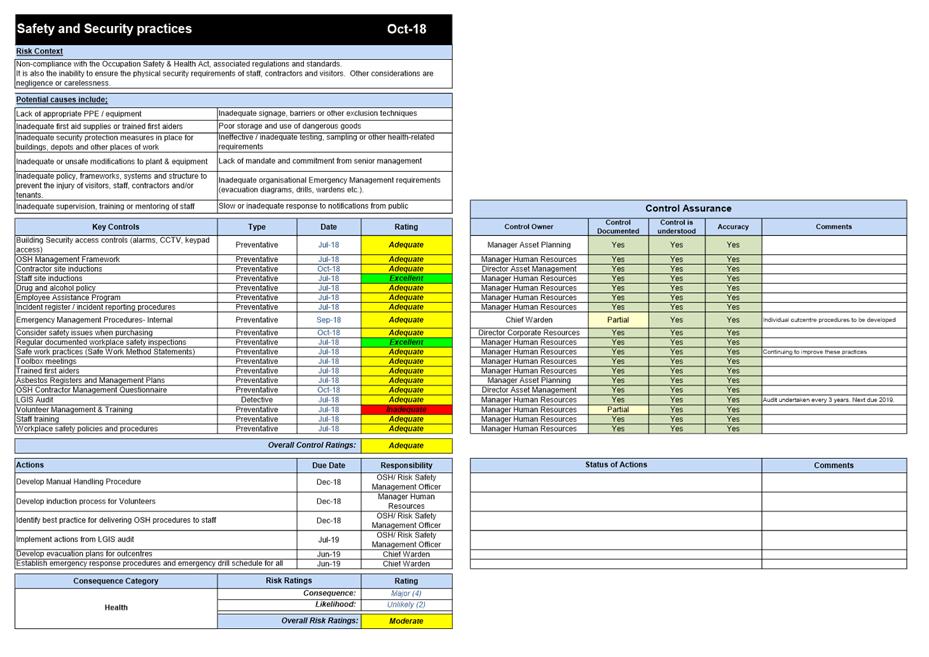

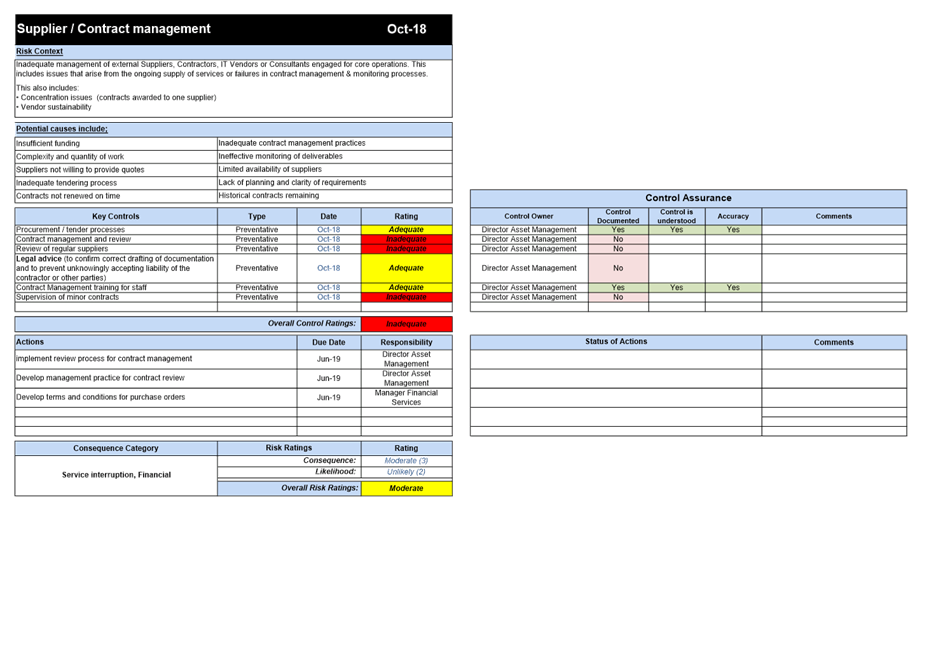

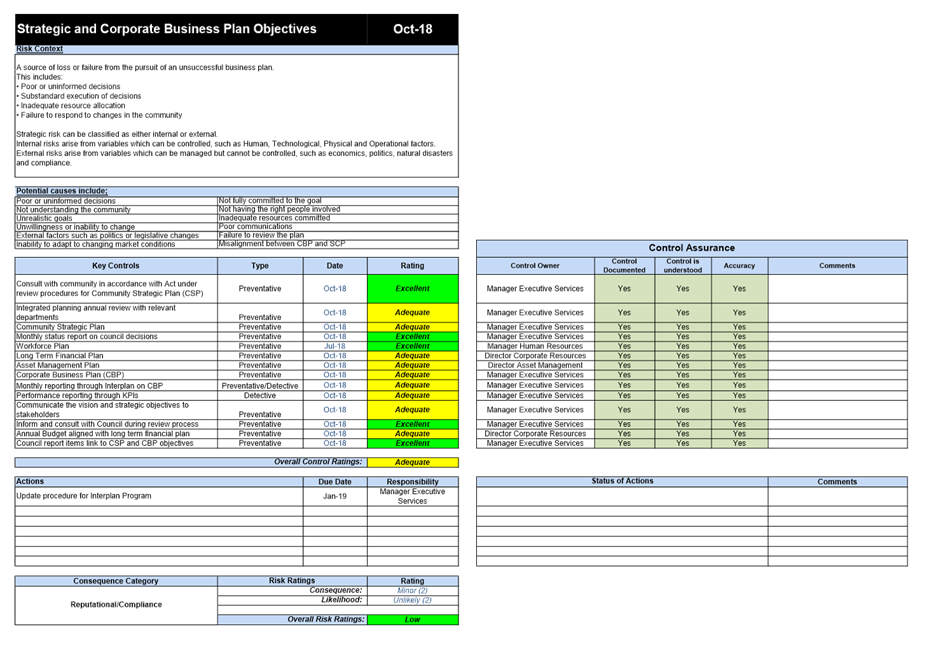

Officer’s Comment

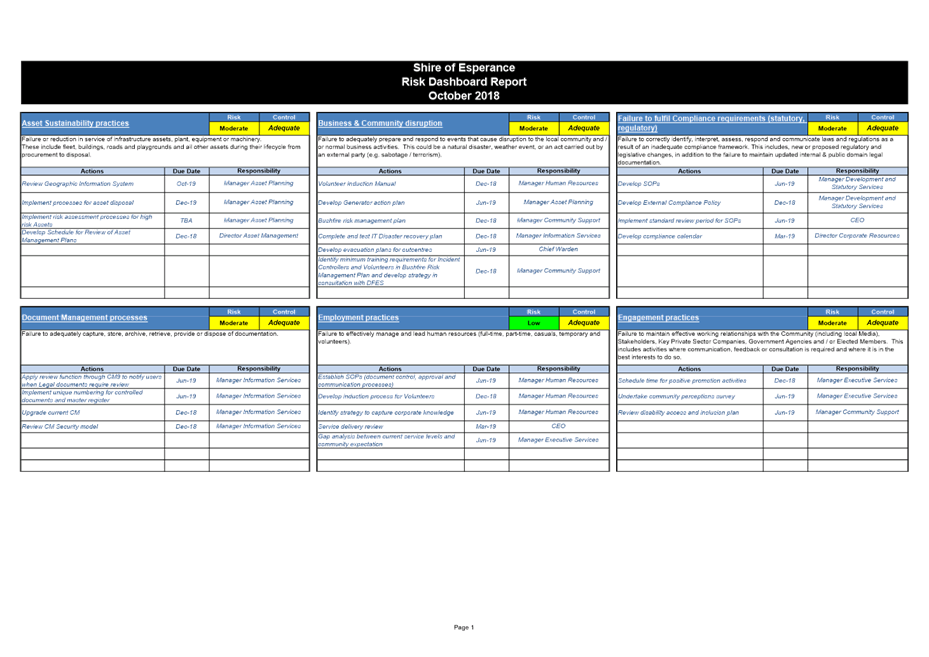

Attachment B has the risk management report and the

process that the Shire has worked through to determine the level of risk for

each risk theme and to what level the risk is being managed. The executive

summary provides a brief snapshot of each risk profile with appropriate colour

coding to easily identify the risk rating along with the level of control. The

executive summary also outlines those actions that are proposed to improve the

level of control for the risk theme. The full analysis for each profile is then

attached listing all the controls and the effectiveness of each control.

Actions have been suggested to improve controls and therefore reduce the risk.

It has been identified that the only area where there

is an inadequate level of controls in place is with regard to the supplier and

contract management risk profile. This is due to a lack of established

procedures for;

· reviewing contracts;

· monitoring minor contracts; and

· reviewing regular supplier’s

performance.

These procedures should be developed by the end of the

current financial year.

The treatment or action that is proposed will depend

upon the cost or resources required to improve the control. It may be

determined that some control measures are too resource intensive to implement

compared to the level of increased control that will be obtained.

Prioritisation and analysis of cost/benefit will be required in some instances

due to resource or budget constraints.

The risk management analysis has been a useful

exercise to evaluate the Shire’s business practices and determine how

effective they are operating. The process is used to communicate to staff who

have responsibility for the areas around areas of improvement or efficiency. It

is expected that this high level risk analysis will also provide guidance in

future decision making and resource allocation where business practice needs

improvement or the Shire is exposed to an unacceptable level of risk.

Consultation

OSH/Risk Officer

Middle Management

Directors

Financial Implications

Although there are no direct financial implications

arising from this report the actions that have been identified to increase controls

or reduce risk may have financial or resource implications for the

organisation. The cost of implementing the controls to reduce or manage risk

will need to be weighed up against the risk appetite of the organisation to

determine the most appropriate course of action.

Asset Management Implications

Nil

Statutory Implications

Local Government (Audit) Regulations

1996

– r.17 CEO to review certain systems and procedures

Policy Implications

EXE019: Risk Management

Strategic Implications

Strategic Community Plan 2017 - 2027

Community

Leadership

A financially

sustainable and supportive organisation achieving operational excellence

Provide

responsible resource and planning management for now and the future

Corporate Business Plan 2017/2018

– 2020/2021

Manage Risk Management System

Environmental Considerations

Nil

Attachments

|

a⇩.

|

Risk Management Policy

|

|

|

b⇩.

|

Risk Register Report

|

|

|

Officer’s Recommendation

That the Audit

Committee;

1. Accept

the CEO’s review of the appropriateness and effectiveness of the Shire of Esperance systems

and procedures in relation to risk management, internal control and

legislative compliance; and

2. Recommend the review to Council for

endorsement.

Voting Requirement Simple Majority

|