Disclosure of Interests

Disclosure of Interests

Notes for Your Guidance

Notes for Your Guidance

Impact of a

Financial Interest (s. 5.65. & s. 67.

Local Government Act 1995)

A

member who has a Financial Interest in any matter to be discussed at a Council or

Committee Meeting, which will be attended by the member, must disclose the nature

of the interest:

a. In a written notice given to the Chief Executive

Officer before the Meeting or;

b. At the Meeting immediately before the matter is

discussed.

A member, who makes a

disclosure in respect to an interest, must not:

a. Preside at the part of the Meeting relating to the

matter or;

b. Participate in, or be present during, any discussion

or decision making procedure relative to the matter, unless and to the extent

that, the disclosing member is allowed to do so under Section 5.68 or Section

5.69 of the Local Government Act 1995.

Interests

Affecting Financial Interest

The

following notes are a basic guide for Councillors when they are considering

whether they have a Financial Interest in a

matter.

1. A Financial Interest, pursuant to s. 5.60A or 5.61 of

the Local Government Act 1995, requiring disclosure occurs when a Council

decision might advantageously or detrimentally affect the Councillor or a

person closely associated with the Councillor and is capable of being measured

in money terms. There are expectations in the Local Government Act 1995

but they should not be relied on without advice, unless the situation is very

clear.

2. If a Councillor is a member of an Association (which

is a Body Corporate) with not less than 10 members i.e sporting, social,

religious etc, and the Councillor is not a holder of office of profit or a

guarantor, and has not leased land to or from the club, i.e, if the Councillor

is an ordinary member of the Association, the Councillor has a common and not a

financial interest in any matter to that Association.

3. If an interest is shared in common with a significant

number of electors and ratepayers, then the obligation to disclose that

interest does not arise. Each case needs to be considered.

4. If in doubt declare.

5. As stated if written notice disclosing the interest

has not been given to the Chief Executive Officer before the meeting, then it must be

given when the matter arises in the Agenda, and immediately before the matter

is discussed. Under s. 5.65 of the Local Government Act 1995

failure to notify carries a penalty of $10 000 or imprisonment for 2 years.

6. Ordinarily the disclosing Councillor must leave the

meeting room before discussion commences. The only exceptions are:

6.1 Where

the Councillor discloses the extent of the interest, and Council carries a motion

under s.5.68(1)(b)(ii) of the Local Government Act 1995; or

6.2 Where

the Minister allows the Councillor to participate under s.5.69(3) of the

Local Government Act 1955, with or without conditions.

Interests Affecting

Proximity (s. 5.60b Local Government Act 1995)

1. For the purposes of this subdivision, a person has a

proximity interest, pursuant to s.5.60B of the Local Government Act 1995,

in a matter if the matter concerns;

- a

proposed change to a planning scheme affecting land that adjoins the

person’s land; or

- a

proposed change to the zoning or use of land that adjoins the

person’s land; or

- a

proposed development (as defined in section 5.63(5)) of land that adjoins

the person’s land.

2. In this section, land (the proposal land) adjoins a

person’s land if;

- The

proposal land, not being a thoroughfare, has a common boundary with the

person’s land; or

- The

proposal land, or any part of it, is directly across a thoroughfare from,

the person’s land; or

- The

proposal land is that part of a thoroughfare that has a common boundary

with the person’s land.

3. In this section a reference to a person’s land

is a reference to any land owned by the person or in which the person has any

estate or interest.

Interests Affecting Impartiality

Definition:

An interest, pursuant to Regulation 11 of the Local Government (Rules of

Conduct) Regulations 2007, that would give rise to a reasonable belief that the

impartiality of the person having the interest would be adversely affected, but

does not include an interest as referred to in Section 5.60 of the

‘Act’.

A

member who has an Interest Affecting

Impartiality in any matter to be discussed at a Council or Committee

Meeting, which will be attended by the member, must disclose the nature of the interest;

a. In a written notice given to the Chief Executive

Officers before the Meeting or;

b. At the Meeting, immediately before the matter is

discussed

Impact of an Impartiality

disClosure

There

are very different outcomes resulting from disclosing an interest affecting

impartiality compared to that of a financial interest. With the declaration of

a financial interest, an elected member leaves the room and does not vote.

With

the declaration of this type of interest, the elected member stays in the room,

participates in the debate and votes. In effect then, following disclosure of

an interest affecting impartiality, the member’s involvement in the

Meeting continues as if no interest existed.

6. Purpose

of Meeting

Item: 6.1

Adoption

of 2021/2022 Annual Budget

|

Author/s

|

Beth O'Callaghan

|

Manager Financial Services

|

|

Authorisor/s

|

Felicity Baxter

|

Director Corporate & Community Services

|

File Ref: D21/23203

Applicant

Corporate Resources

Location/Address

Internal

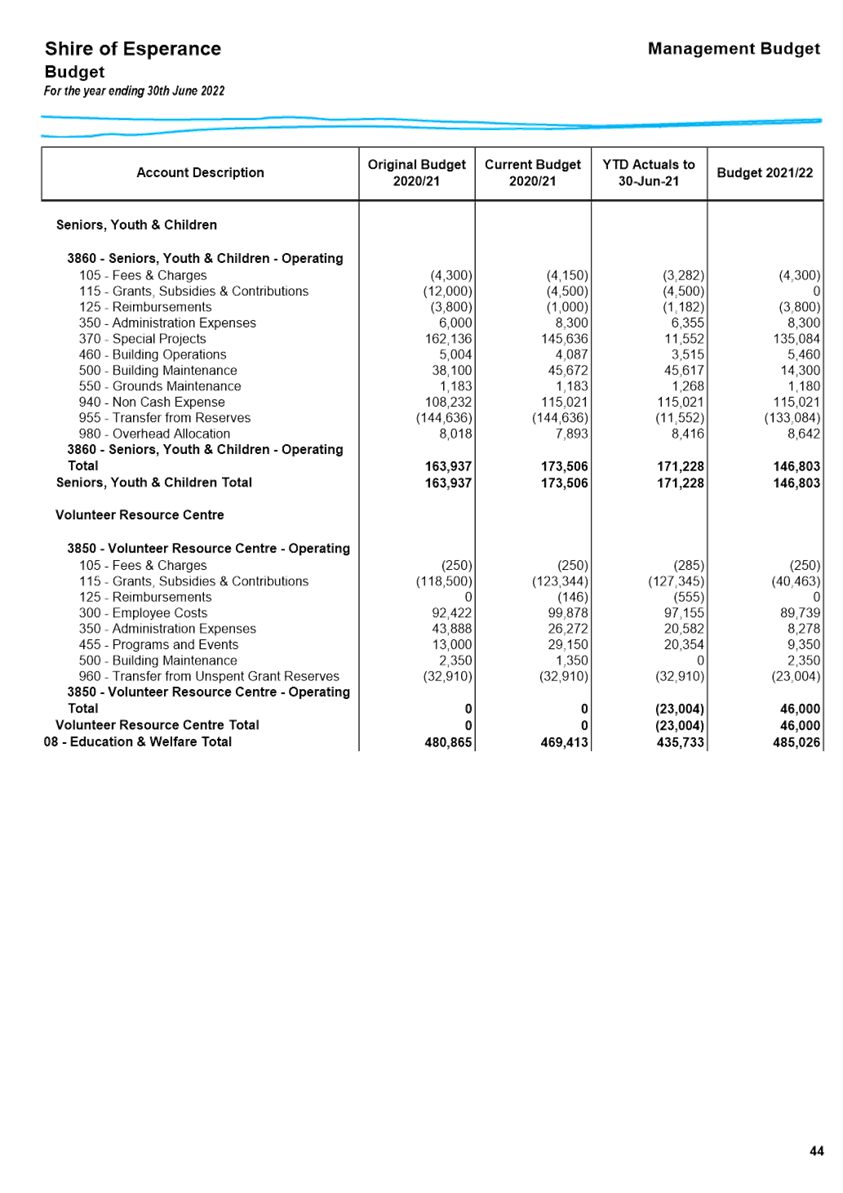

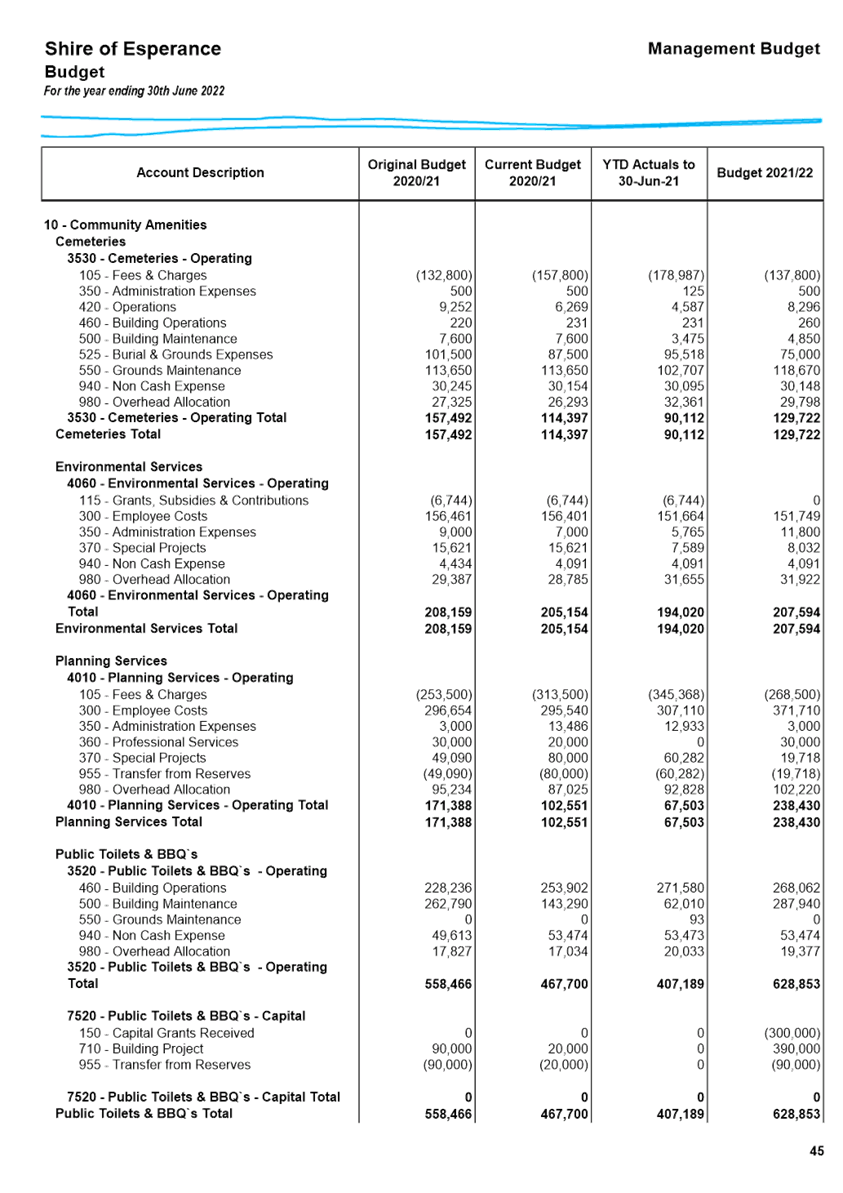

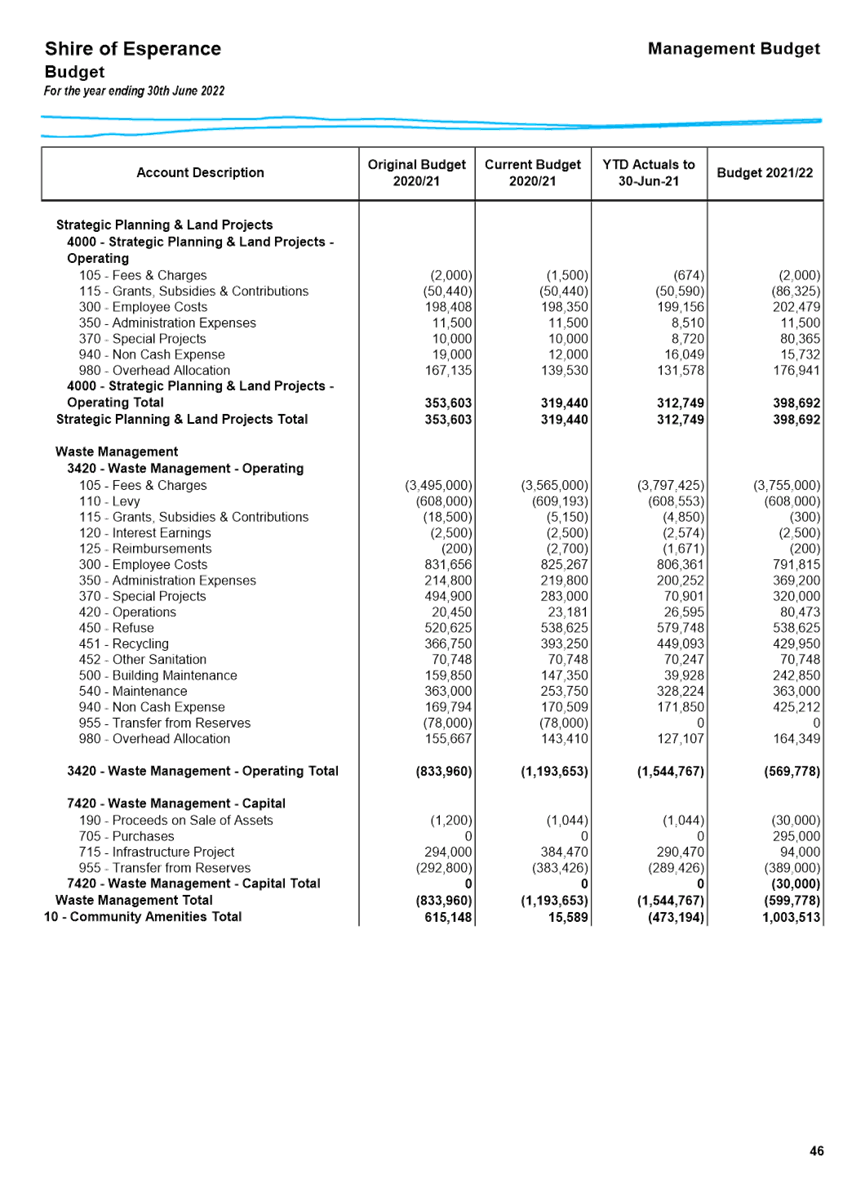

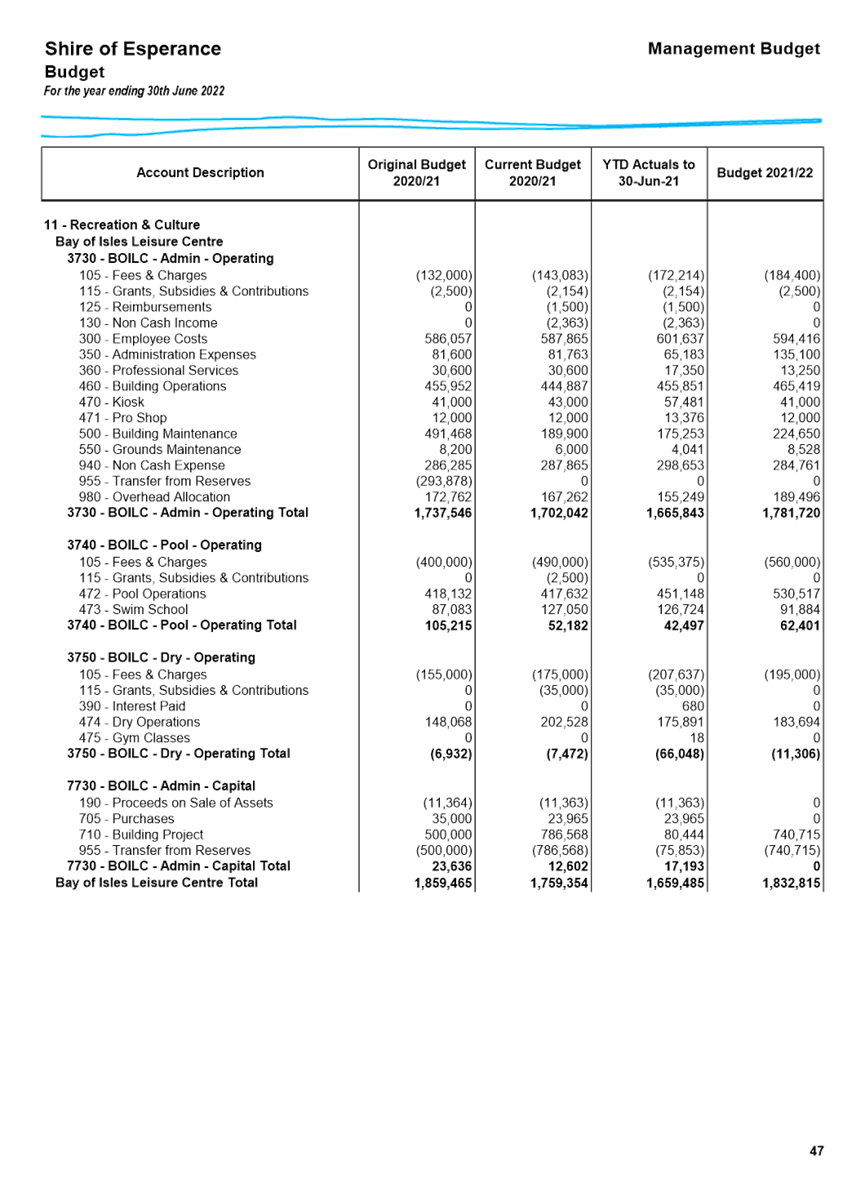

Executive Summary

To present to Council the 2021/2022 Annual Budget for

formal adoption.

Recommendation in Brief

That Council adopt the Statutory Budget and supporting

documents along with rate parameters, fees and charges, reserve movements,

proposed borrowings and waste rate for the 2021/2022 financial year.

Background

This year the process for considering and adopting the Annual

Budget involved a number of draft budget workshops and project briefings. The

merits of these recommendations have been discussed and a direction sought from

the Council as to the final items to be included in the formal budget prepared

for adoption.

The consideration of the parameters that were agreed during

the Draft Budget Workshops do not constitute the final statutory adoption of

the budget due to the format in which it was presented. The statutory format

required by the Local Government Act 1995 and Local Government and

Financial Management Regulations 1996, is quite different from the management

format provided to Councillors during the draft budget workshops. The proposed

budget as discussed and considered during the draft budget workshops is a

balanced budget.

As a result of queries raised

at the Annual Meeting of Electors on the 9th of February, via motion

2 of the minutes of the meeting, Council instructed the CEO to advise on the

impacts considered when setting the Rates for the 2021/22 Annual Budget. At the

time CPI was quoted at 0.7%, and impact of COVID-19 on projects and the rate

freeze was raised. During the Budget Workshops with Councillors, considerable

effort was made to keep any Rate increase to a minimum.

On Monday, 31 May 2021 the WA

State Government announced its intention to hand down the State budget in

September. They confirmed then that core components of the state budget

will include an inflation rate increase of 1.75%. There were no indications of

continuing all of the restrictions experienced during the COVID budget

decisions of 2020/21, including any freeze on Rates. In contrast street light

tariffs were foreshadowed to increase greater than 5.9% on average.

WALGA’s latest base

case forecasts indicate that the LGCI is expected to grow by 3.2% in 2021-22,

and 2.8% in 2022-23, driven by higher construction costs for roads and bridges,

non-road infrastructure and non-residential buildings. Key factors taken

into consideration in this budget include key local issues and

experiences. For example, growing reports of skilled labour shortages,

particularly with border closures that have limited the ability to access

broader pools of skilled labour. In addition, reports indicate

constraints on building materials and supplies, such as timber and steel,

particularly in light of the increased demand generated by “stimulus

projects”. (source: WALGA Economic Briefing June 2021). Commencing

July 2021, the Superannuation Guarantee will increase by 0.5% to 10%. For

these economic reasons, with contingency for the pressures of inflation Council

have made earnest measures to minimise the increase in Shire Rates to 3%,

whilst returning to pre COVID service delivery initiatives.

In these budget

considerations, there has been no attempt to “catch-up” on forgone

revenue and or deferred projects. The Long Term Financial Plan had

factored an approximate annual increase of 1.75% approximately $375k, as an

initiative to close the asset management gap over a 10 year period. With

the anticipated increases in materials and contracts again the initiative to

close the gap has been postponed in the 2021/22 budget proposed.

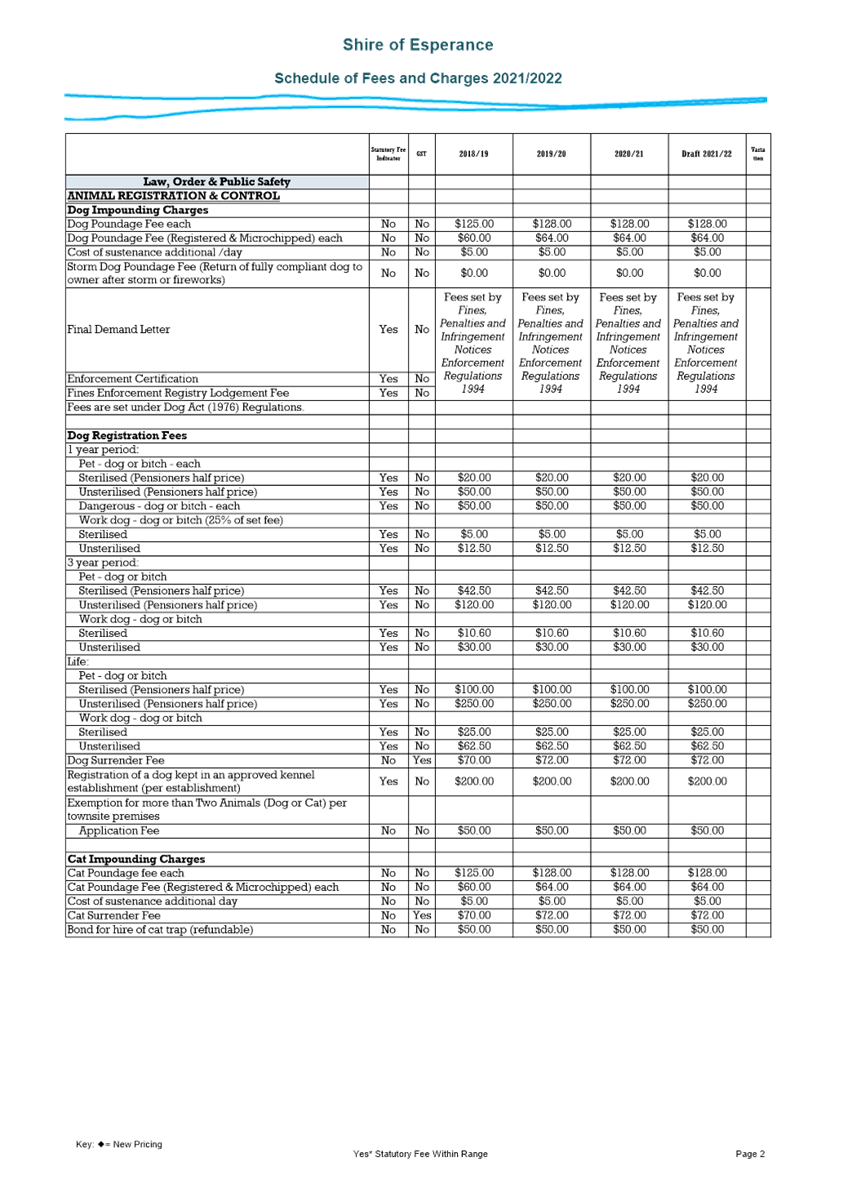

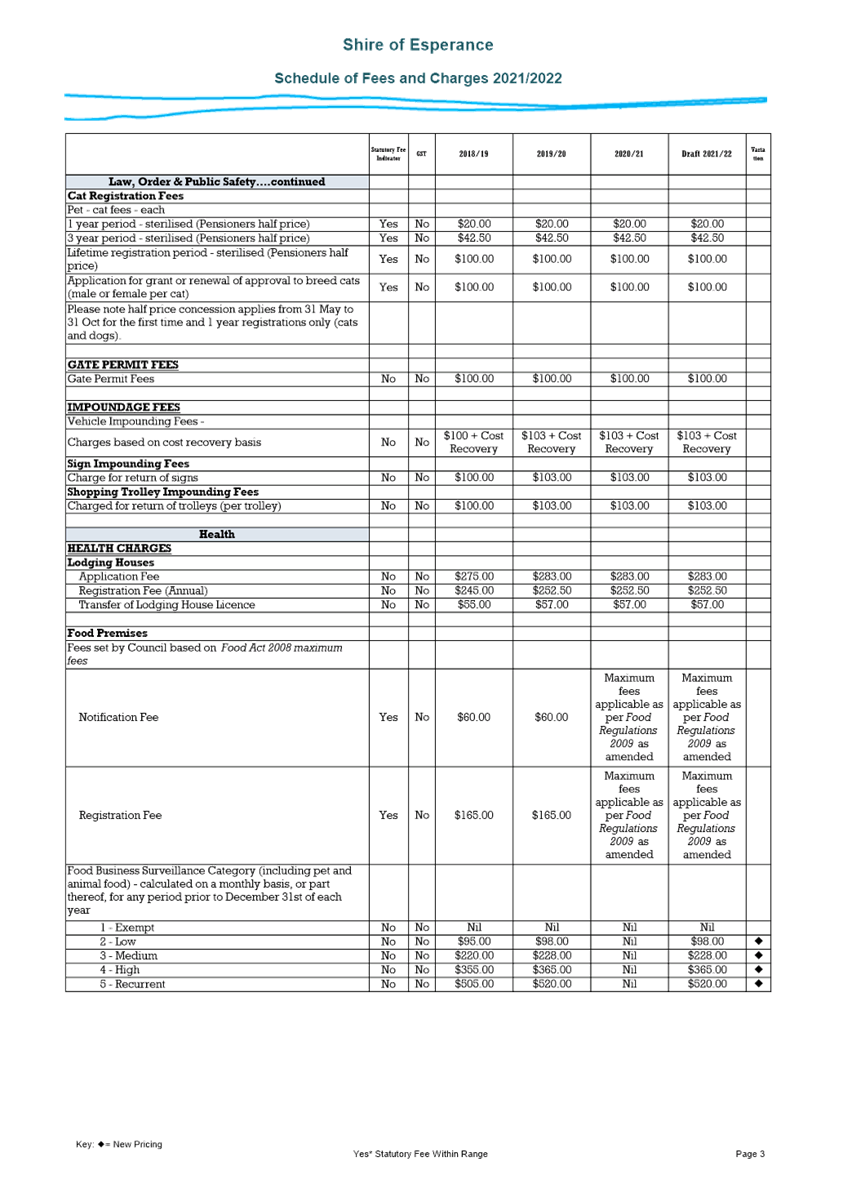

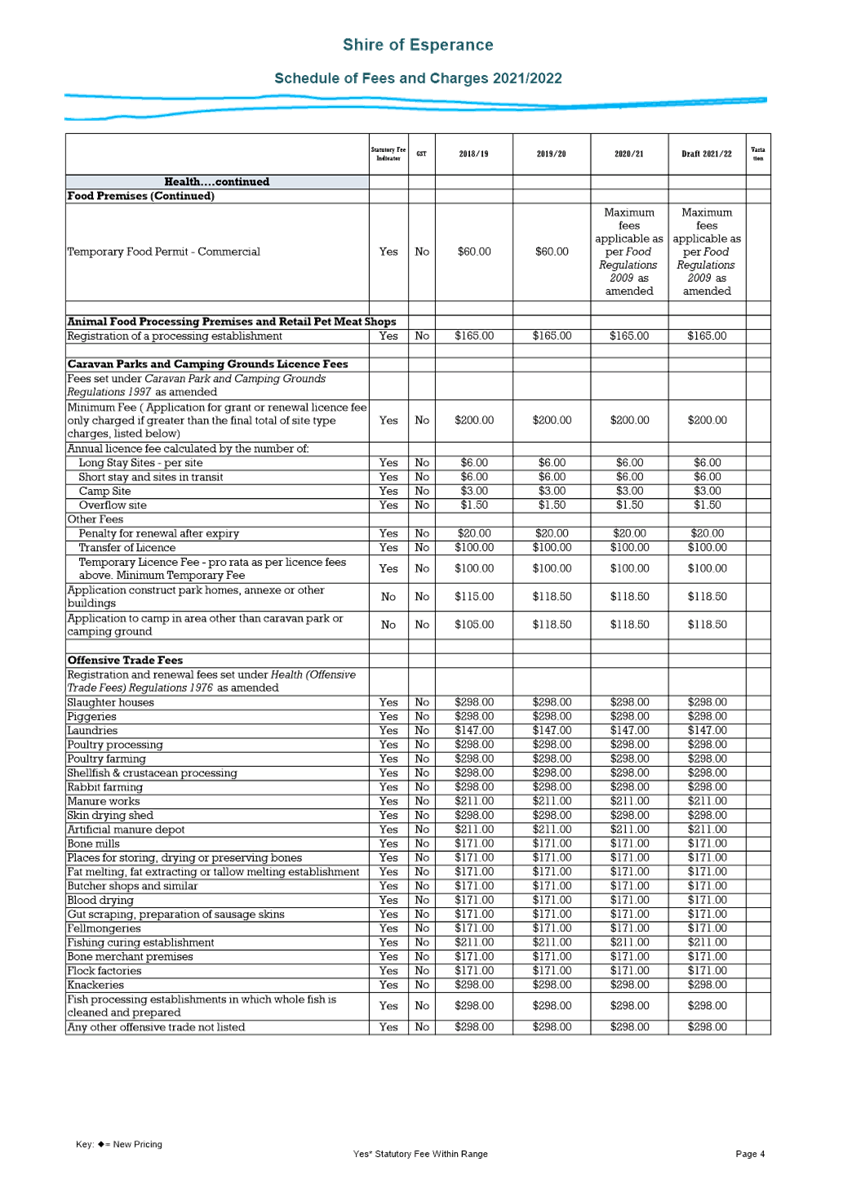

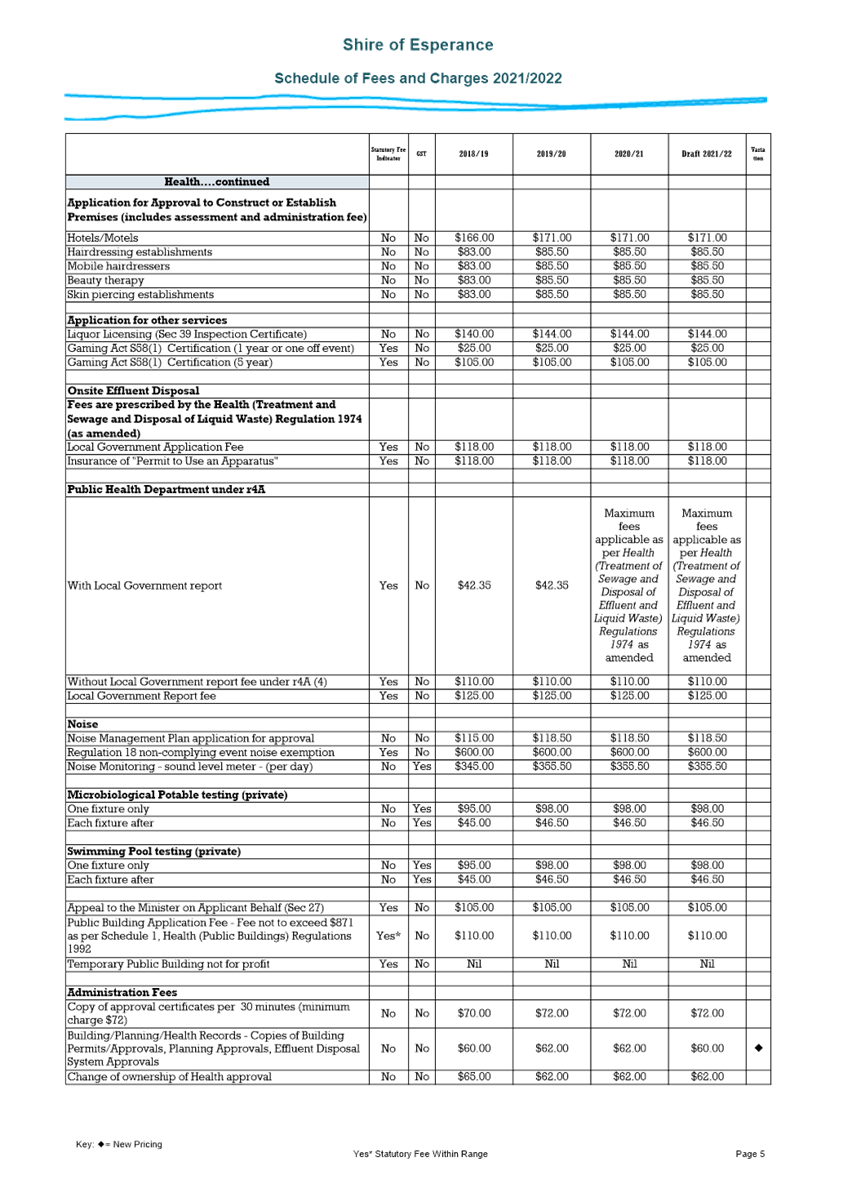

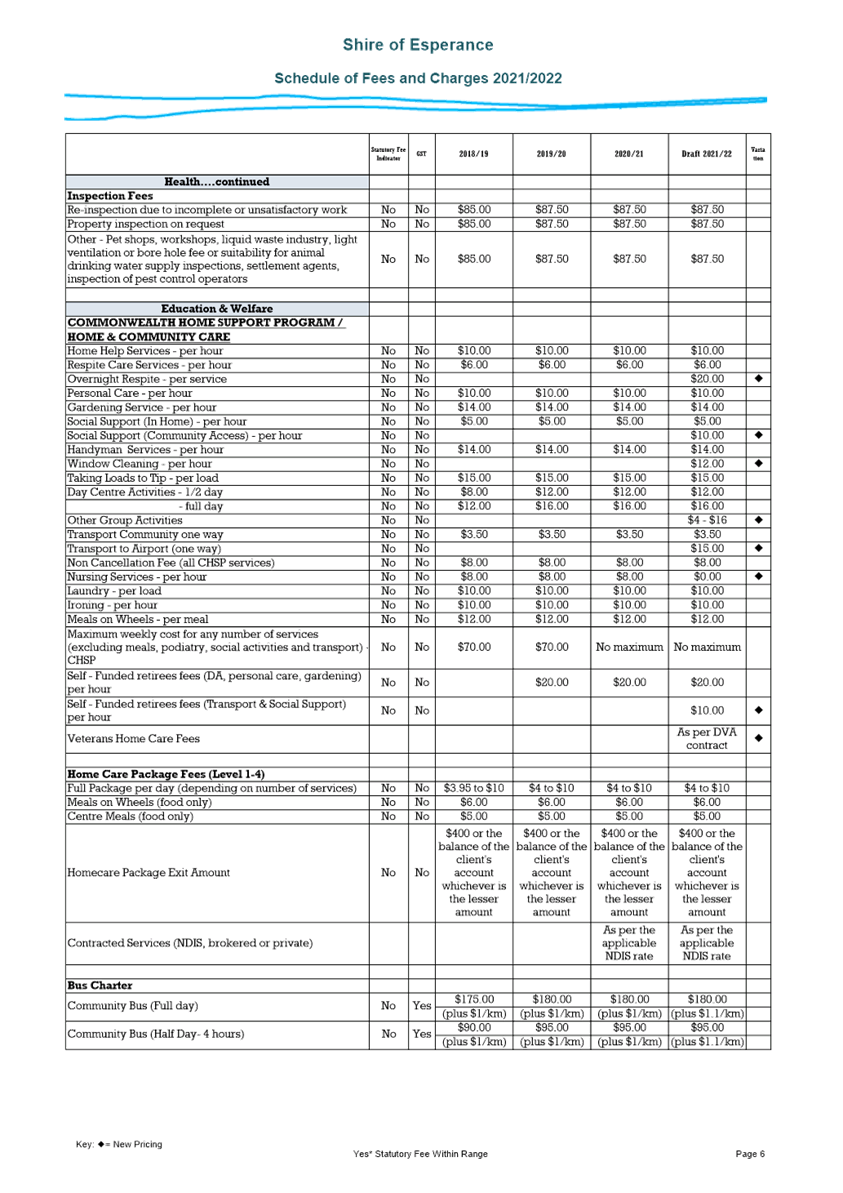

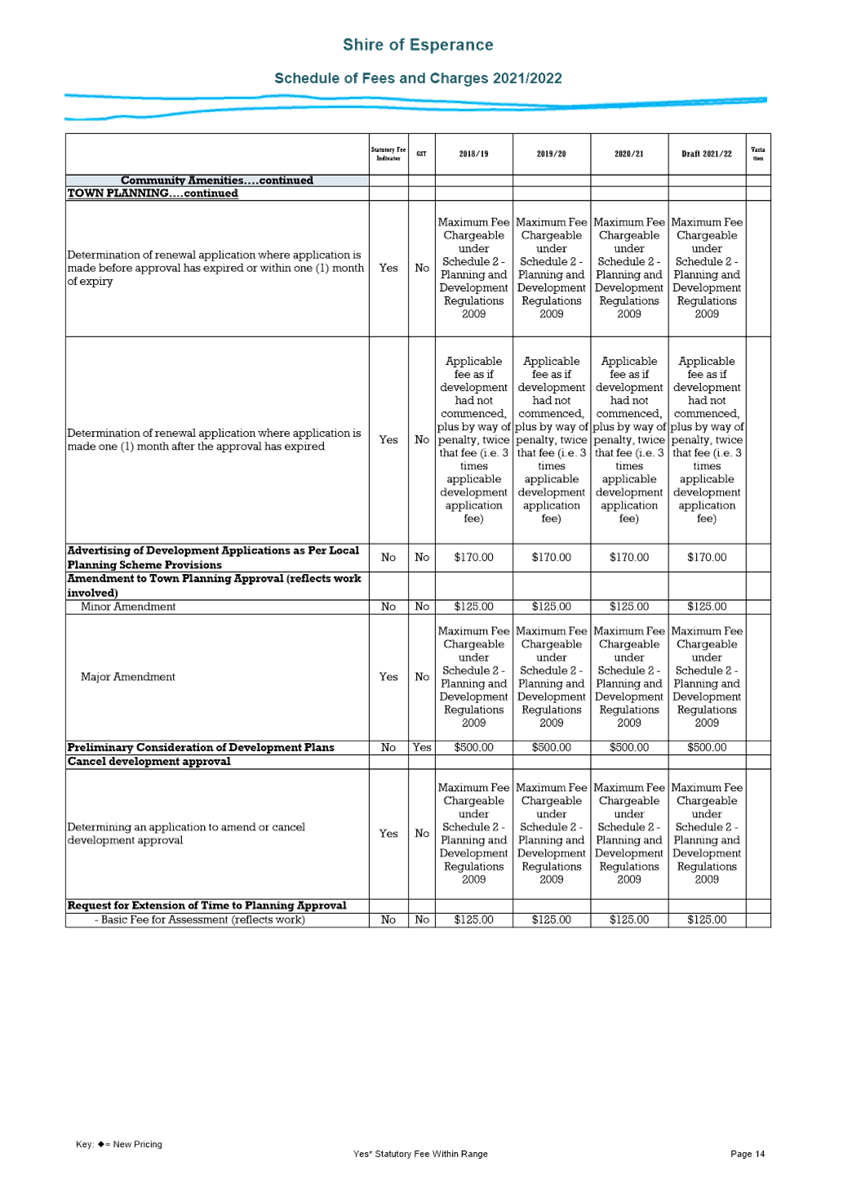

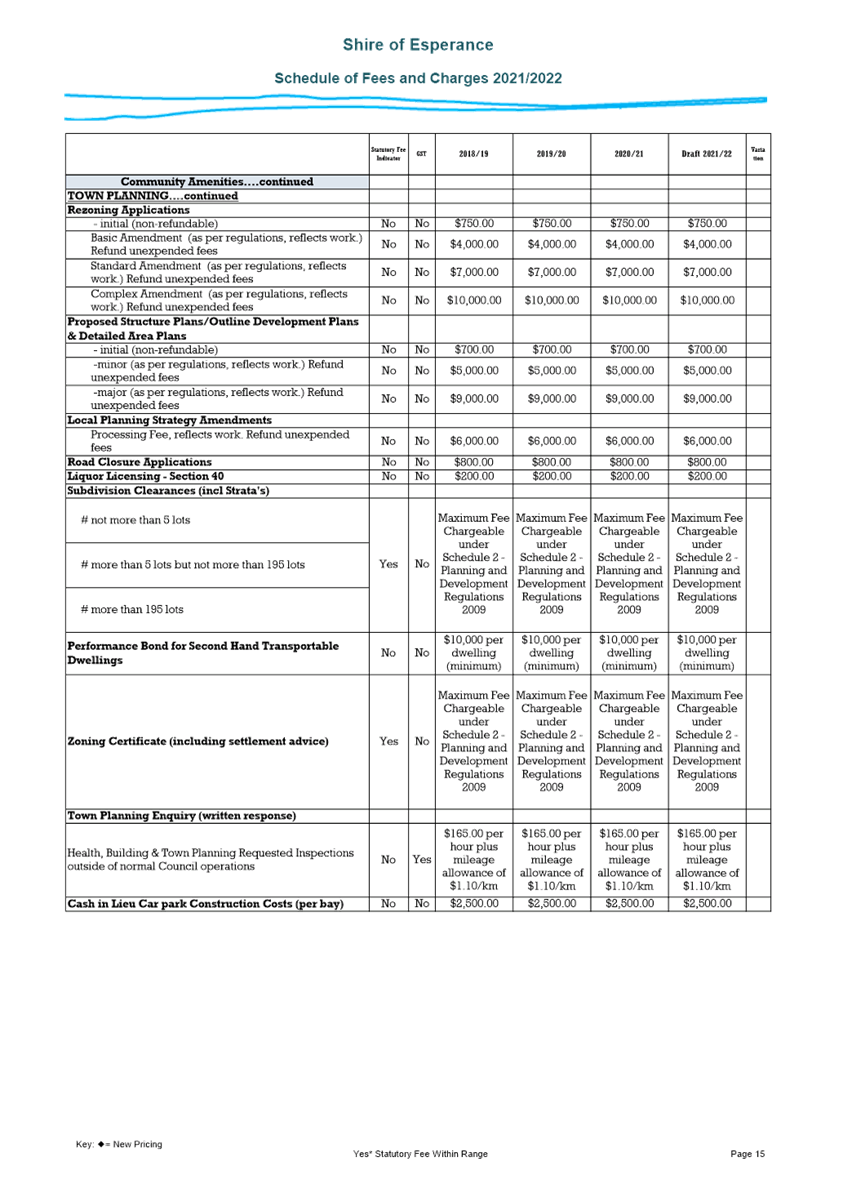

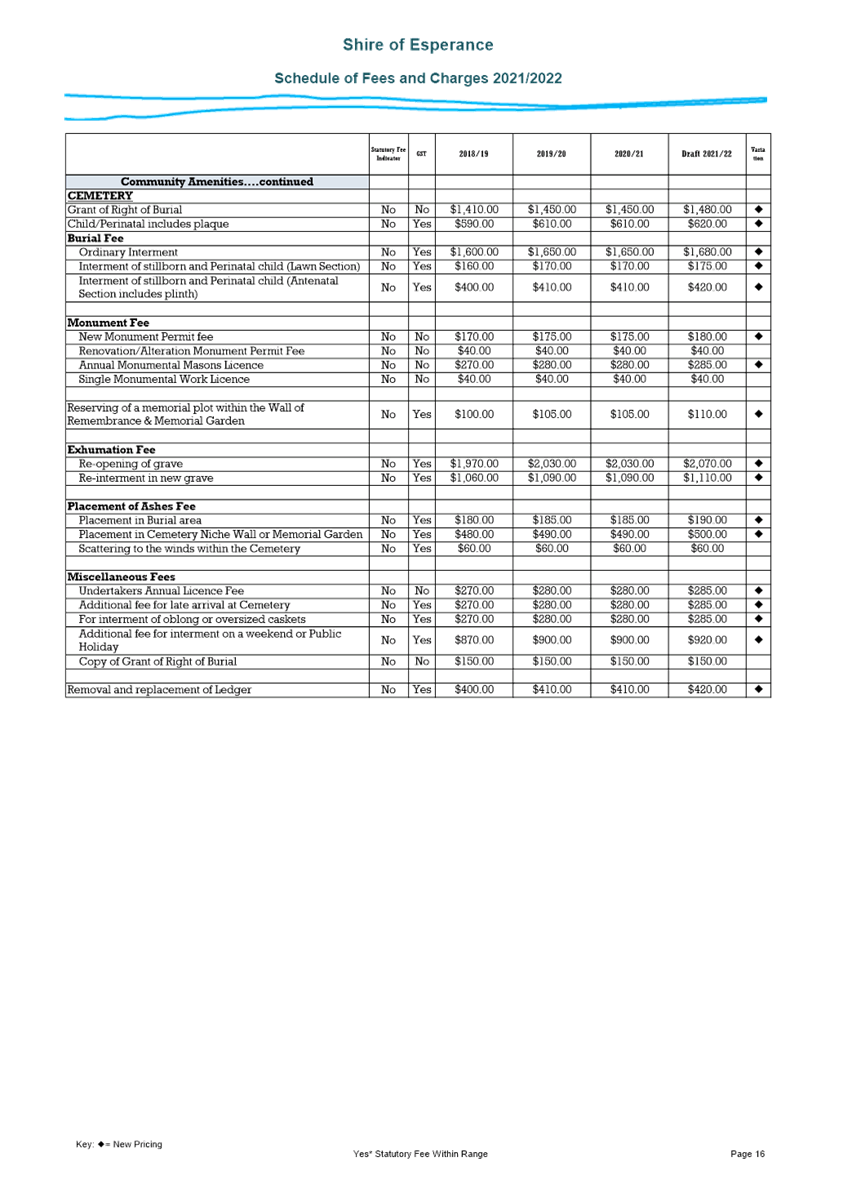

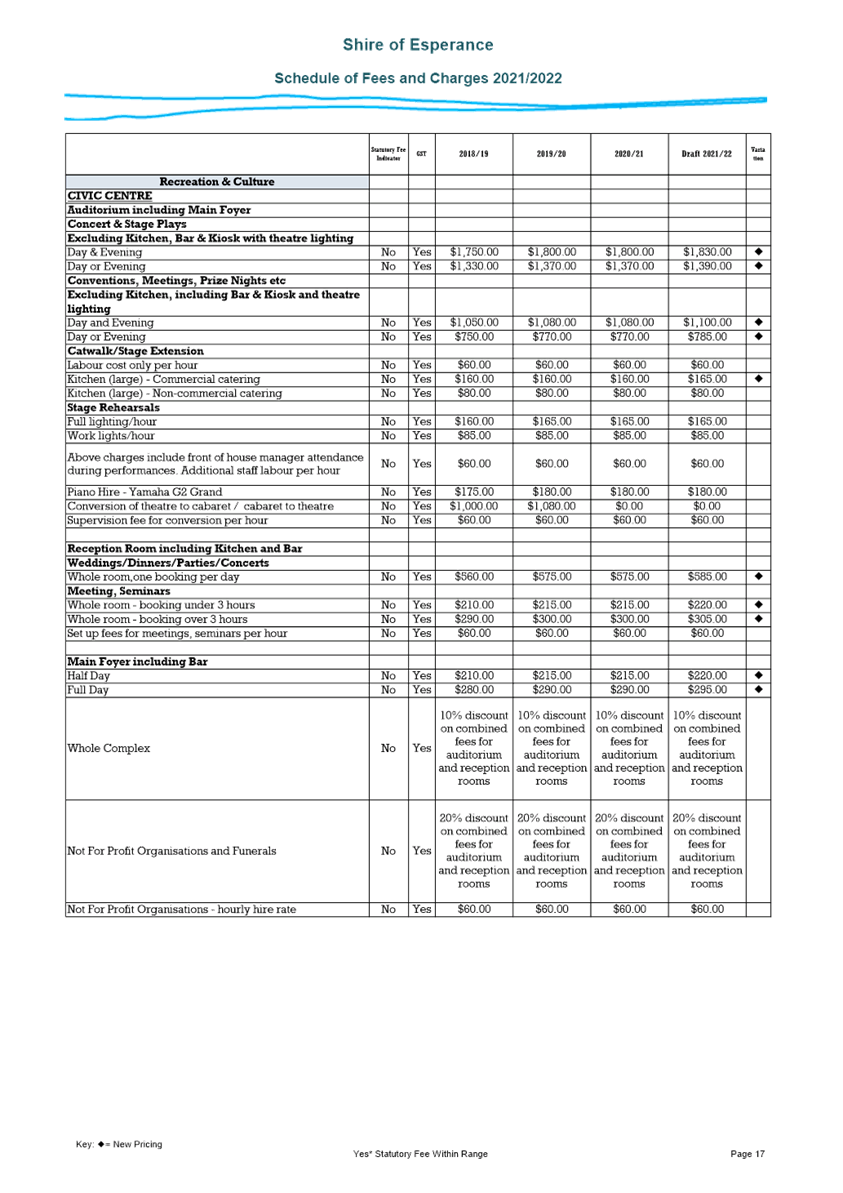

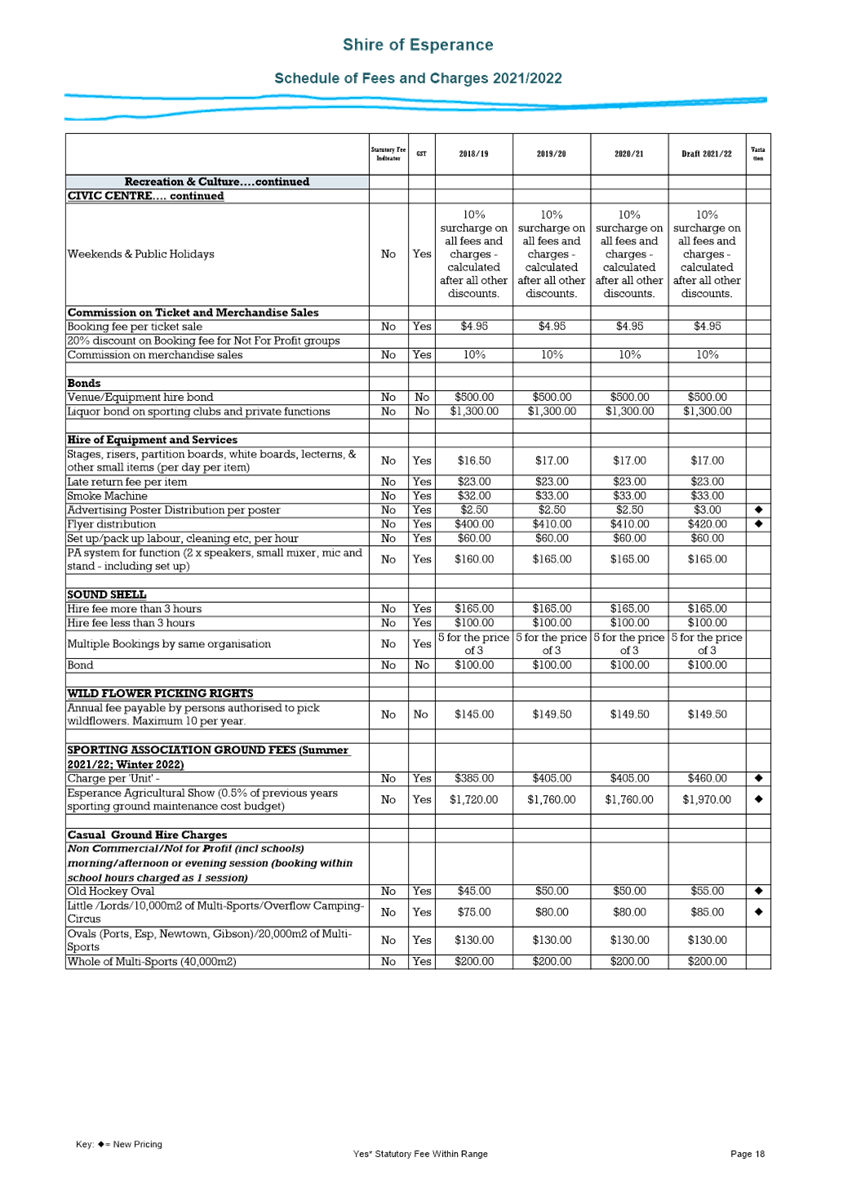

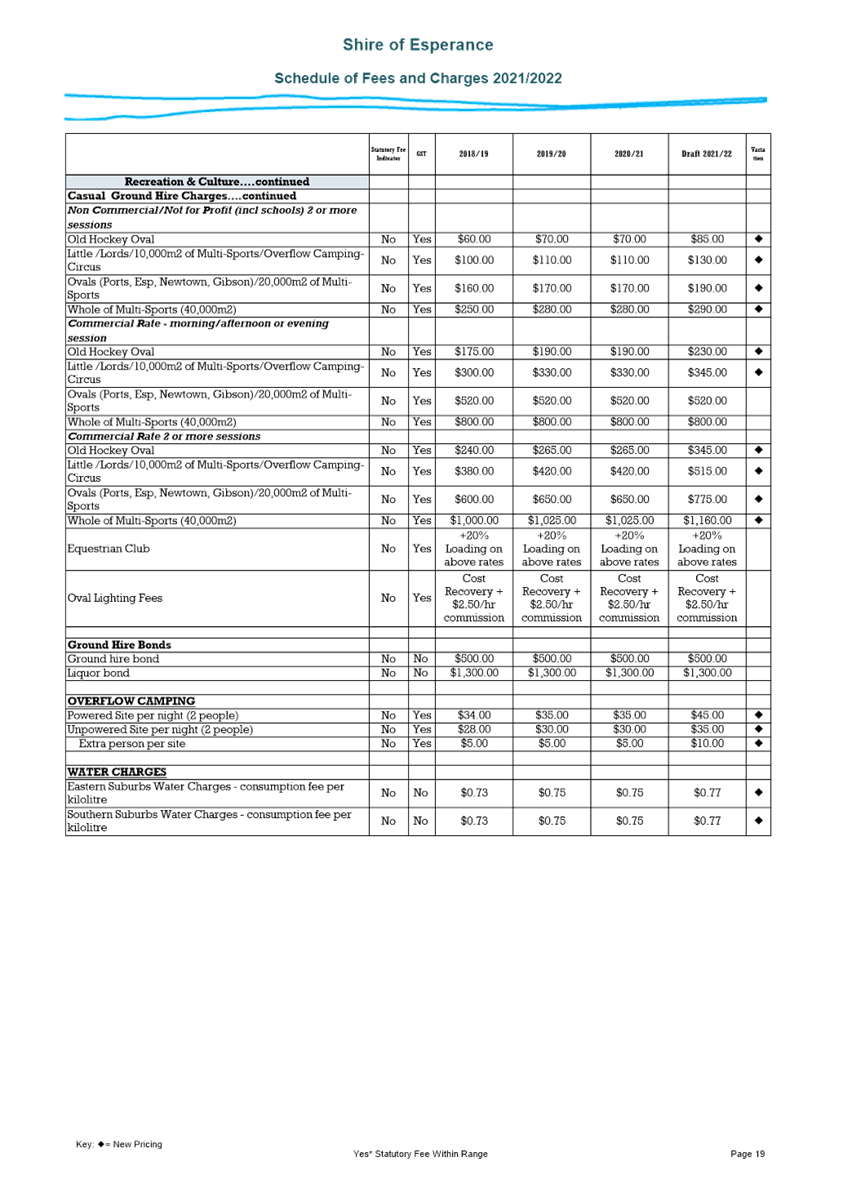

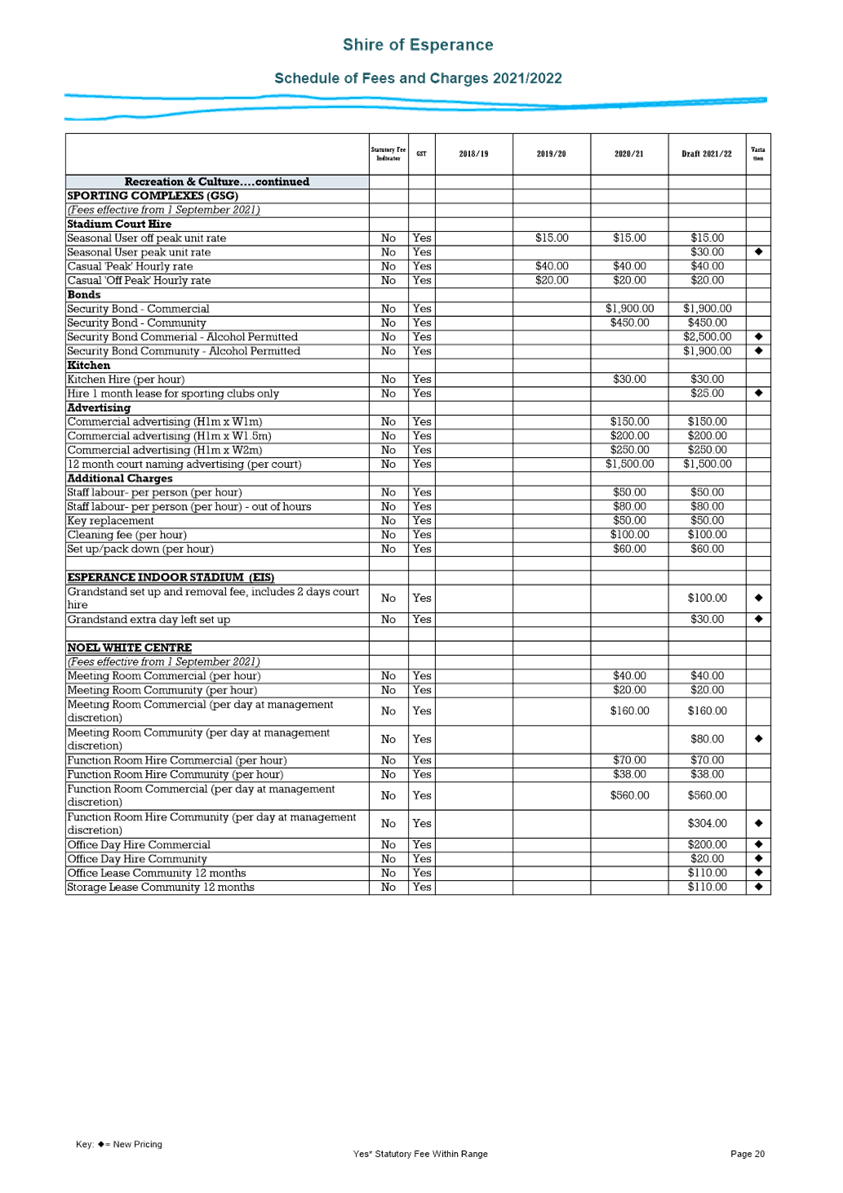

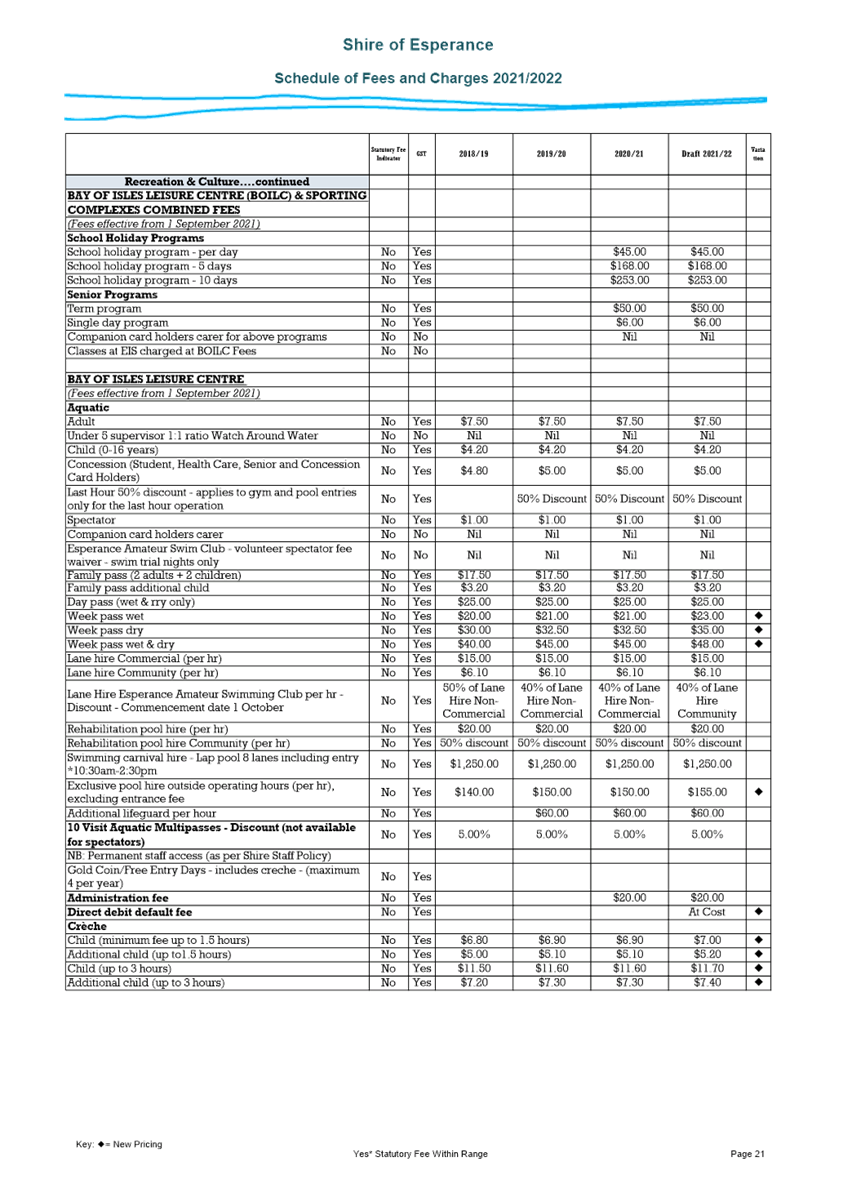

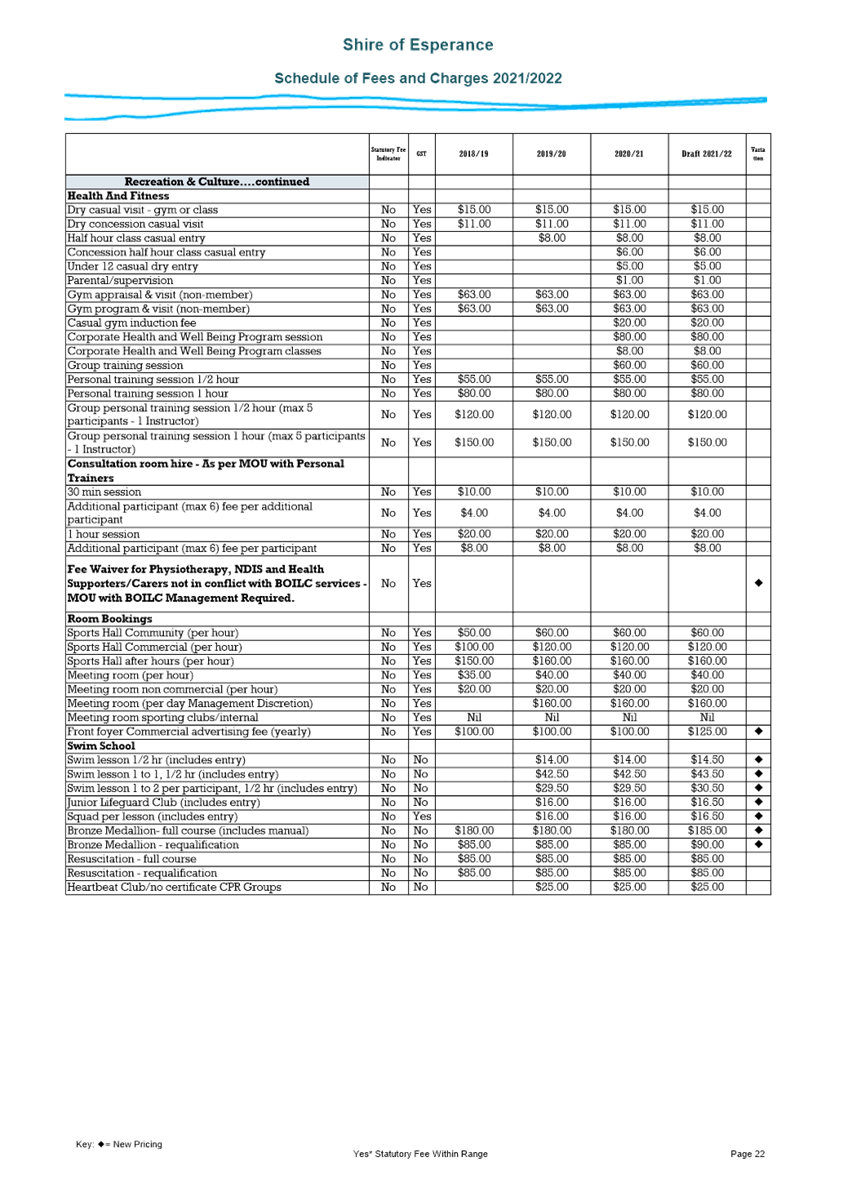

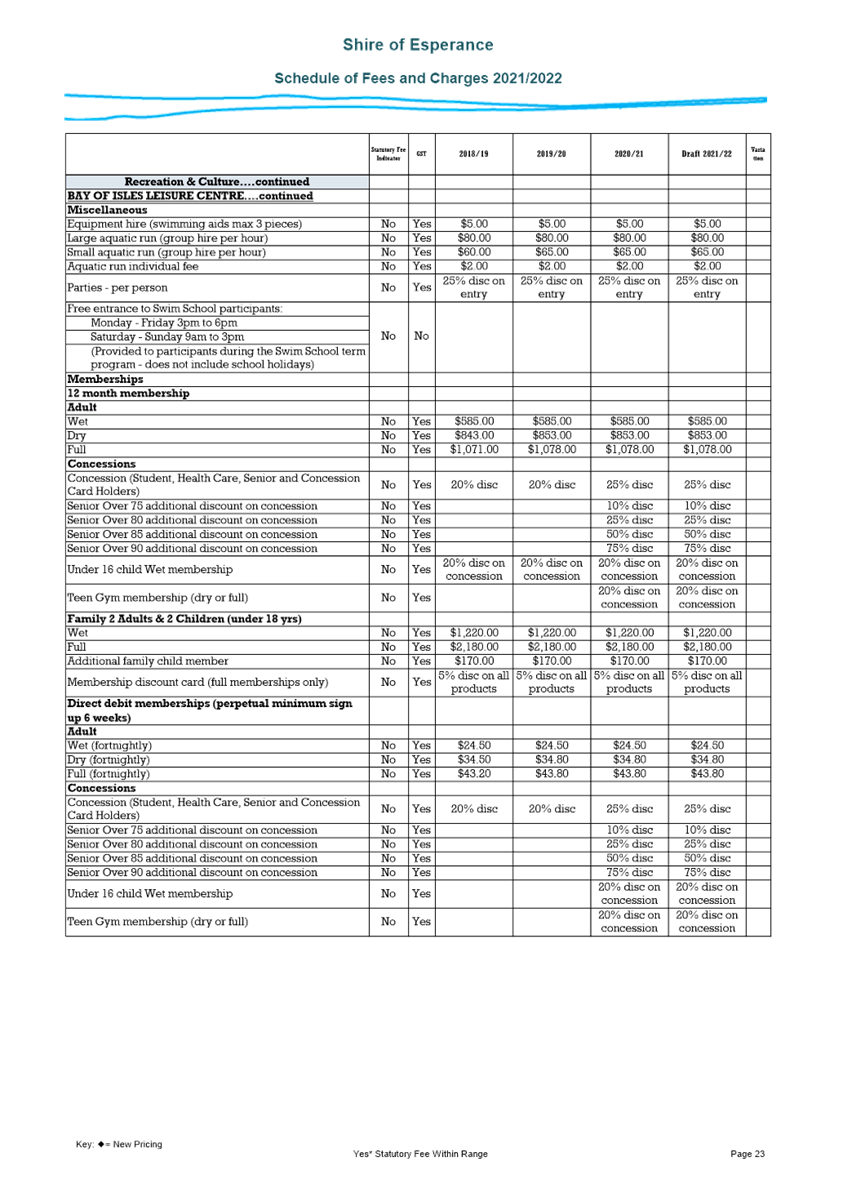

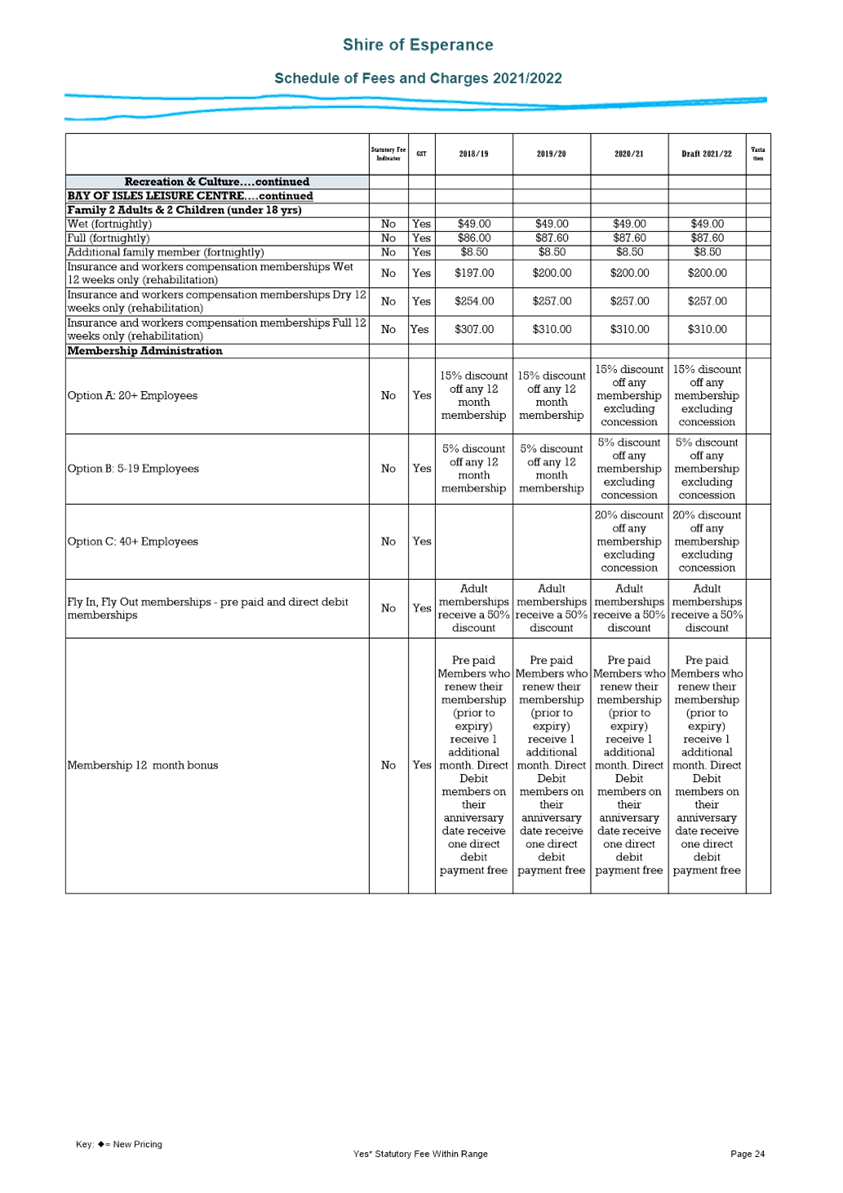

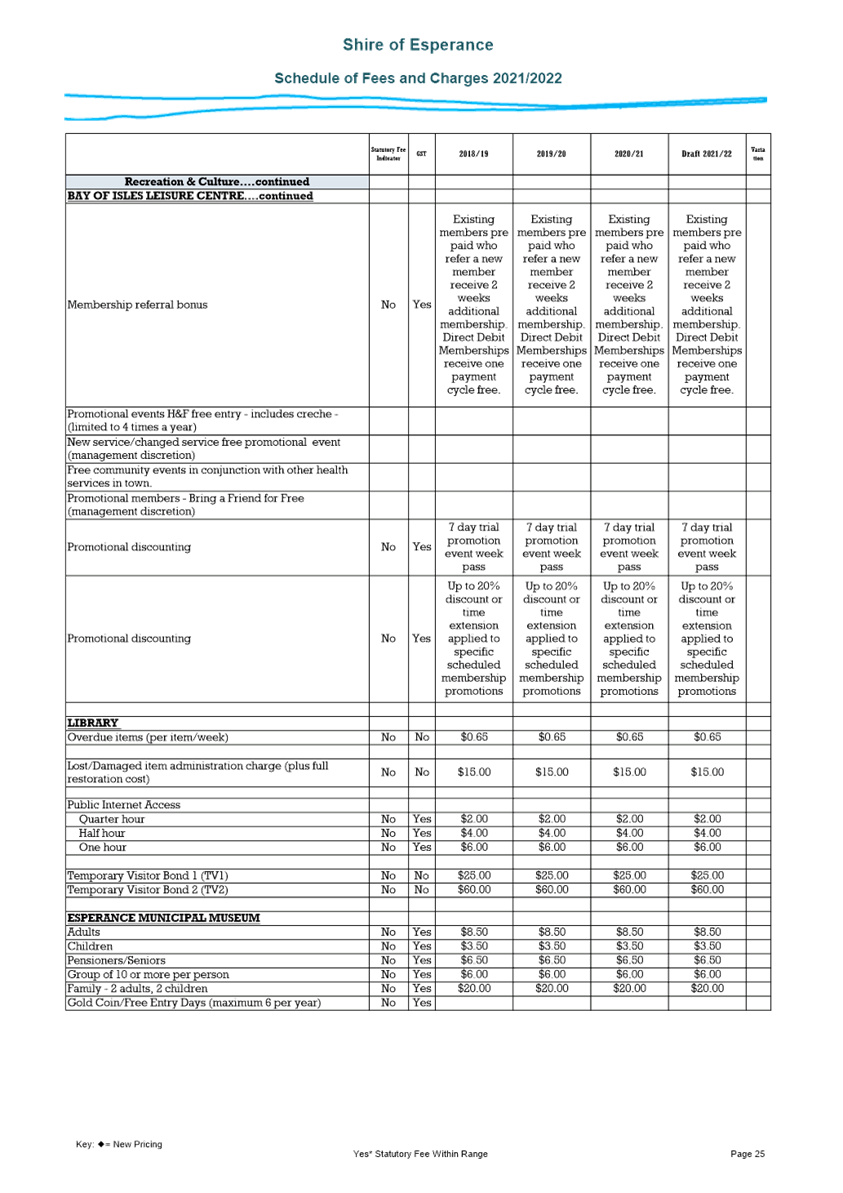

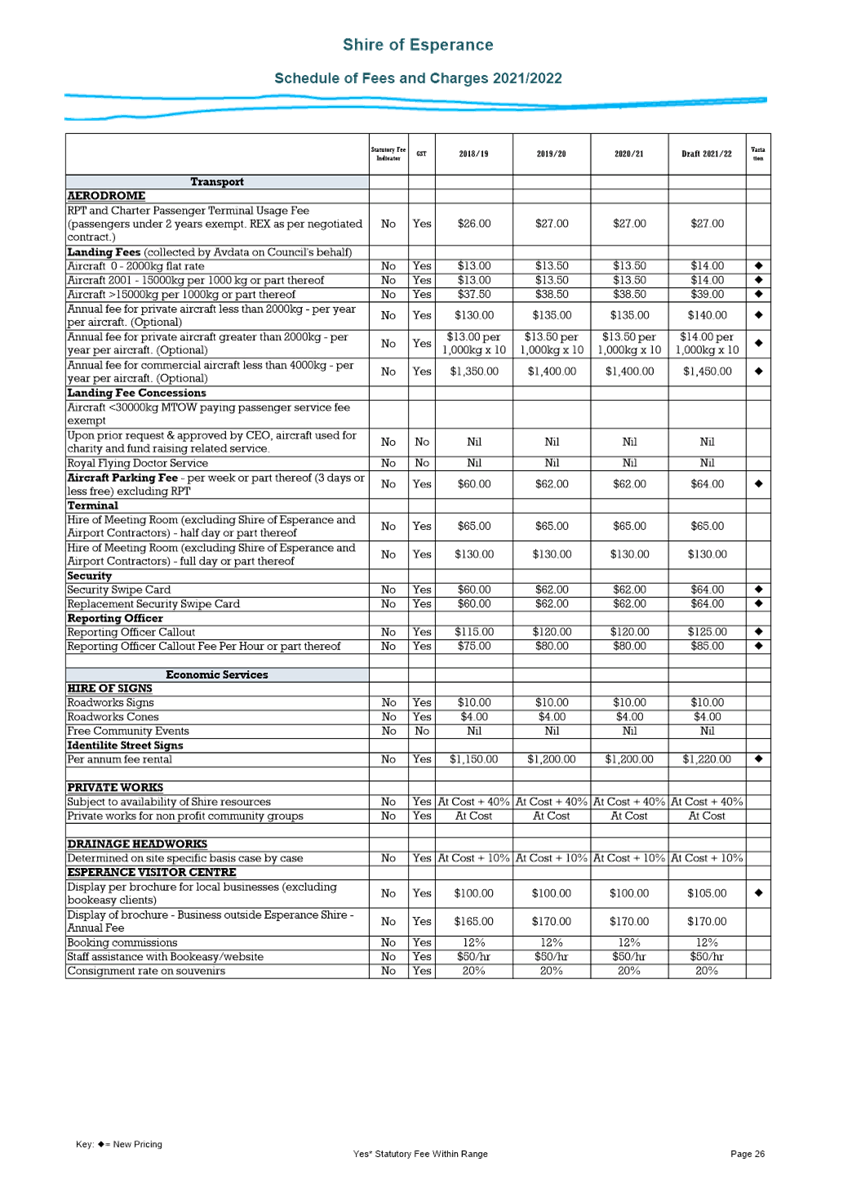

Fees and Charges were also

considered by the Council on the 25 May 2021 with the draft fees and charges to

be included with the budget adoption. Since 25 May 2021 when Council considered

the Fees and Charges there have been no significant changes. The new fees

and charges will become effective with the adoption of the budget except for

Bay of Isles Leisure Centre where the fees will be effective from 1 September

2021.

After the draft budget workshops, staff finalised the

accounts for the end of the previous financial year and now present the budget

in the official statutory format ready for adoption. Since the conclusion of

the draft budget workshop a full time Aviation Refueller Officer has been

included in the budget, being funded from the Airport Reserve. This position

will provide refuelling services at the airport as Australian Flight Handling

services have terminated their service contract with Air BP. Discussion with

Council has also resulted in placing budget allocations to provide an in-house

service using Shire staff and equipment.

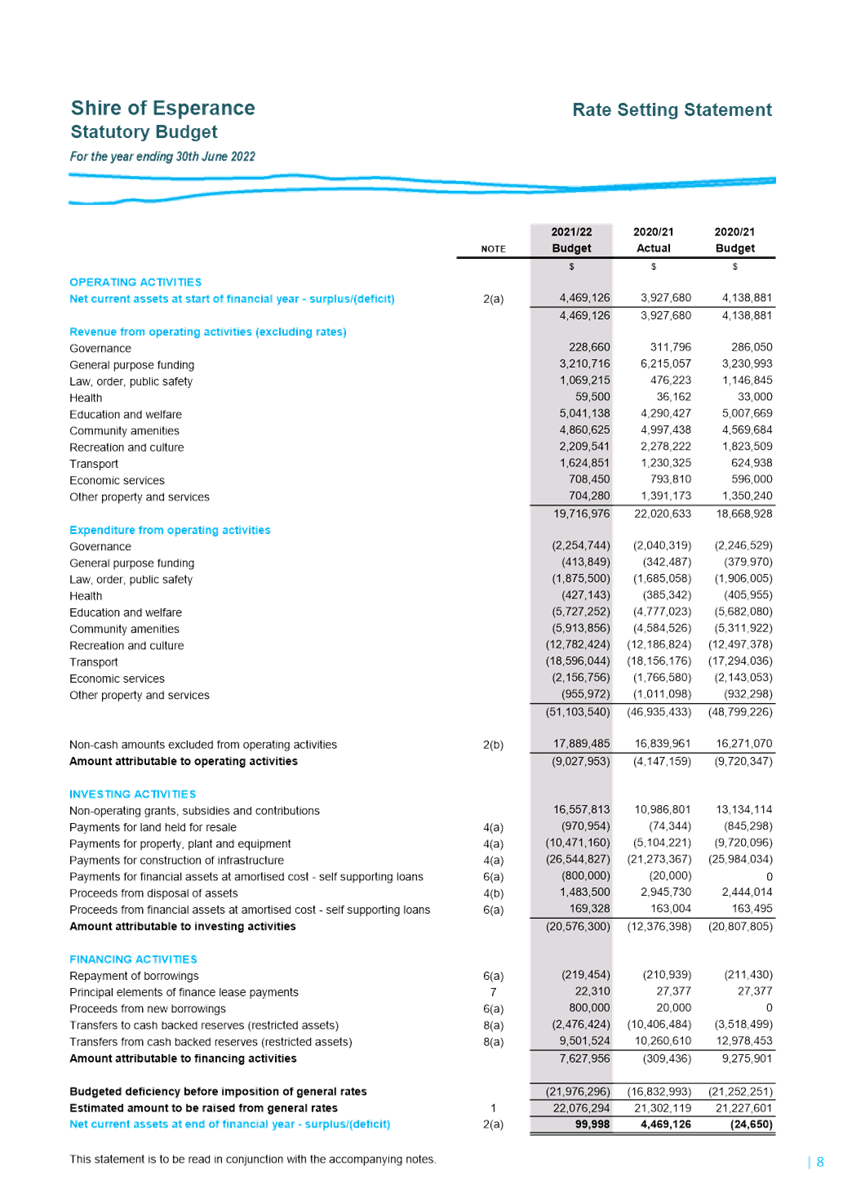

After completing all the necessary adjustments as at 30th

June and completing Reserve Transfers, the predicted closing position for the

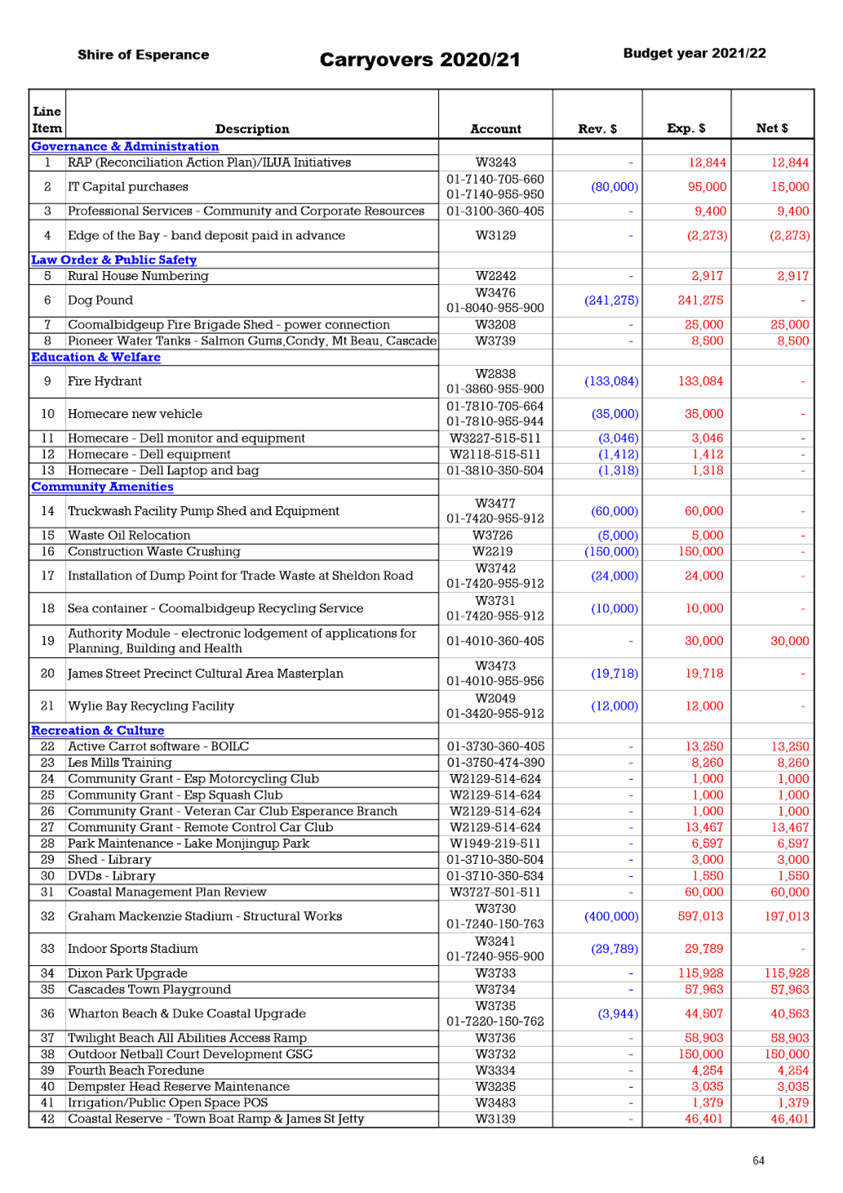

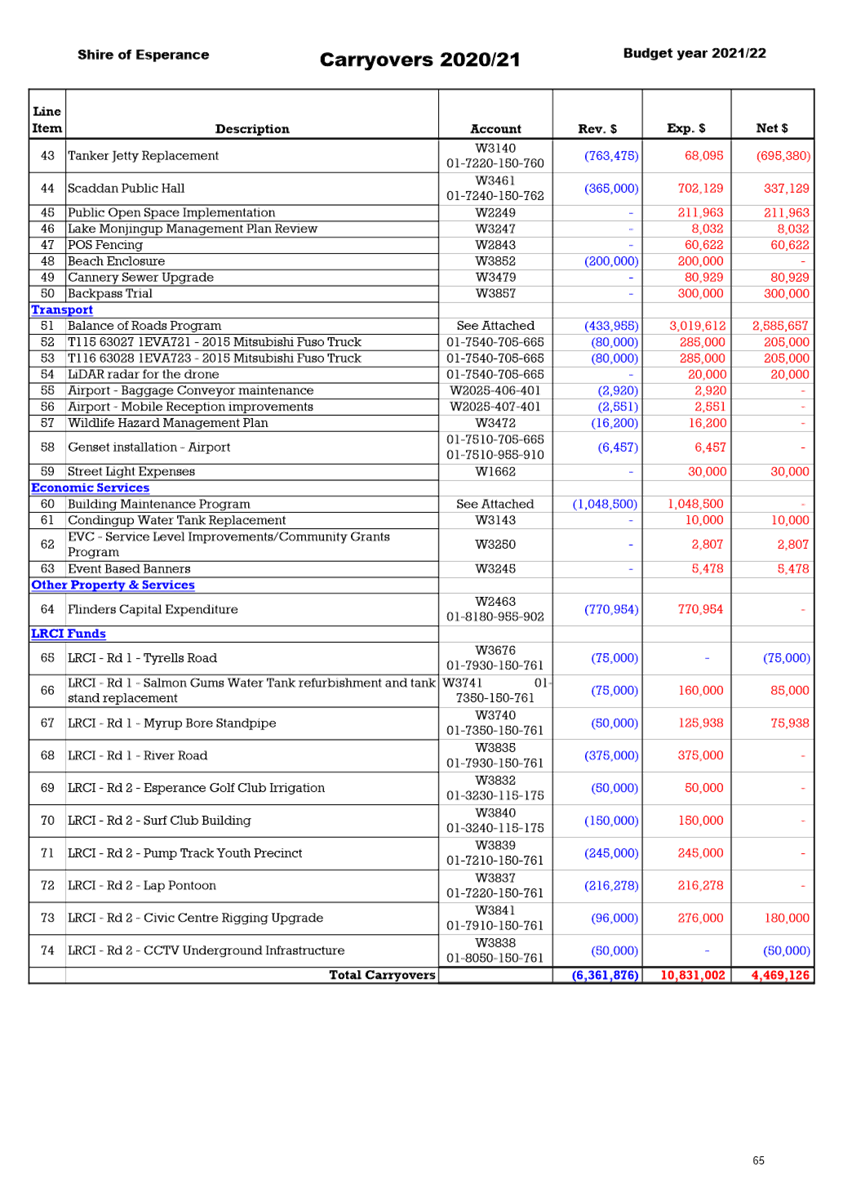

2020/21 year is $4,469,126. This is the total of the carryover projects and

have consequently been re-budgeted into the 2021/22 year.

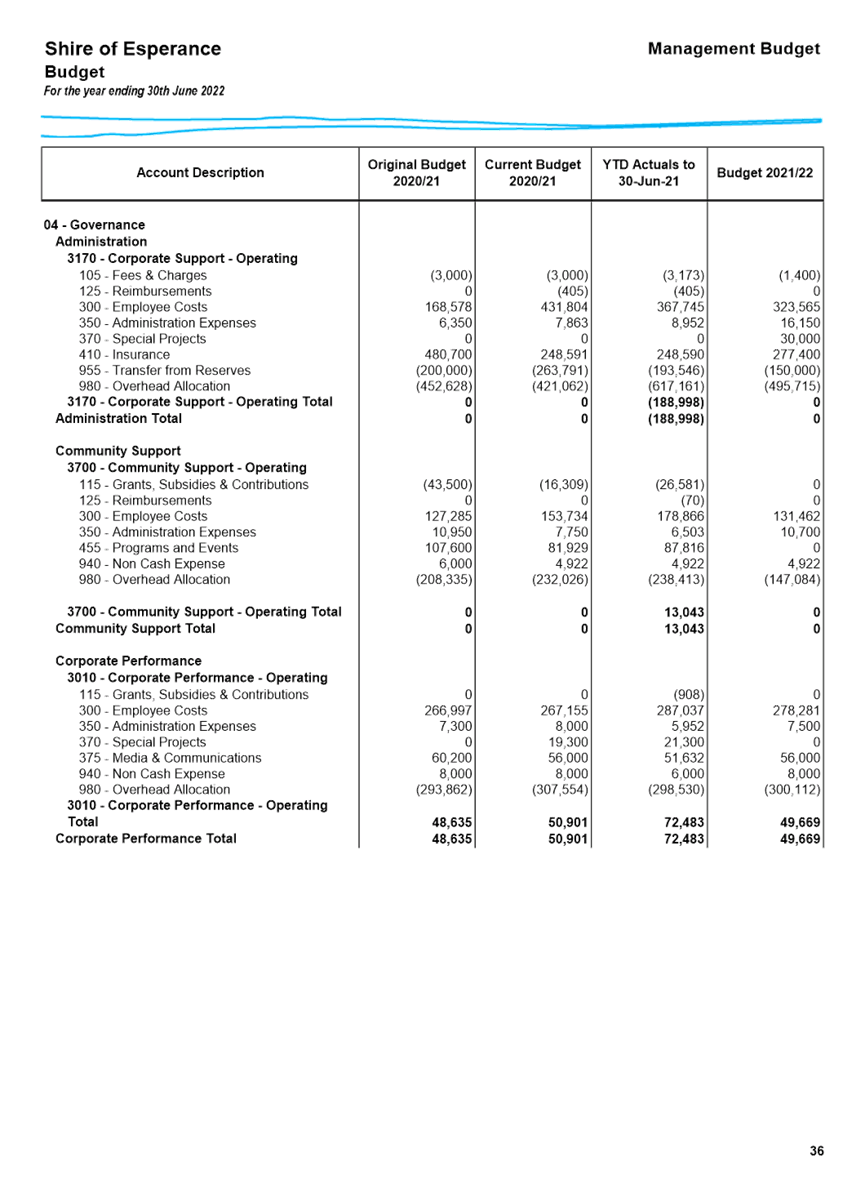

Officer’s Comment

The preparation of this budget is in

line with the adjusted 2020/21 Budget with estimated inflationary increase of

2% to accommodate some services as required for the 2021/22

year.

The opening “cash” position

(net of unexpended grants) carried forward into the 2021/22 budget is a surplus

of $4,469,126. In

adopting the budget, there always remains the possibility that the opening

balance may need adjusting as not all figures may have been processed by the

adoption date or the Shire’s auditors may require some final adjustments

prior to finalising the 2020/21 financial statements. If this occurs,

corrections will be reported during the Budget Review process or an additional

agenda item to Council if required.

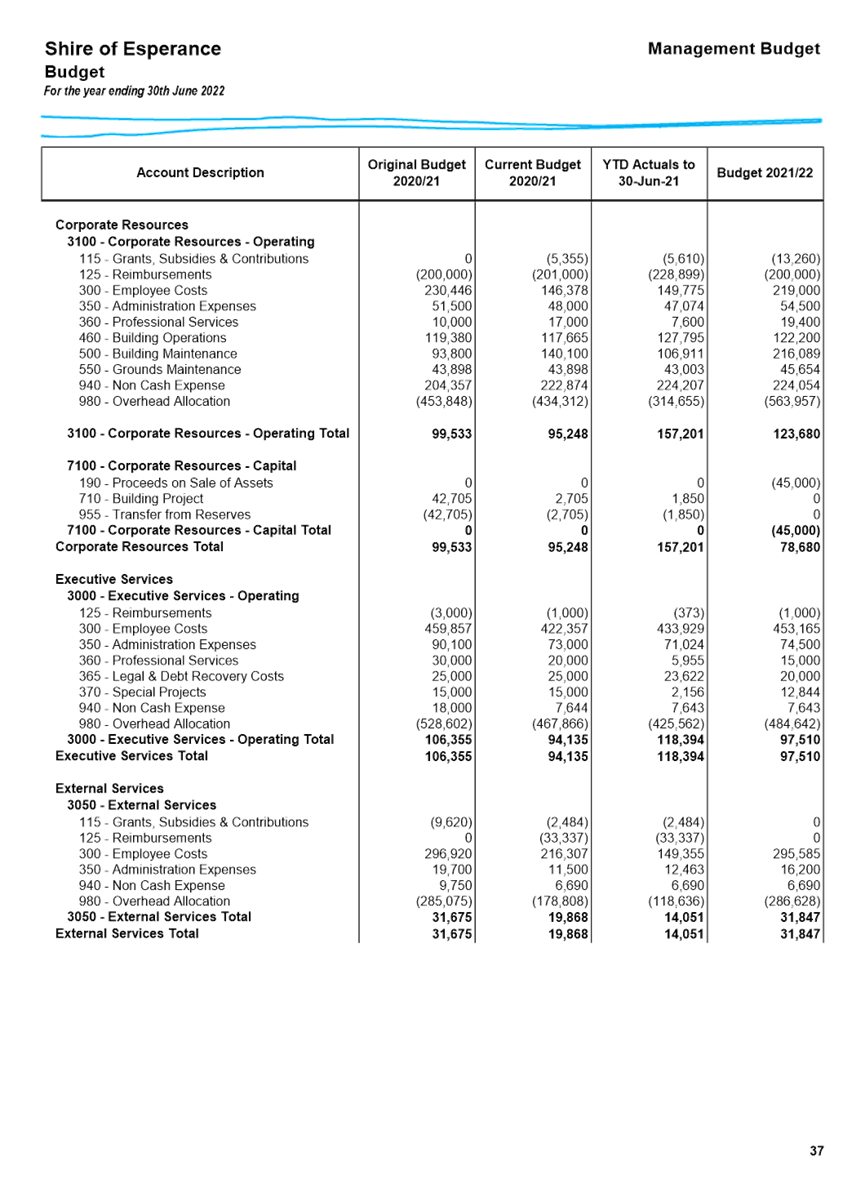

In reaching the end of year position

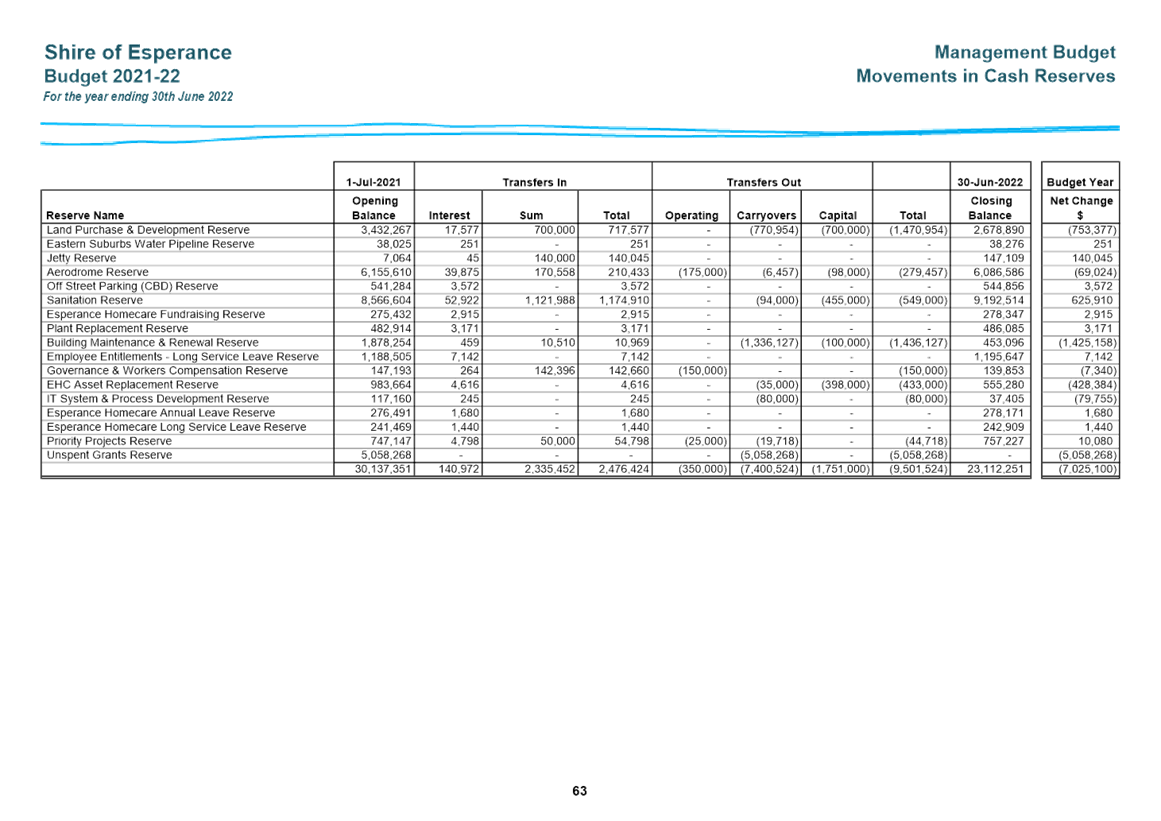

the annual reserve movement reconciliations have been performed for the

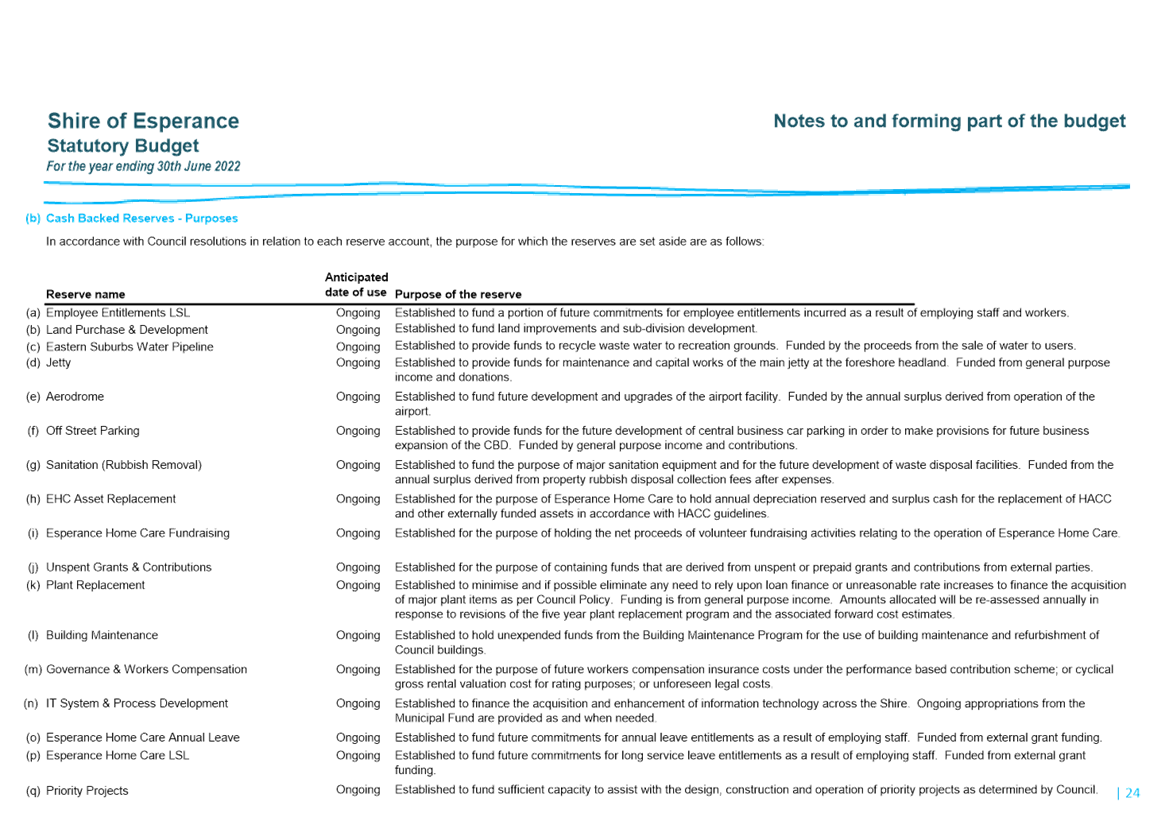

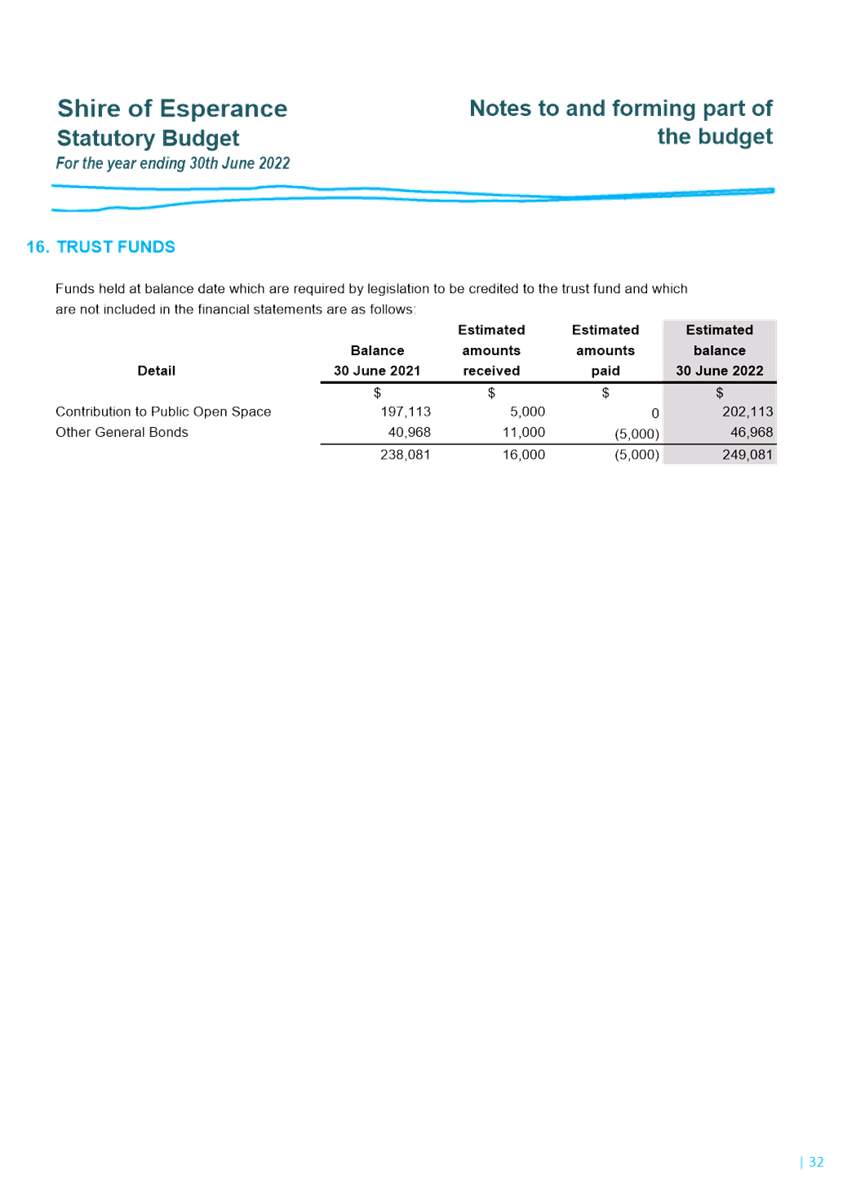

Sanitation, Aerodrome, HACC, IT System Development, Jetty, Governance Support,

Unspent Grants, Plant, Land Purchase and Development, Priority Projects and

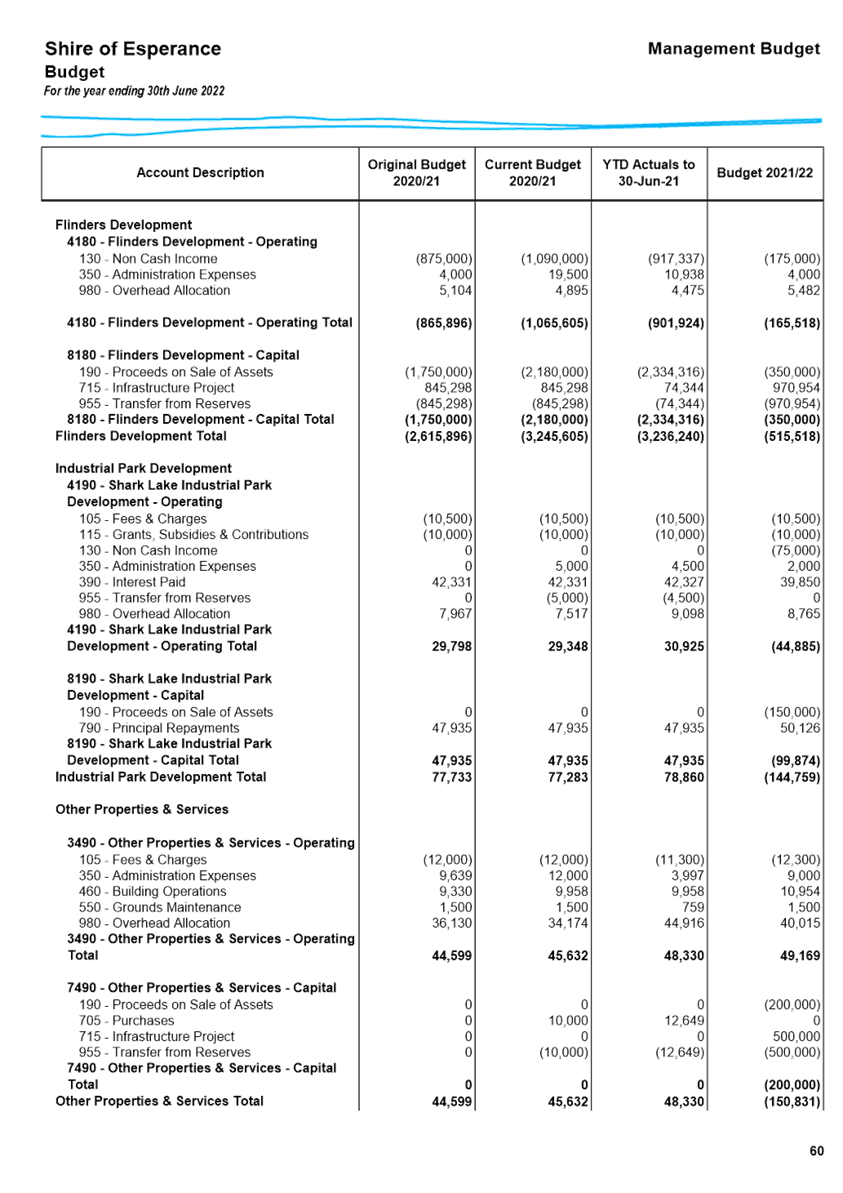

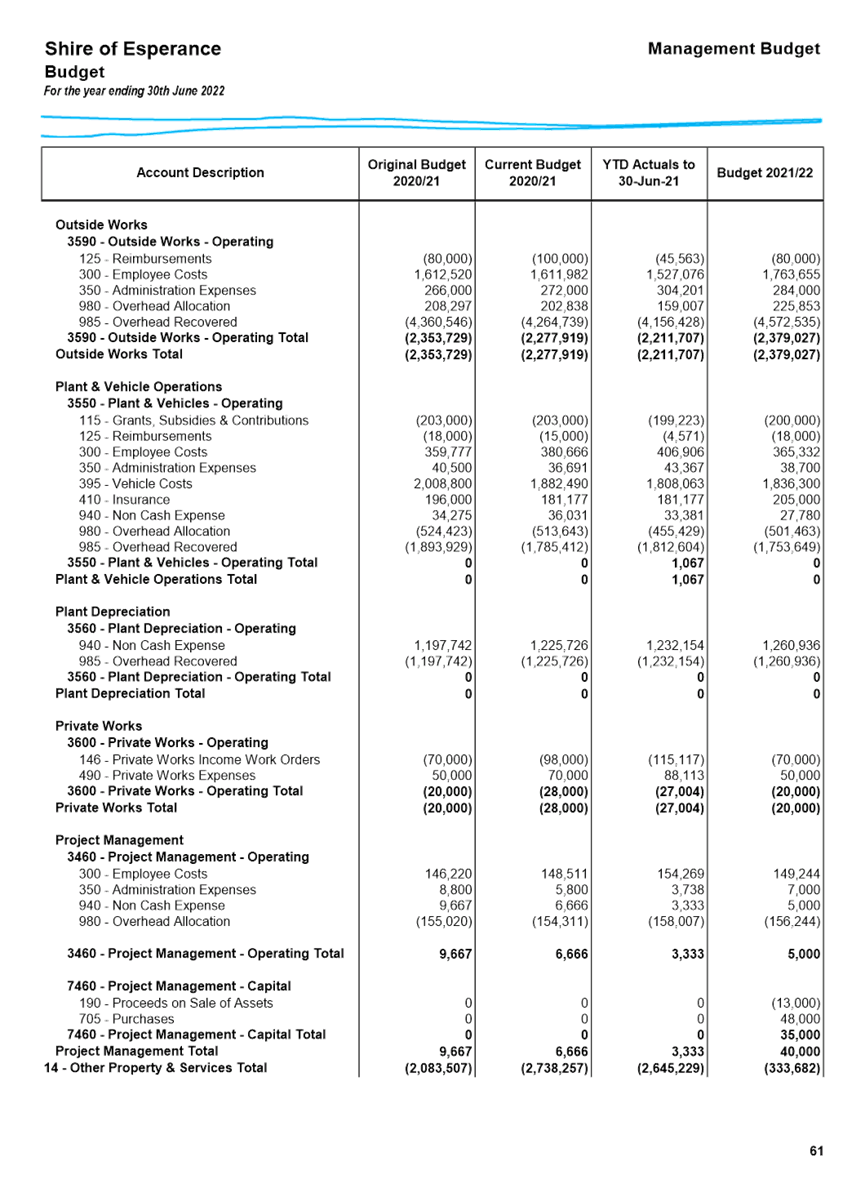

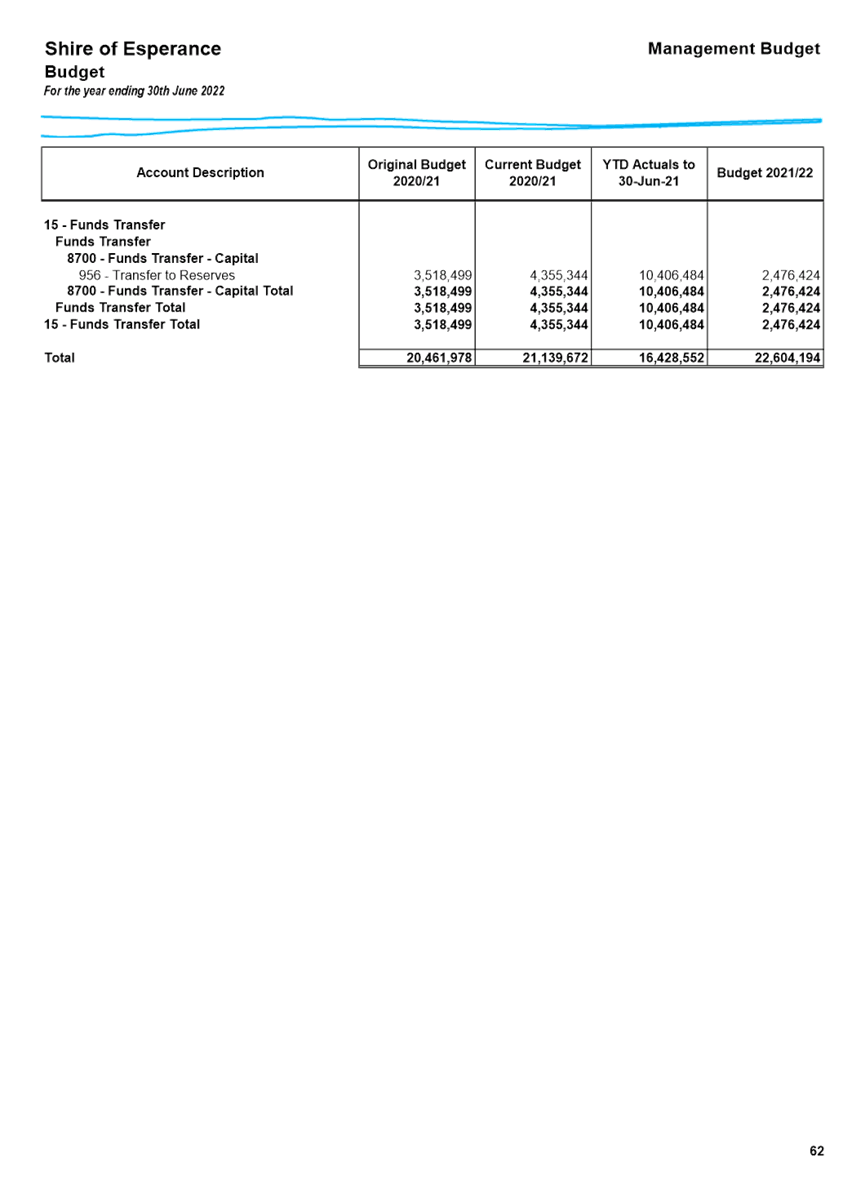

Building Maintenance Reserve. A complete list of the Shire’s reserve

account balances as at 30 June 2021 is provided within the Statutory Budget

document.

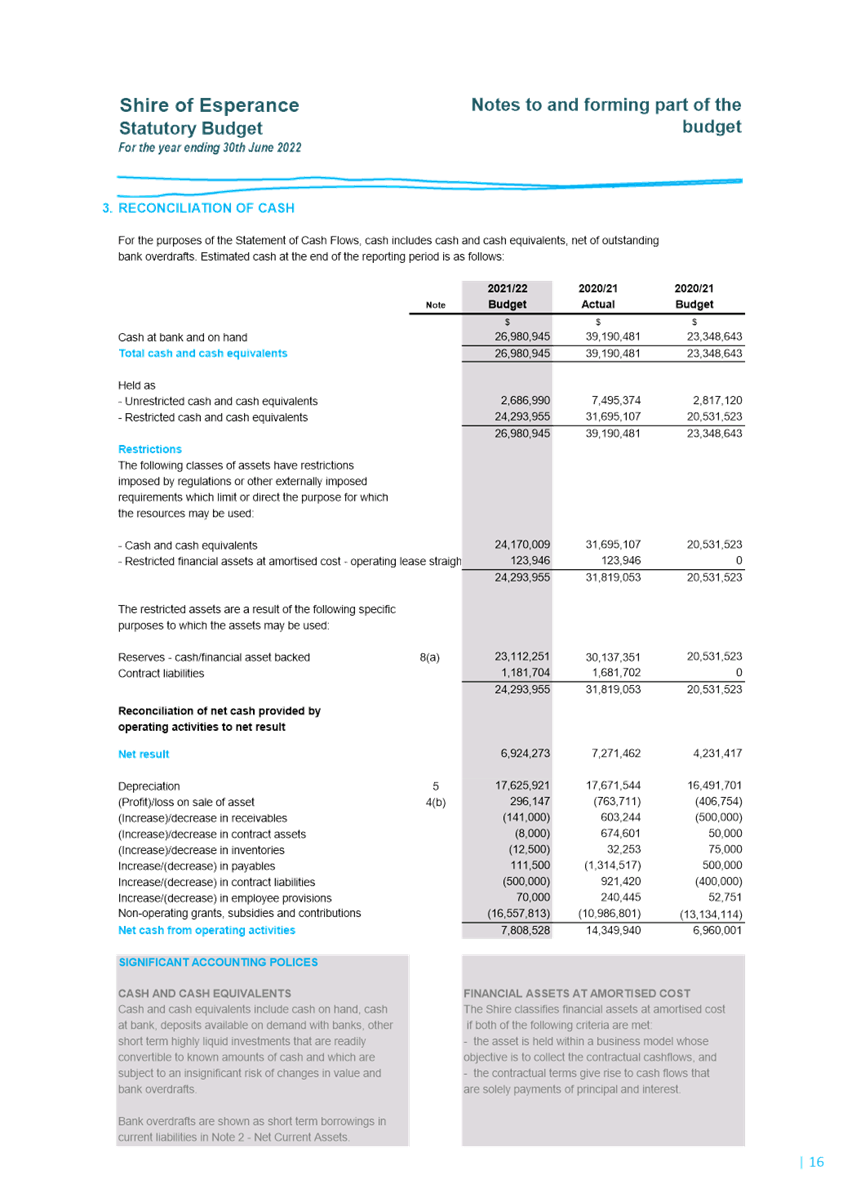

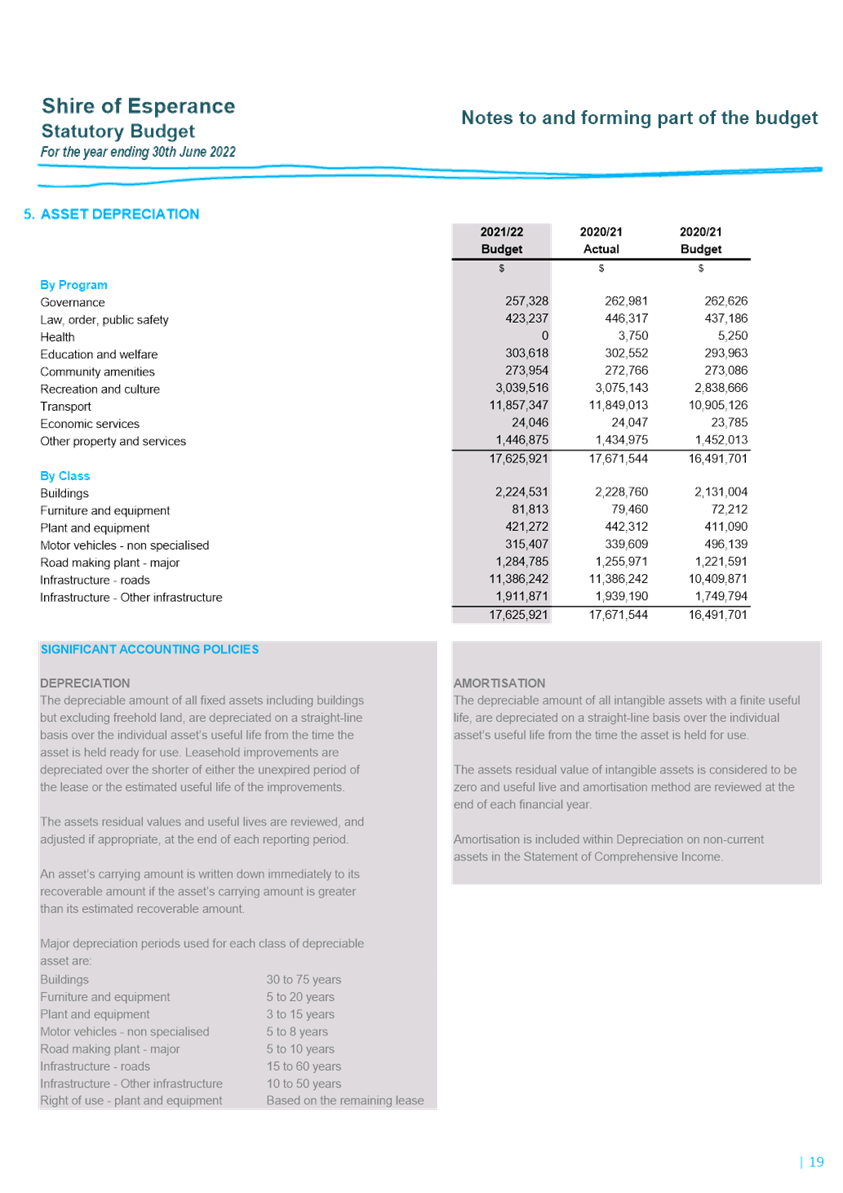

Since the implementation of

“fair value” accounting for assets, depreciation has increased

significantly. The FY 2021/22 year estimate for depreciation is

$17,625,921. Current depreciation rates has placed considerable pressure

on maintaining an operating surplus position, as reflected in the asset based

financial ratios reported in the FY 2019/20 Annual Statements. Measures to

address this as well as addressing the asset management gap will be considered

further in the review of the Long Term Financial Plan, with an aim to

maintaining a balanced financial position.

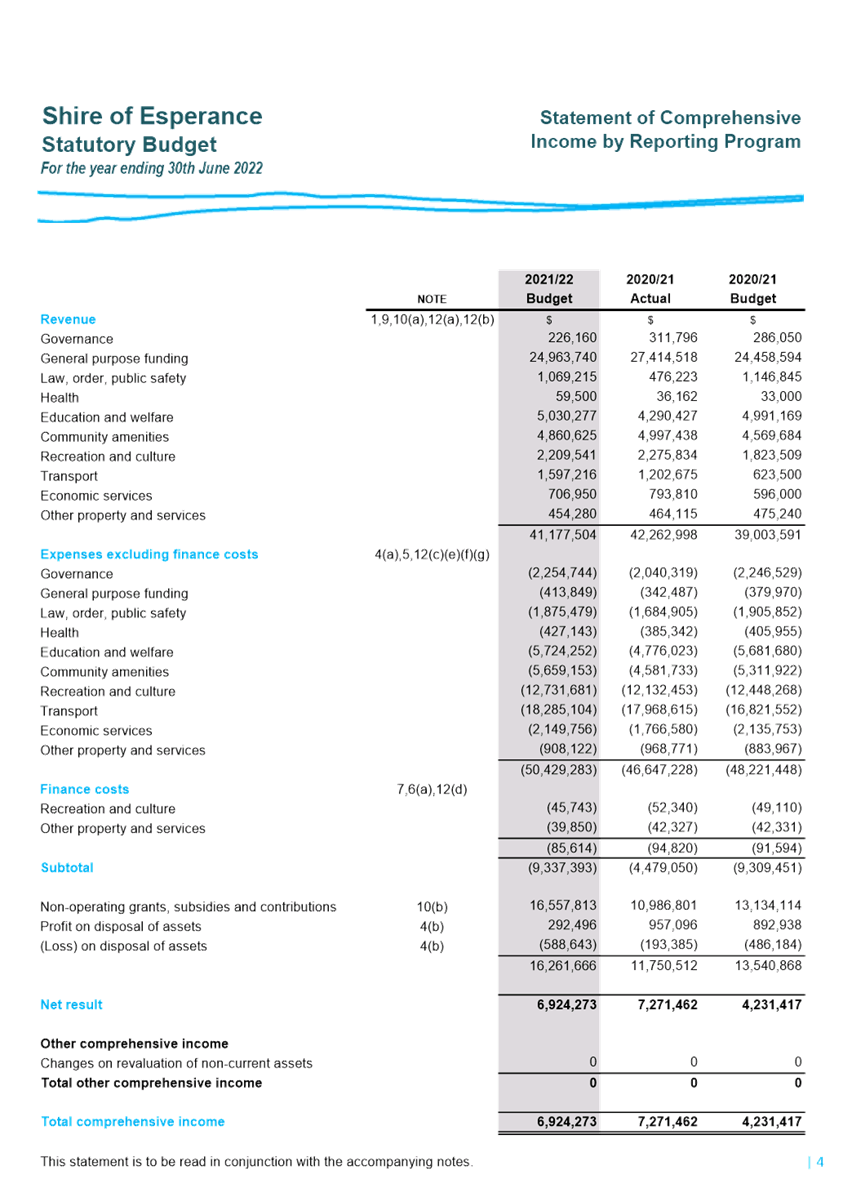

Council will notice that within the

Statement of Comprehensive Income by Nature or Type that an operational loss

(net of capital grant income) is predicted within the 2021/22 year. The

operational loss for the 2021/22 year is amplified due to prepaid Financial

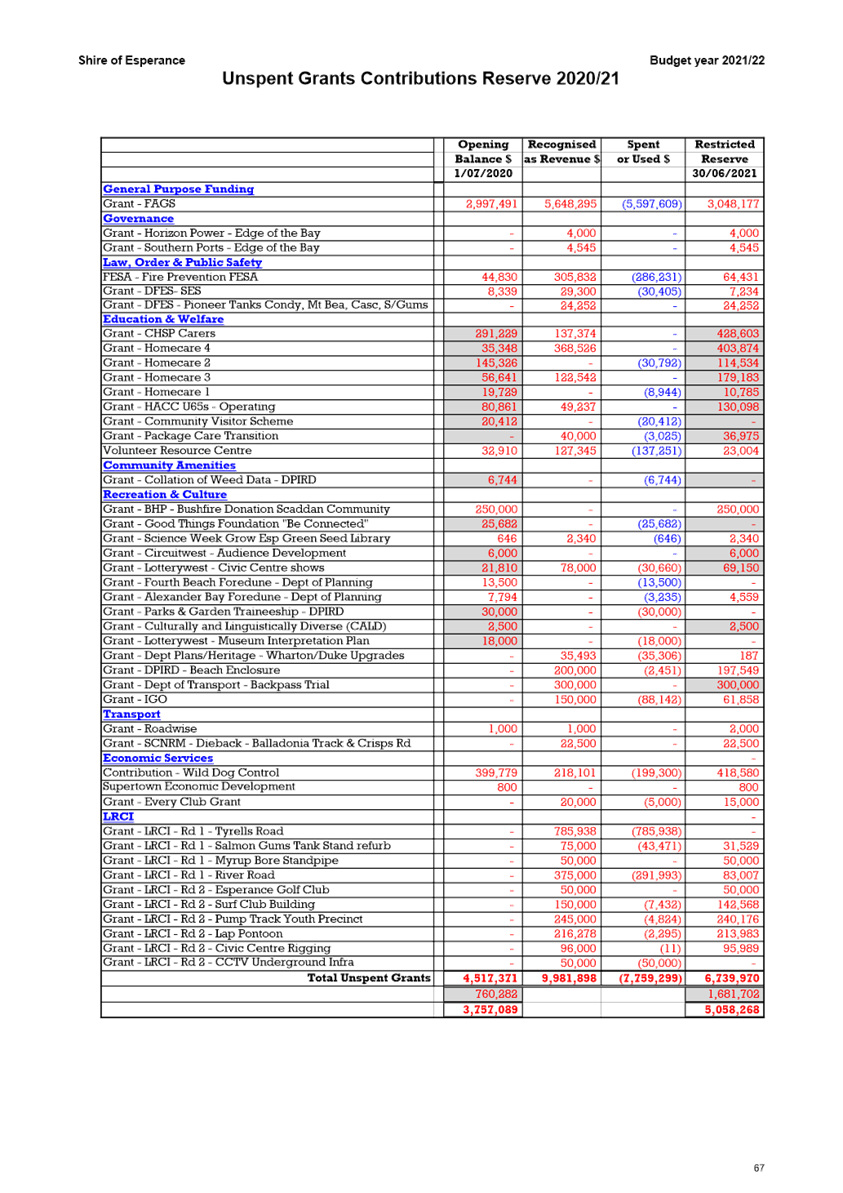

Assistance Grants (FAGS) of $3.048m that was received just prior to the 30th

June 2021. Although this is a good result for the 2020/21 operating position it

means that the FAGS money that is relevant to the 2021/22 year will not be

recognised during the 2021/22 year unless FAGS is again prepaid in June 2022.

The increase in depreciation over the past few years due to the revaluation of

assets from historical cost to fair value has been the main reasoning for the

operational loss. The depreciation cost is now a cost that can be relied upon

to recognise the current cost for the usage of long lived assets. Now that

assets are being depreciated more accurately, operational losses will be an

ongoing issue in the short to medium term that the Shire will continue to

address with an aim to meet sustainability into the

future.

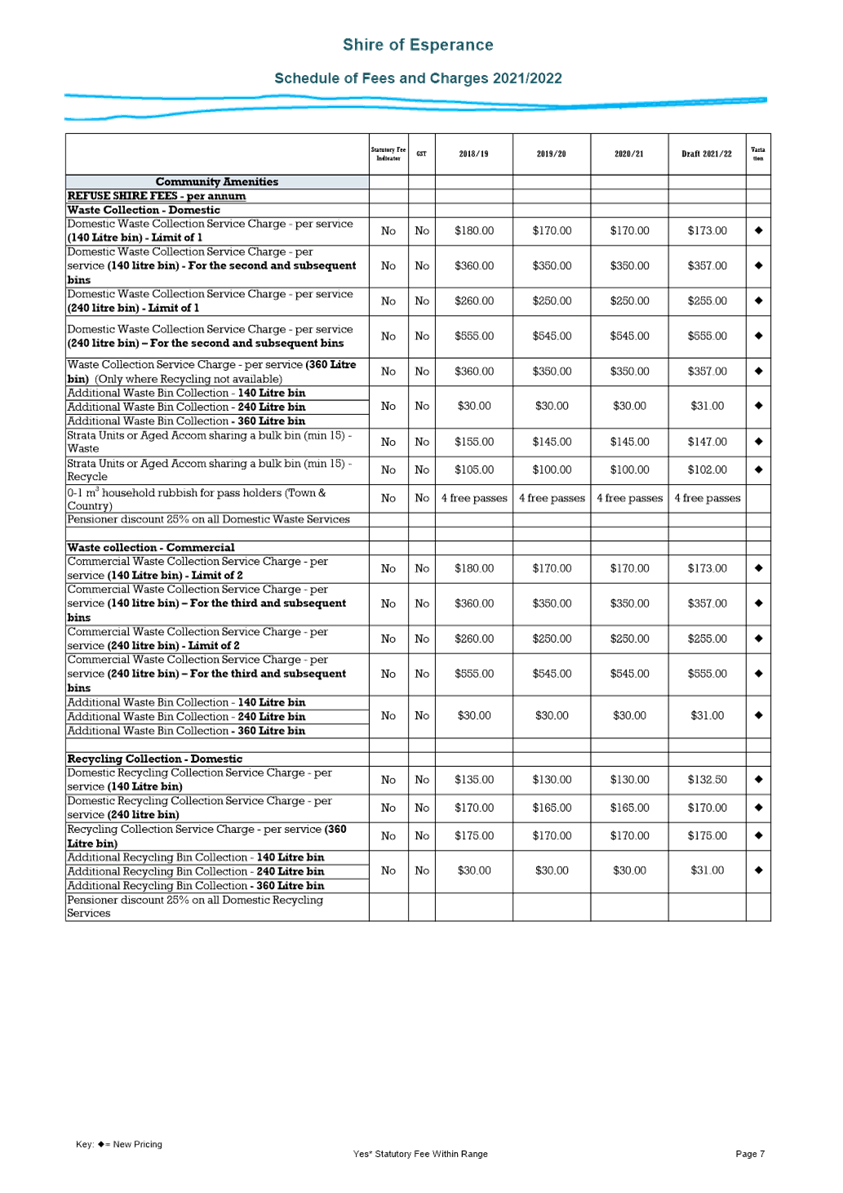

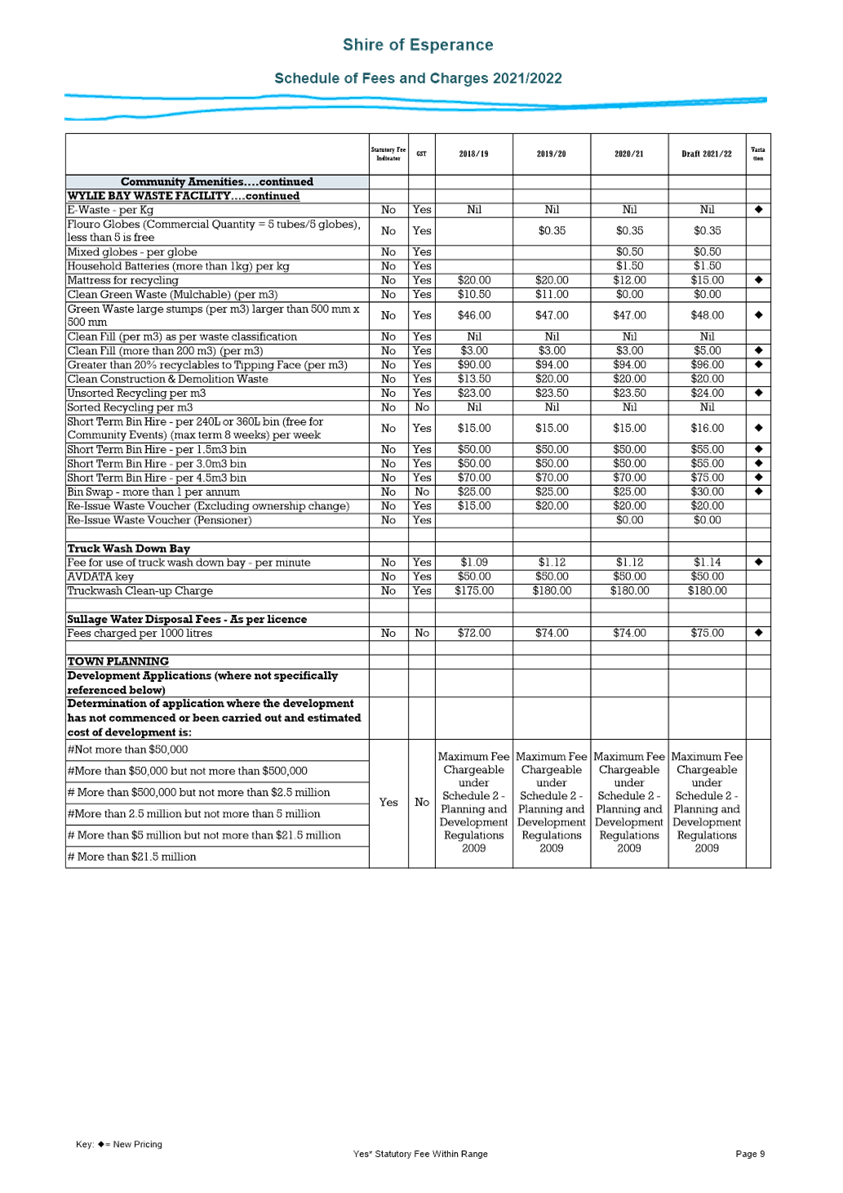

Under the license conditions at the Wylie

Bay Waste Facility there is a limited timeframe to close the existing site at

significant cost and with the development plans necessary to prepare for a new

site and/or alternate waste initiatives, it is proposed to continue the waste

rate at $80 per rateable assessment for 2021/2022. The waste rate will be

charged as a rate in the dollar of 0.000001, covering all rateable properties

within the Shire including rural, mining and un-serviced lots. No property will

pay more than the charge of $80 and this is estimated to raise approx. $608,000

that will assist in the advancement of strategic initiatives for the future of

waste management. A significant amount of money is proposed to be spent in the

near future with further capping of sections of the existing Wylie Bay Site as

well as the development of the community drop off and transfer station at

Myrup.

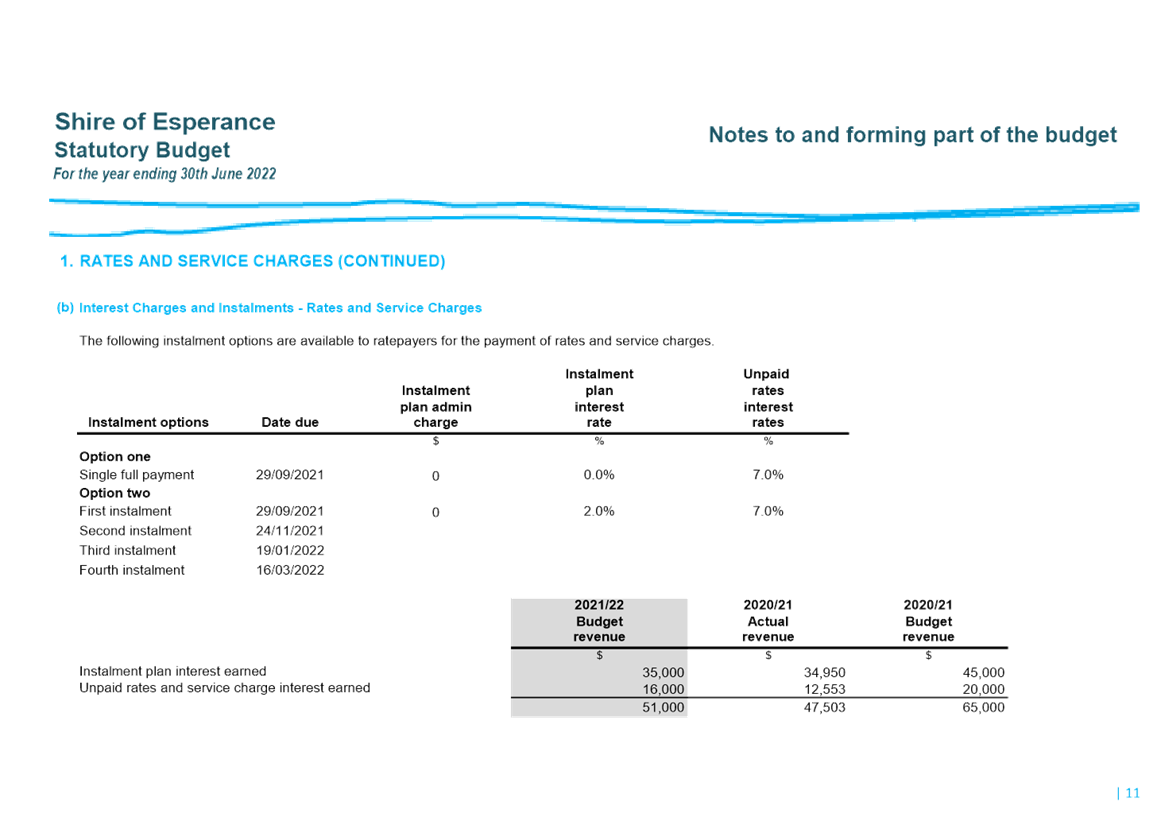

It is proposed to continue with a lower

penalty interest on unpaid rates. In line with the penalty rate set for

outstanding ESL rates, a penalty interest rate of 7% is proposed and instalment

interest maintained at 2%. These are also well within the new revised

regulations from the State Government requiring penalty interest to not exceed

8% and instalment interest not exceeding 5.5%.

The Statutory Budget as presented has

been prepared with the parameters that were set at the Draft Budget workshops

that were held in June. A number of the figures that were presented at the

Draft Budget Workshops have been changed to reflect the known carryovers and

unspent grants being recognised within the 2021/22 budget. The budget presented

is balanced.

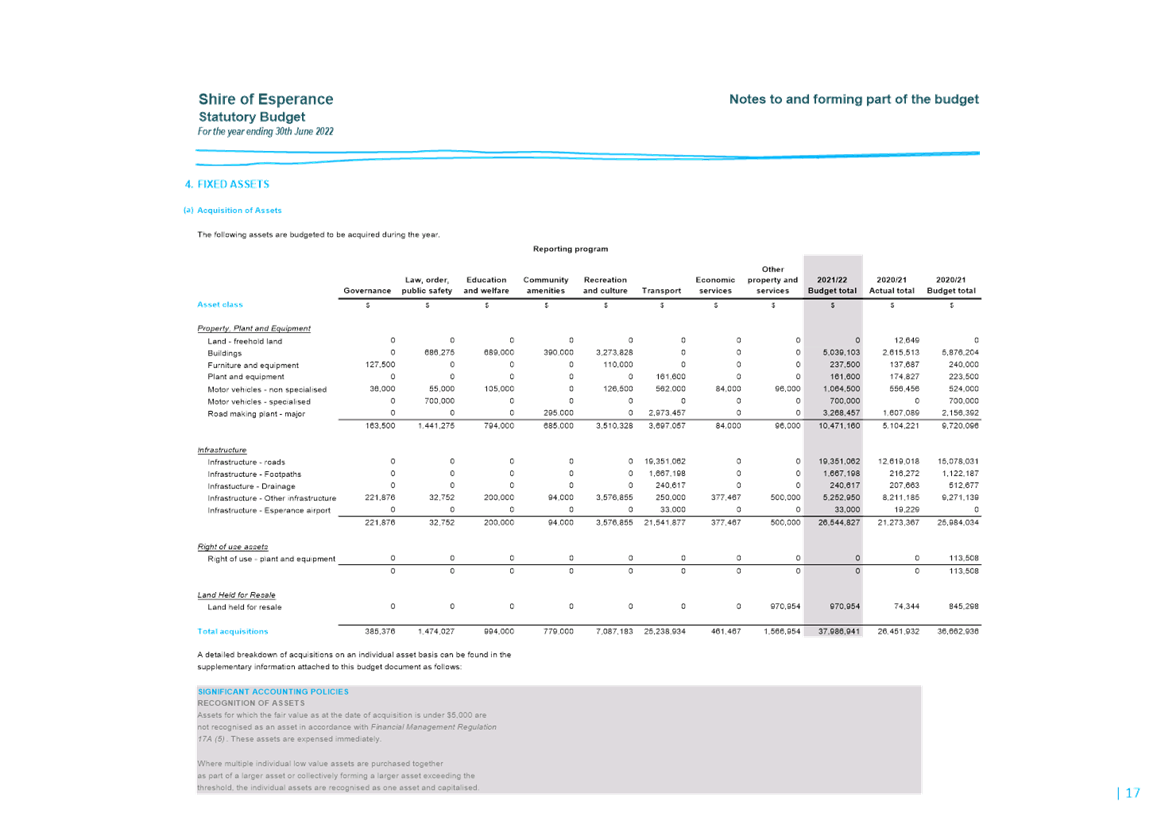

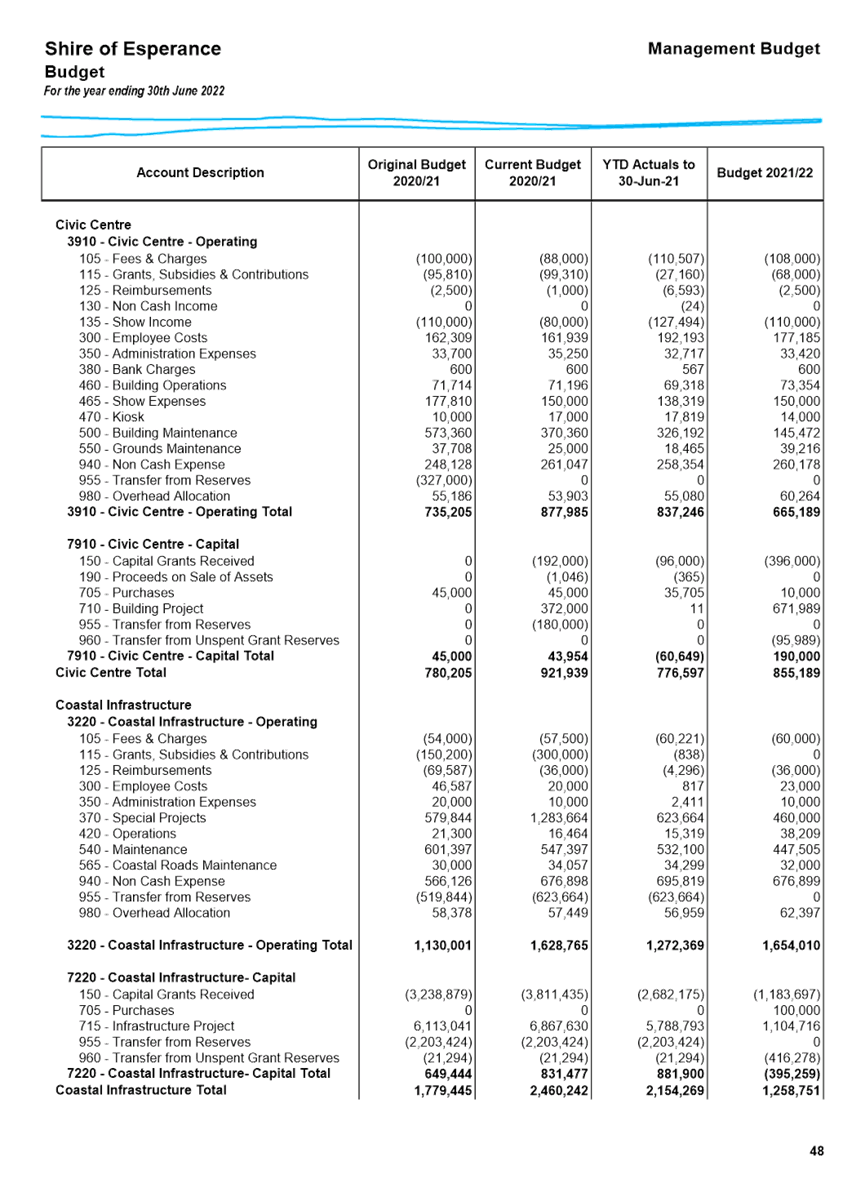

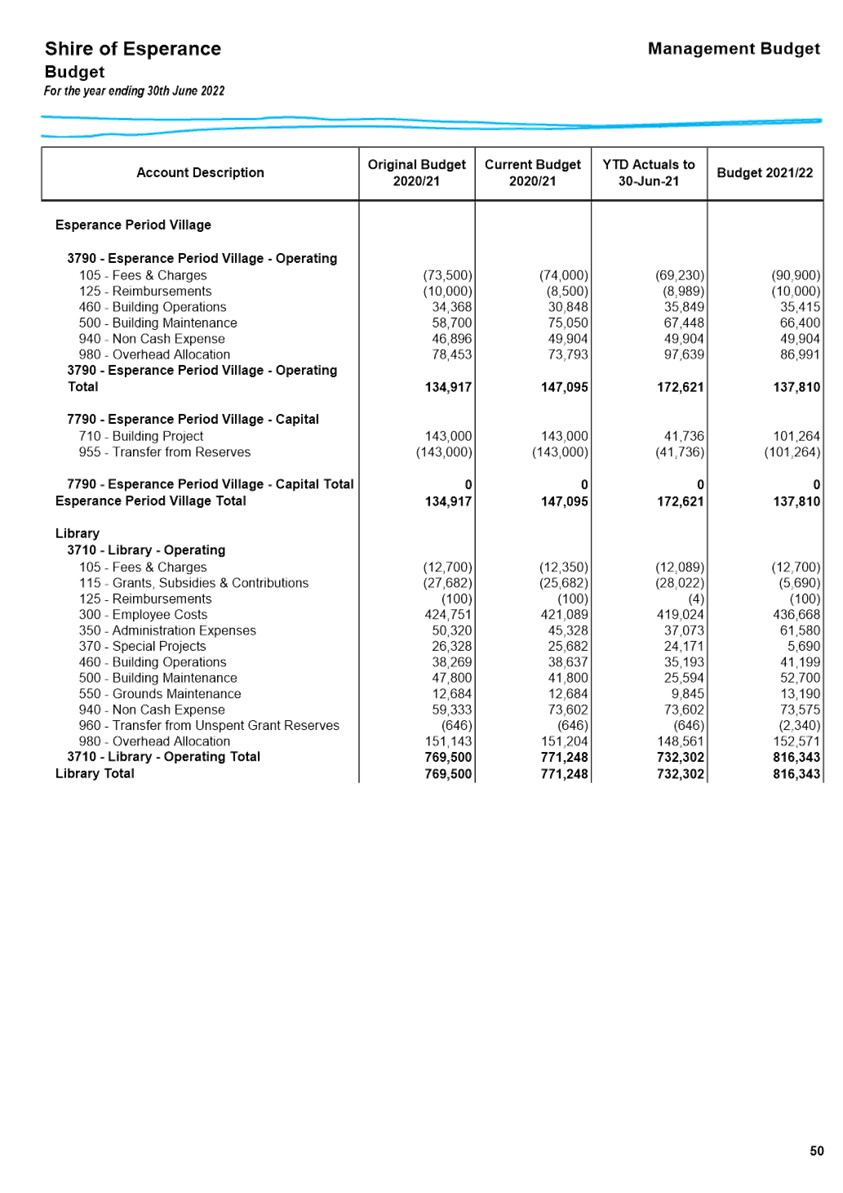

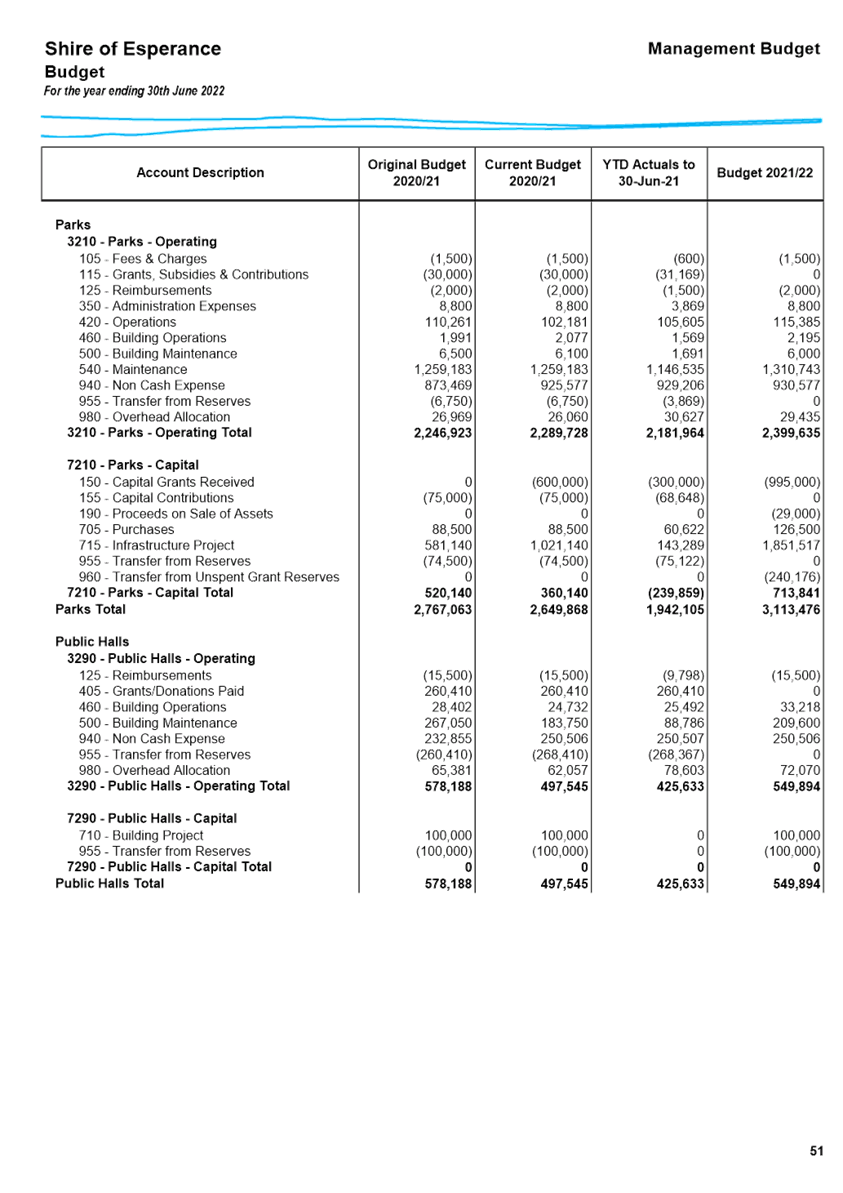

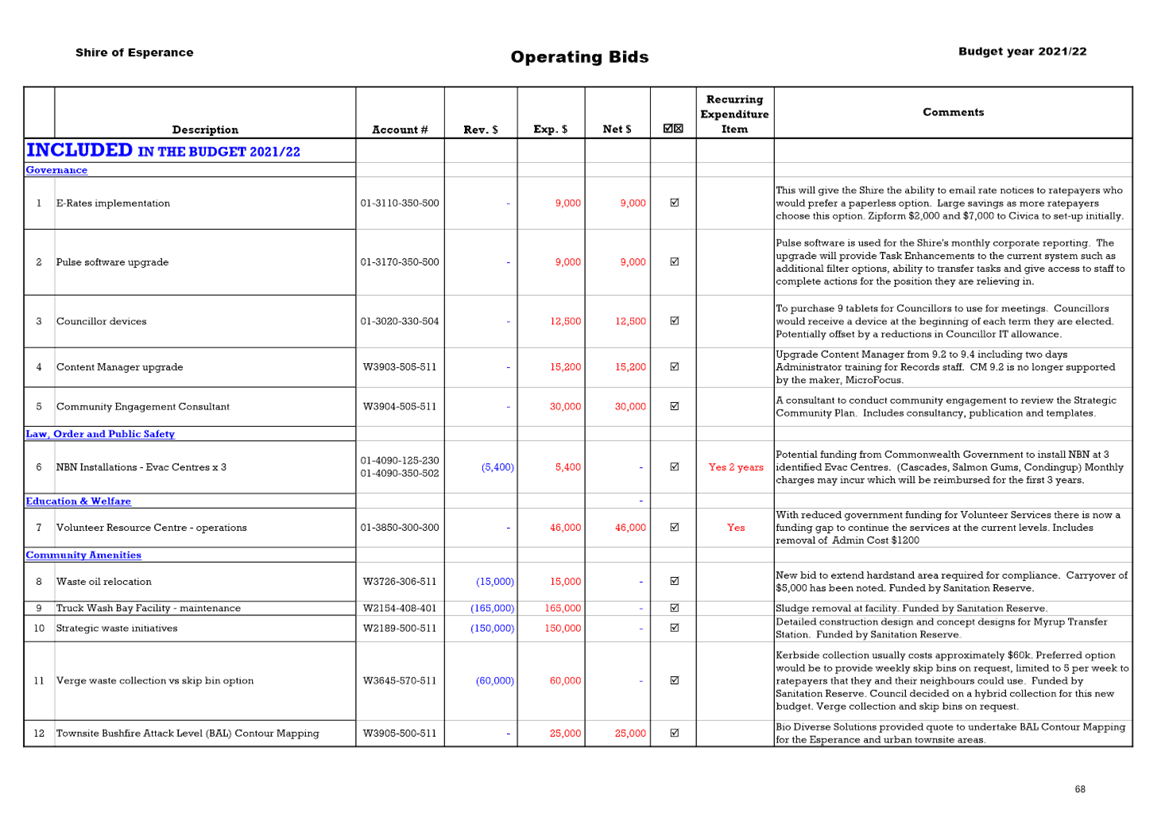

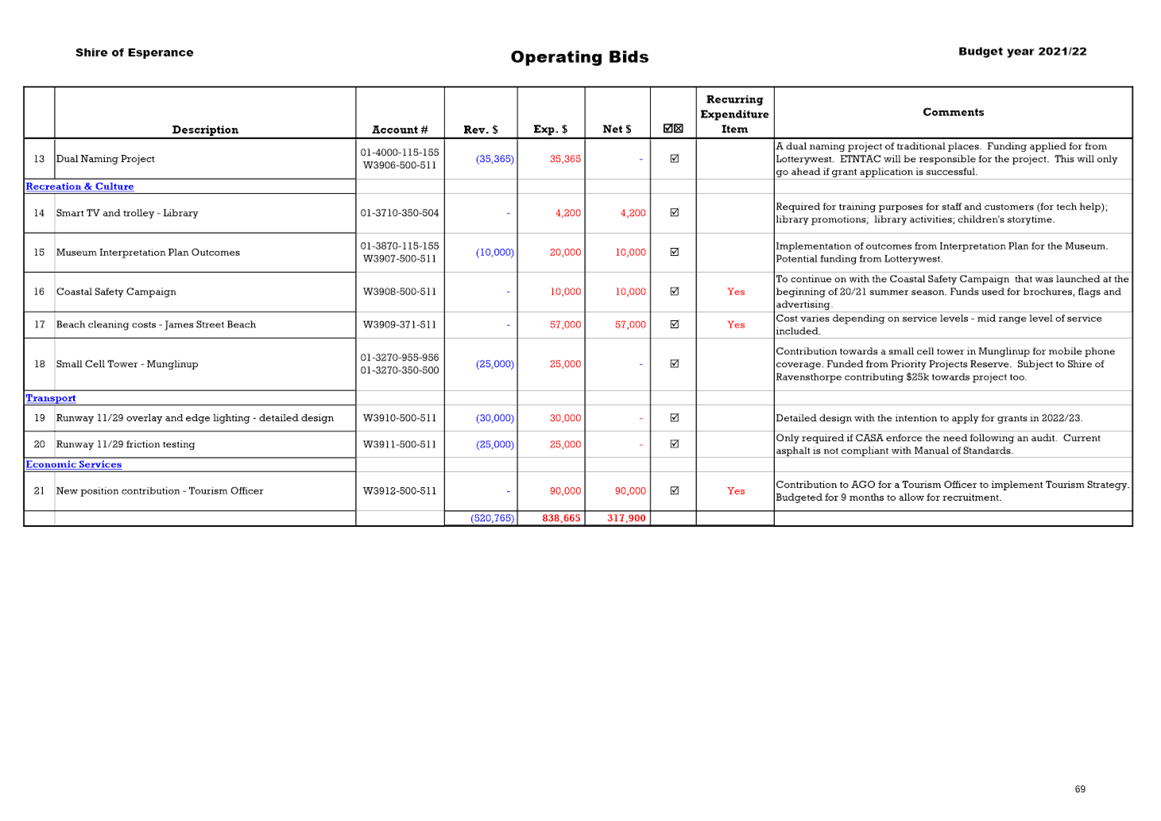

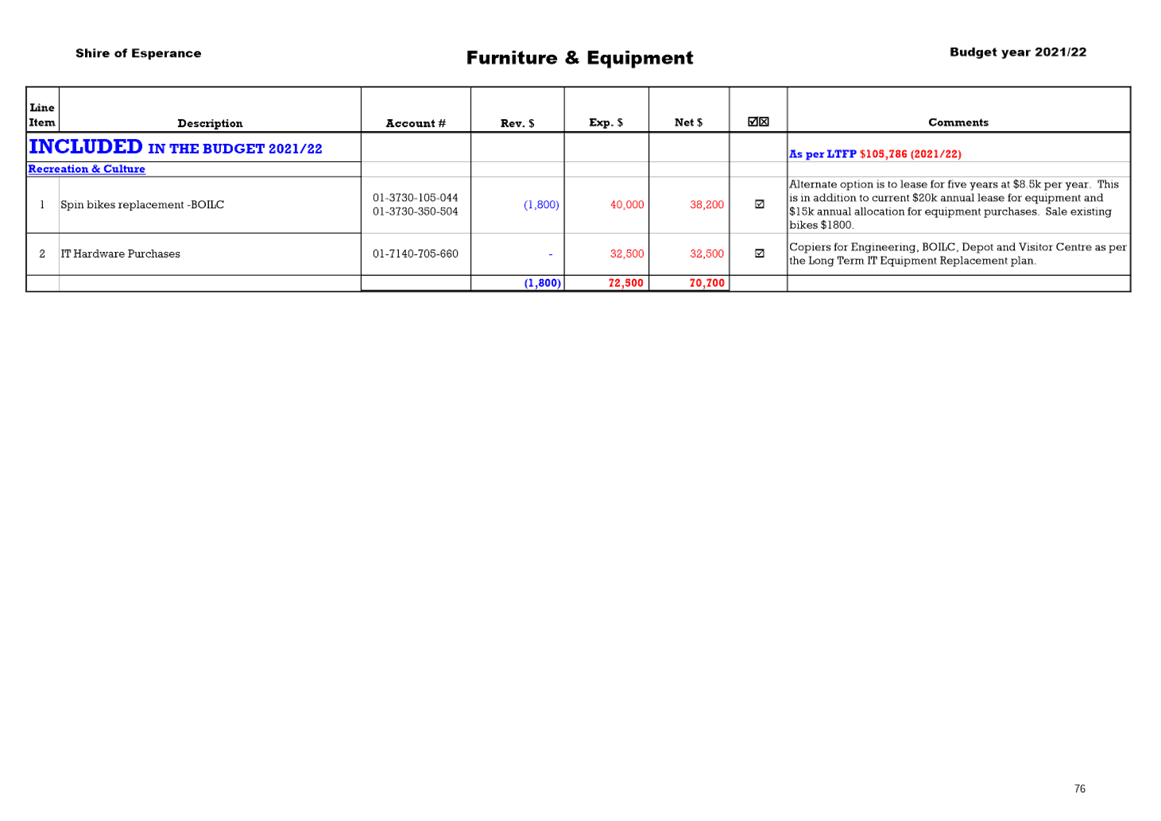

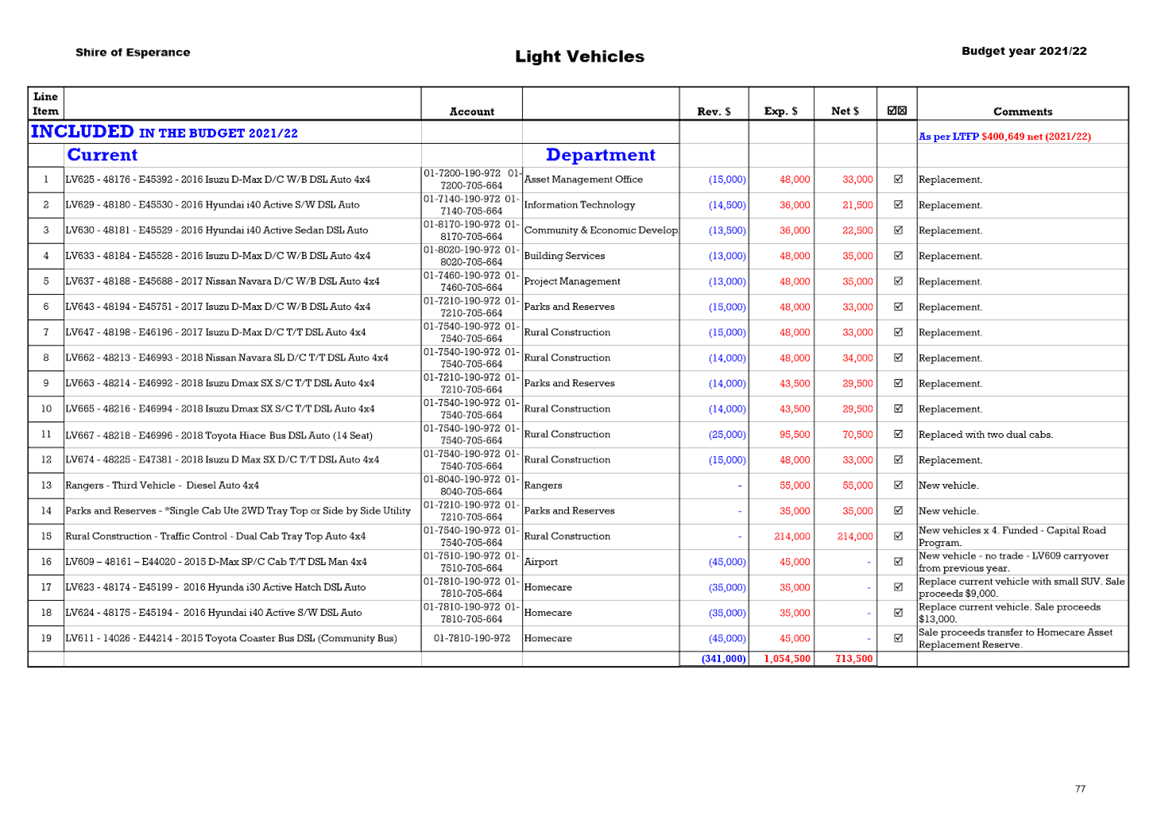

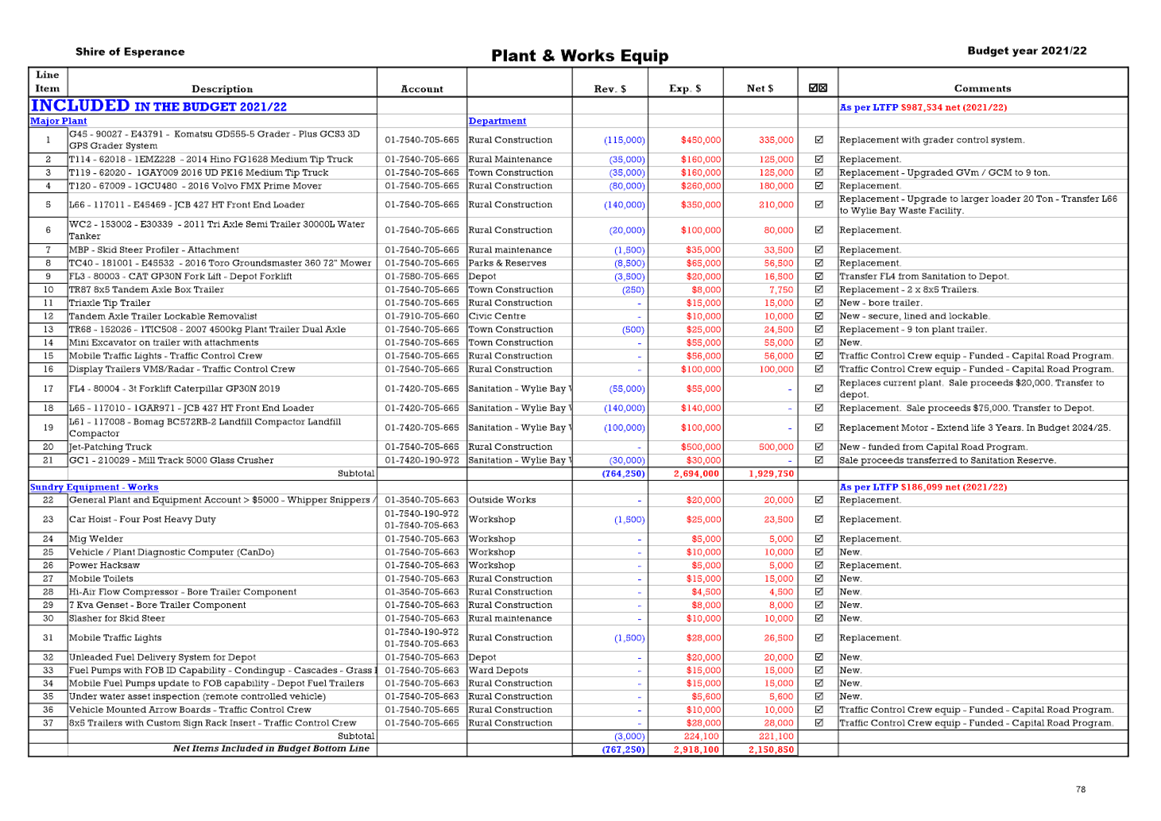

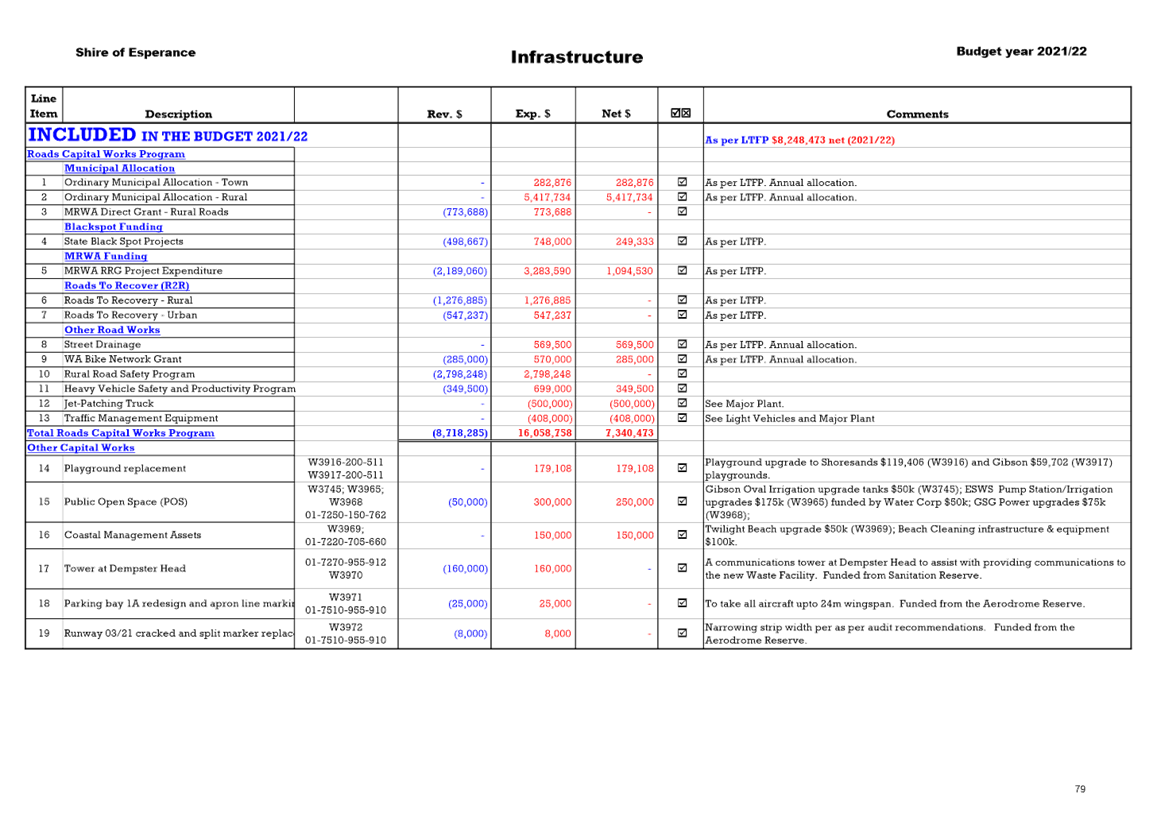

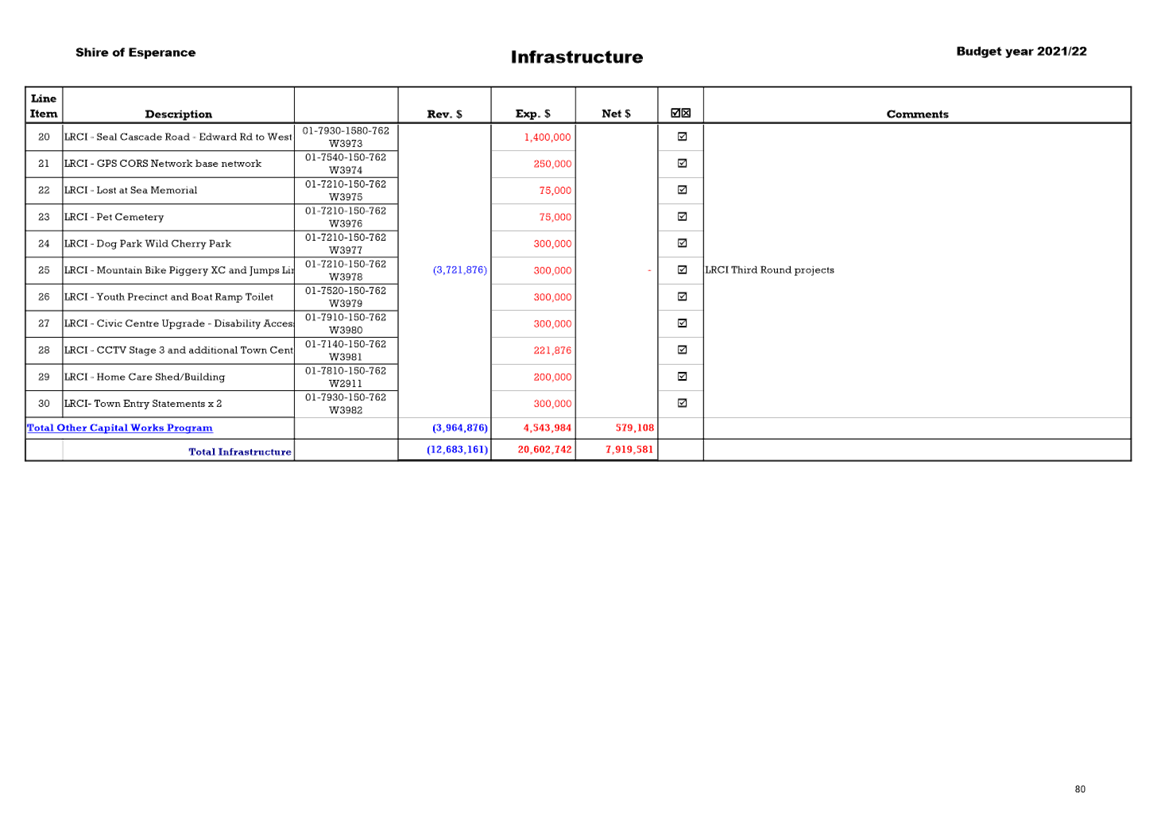

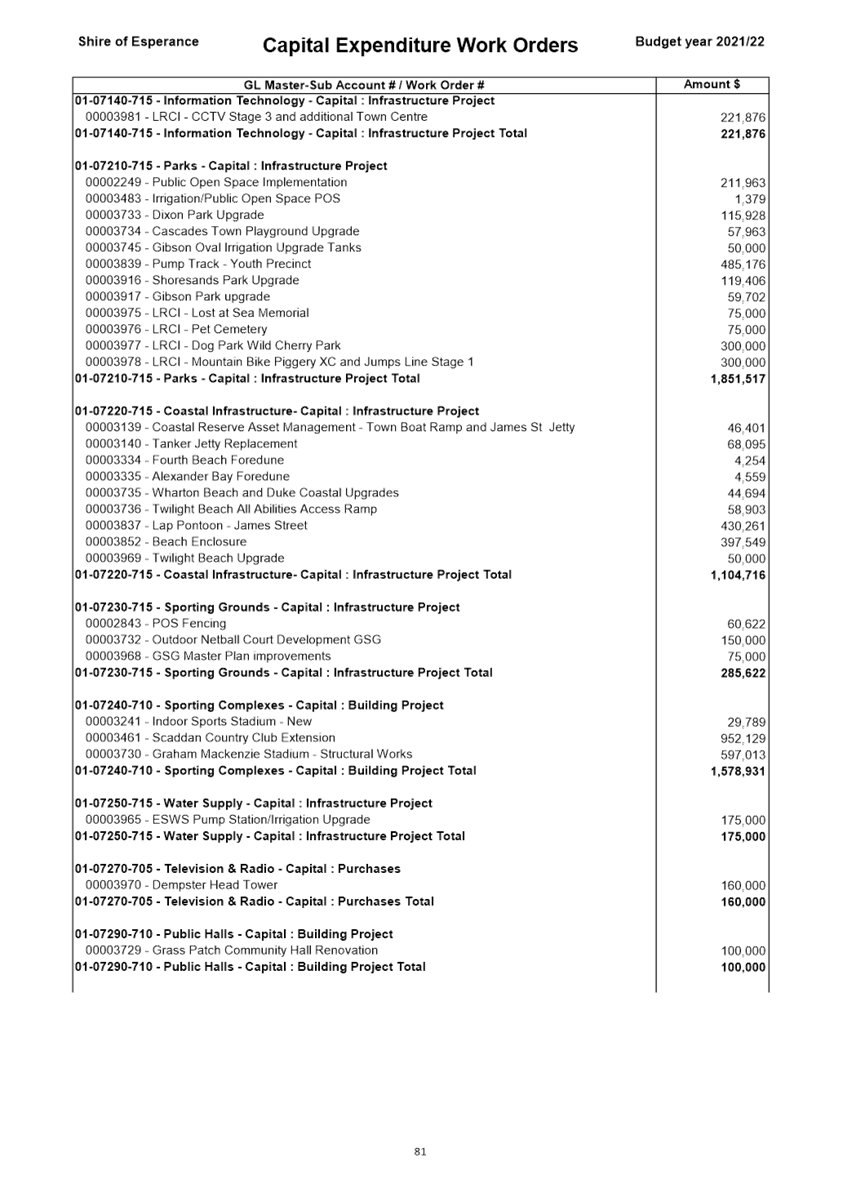

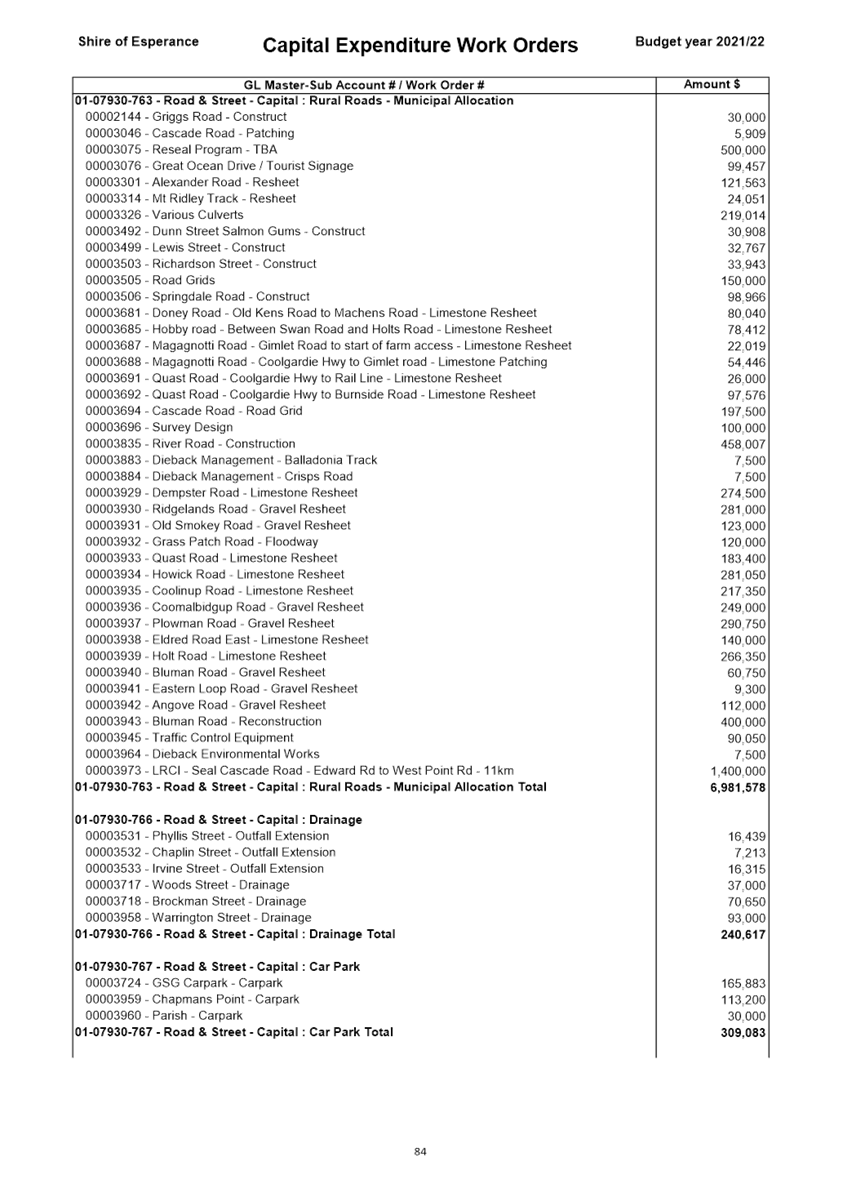

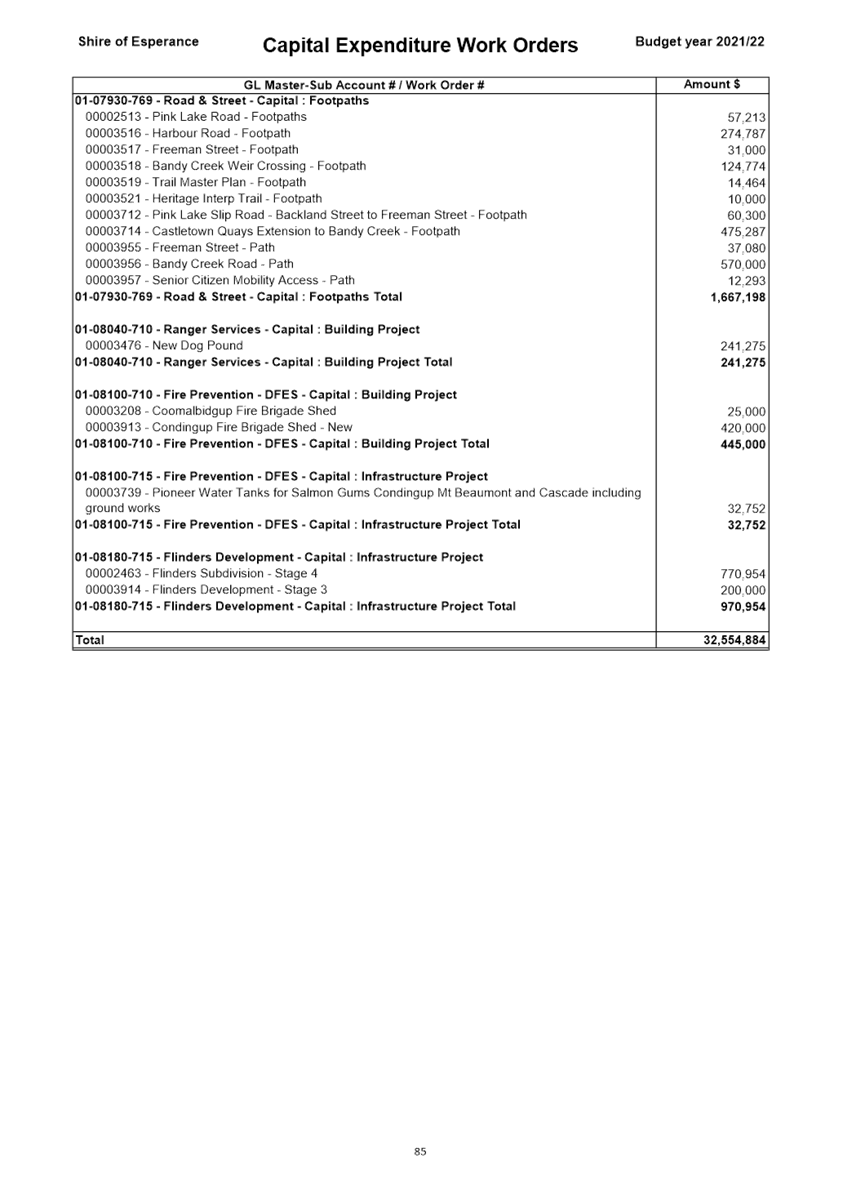

Some of the key capital projects

included within the budget include the following-

· Communications Tower Dempster Head $160,000

· Playground Replacement – Shoresands $119,406

· Irrigation upgrades – various locations $250,000

· Playground Replacement – Gibson $59,702

· GPS CORS Network base network $250,000

· Lost at Sea Memorial $75,000

· Pet Cemetery $75,000

· Dog Park Wild Cherry Park $300,000

· Mountain Bike Piggery XC and Jumps Line Stage 1 $300,000

· Youth Precinct and Boat Ramp Toilet

$300,000

· Civic Centre Upgrade - Disability Access and Toilets $300,000

· CCTV Stage 3 and additional Town Centre $221,876

· Home Care Shed/Building $200,000

· Town Entry Statements x 2 $300,000

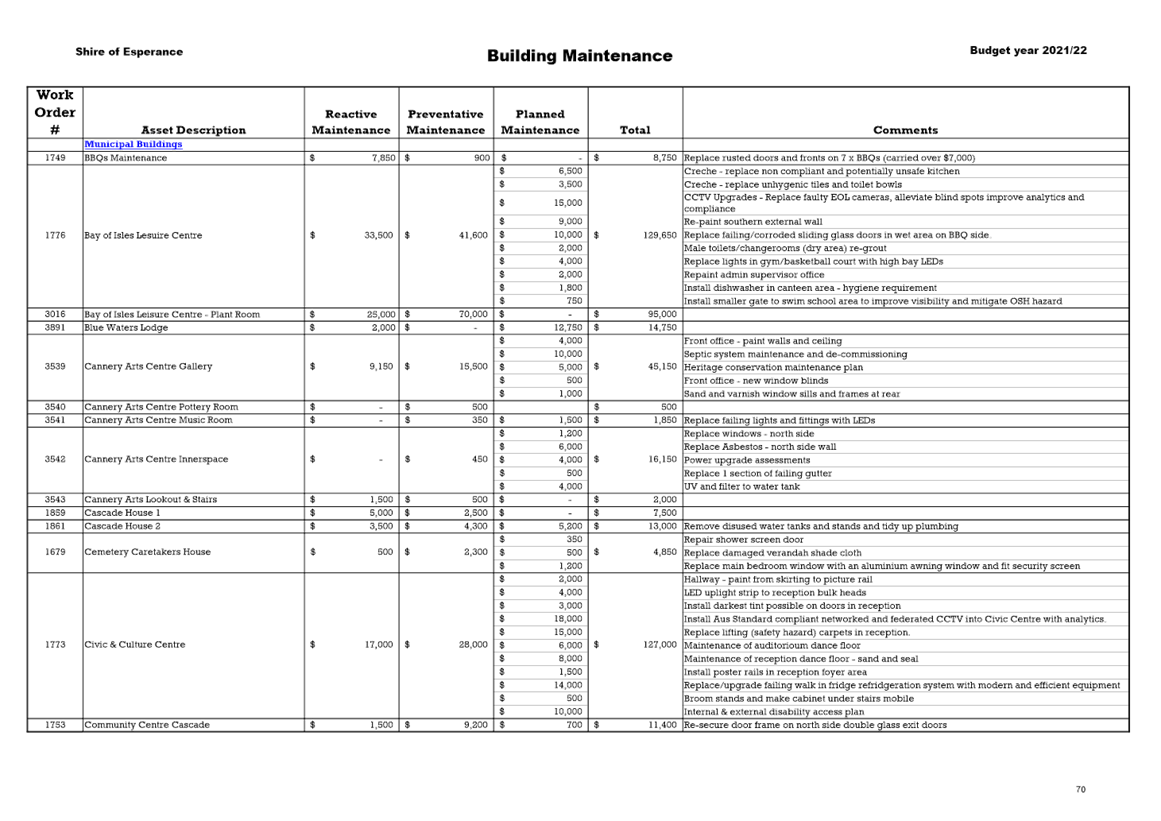

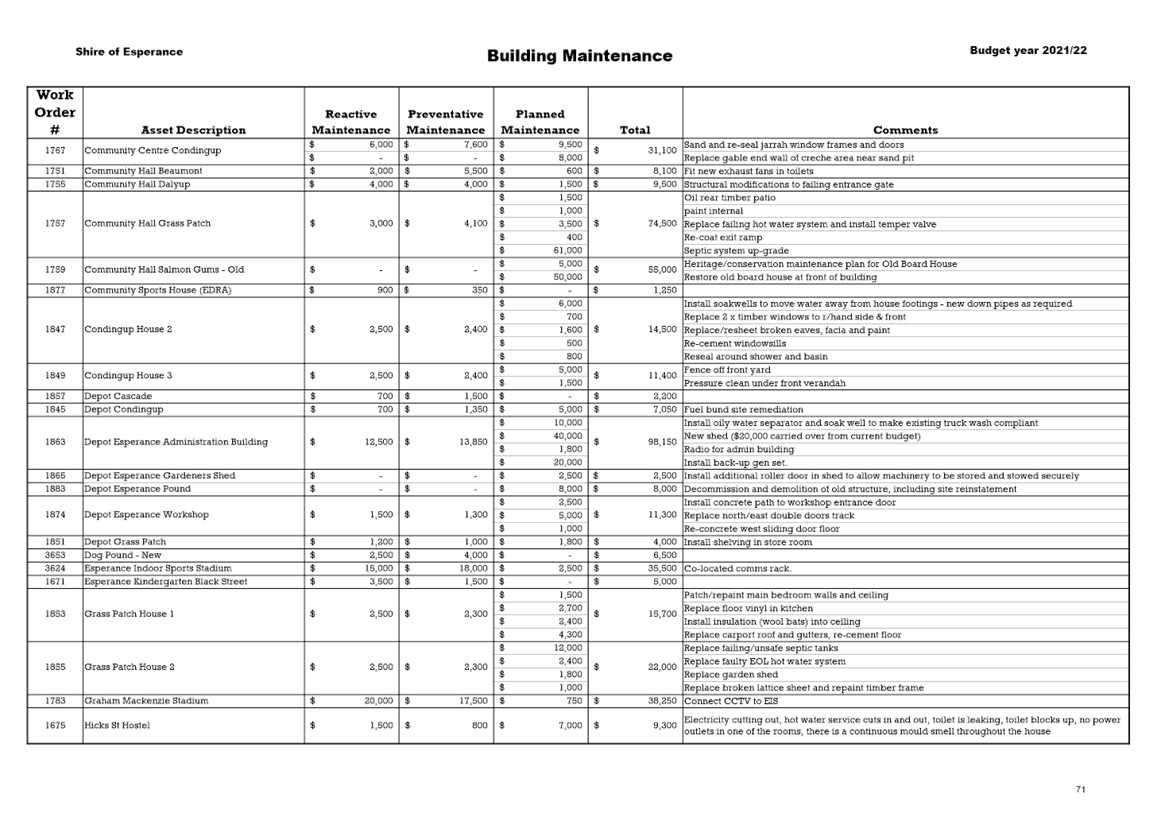

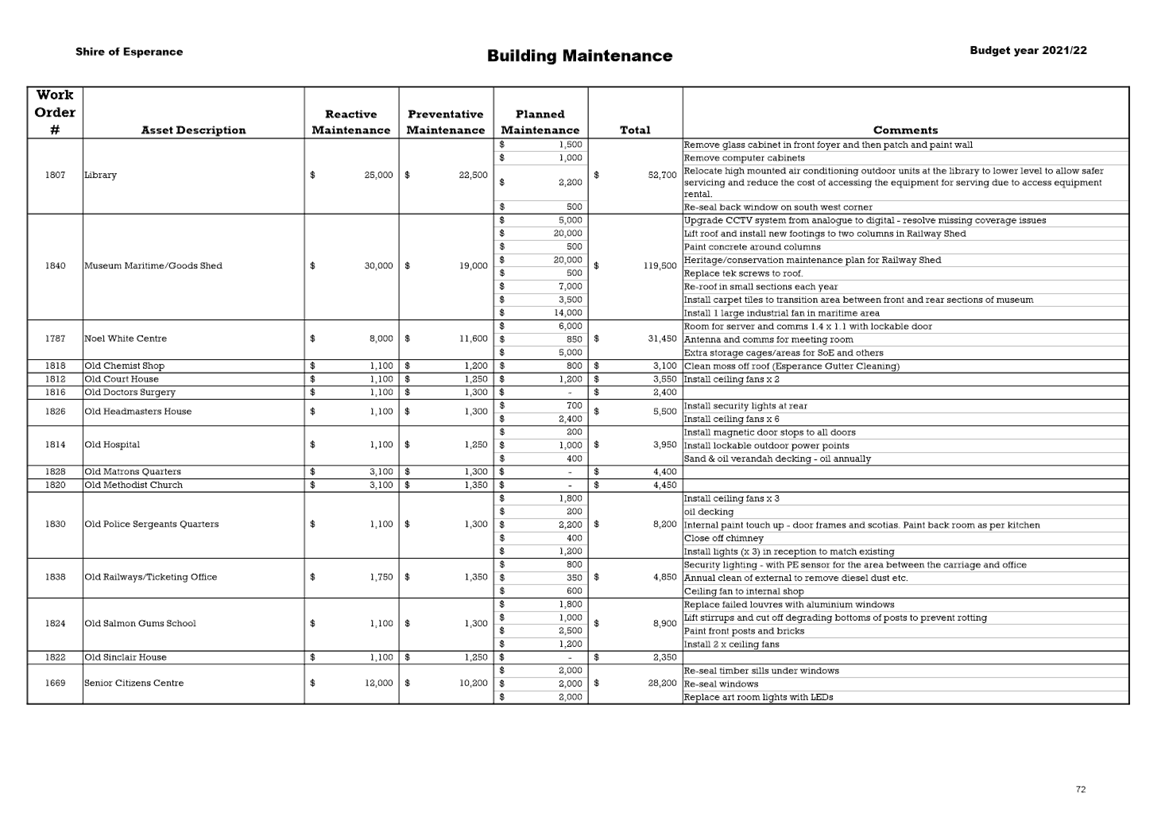

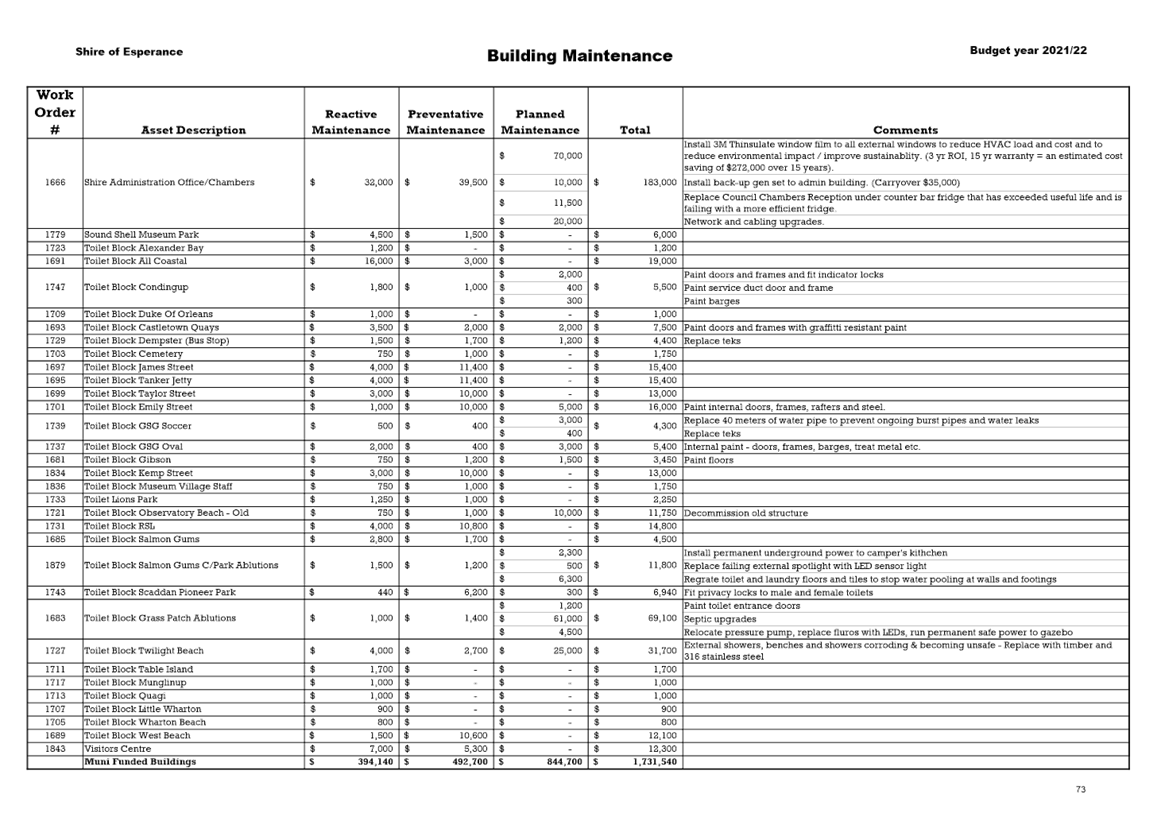

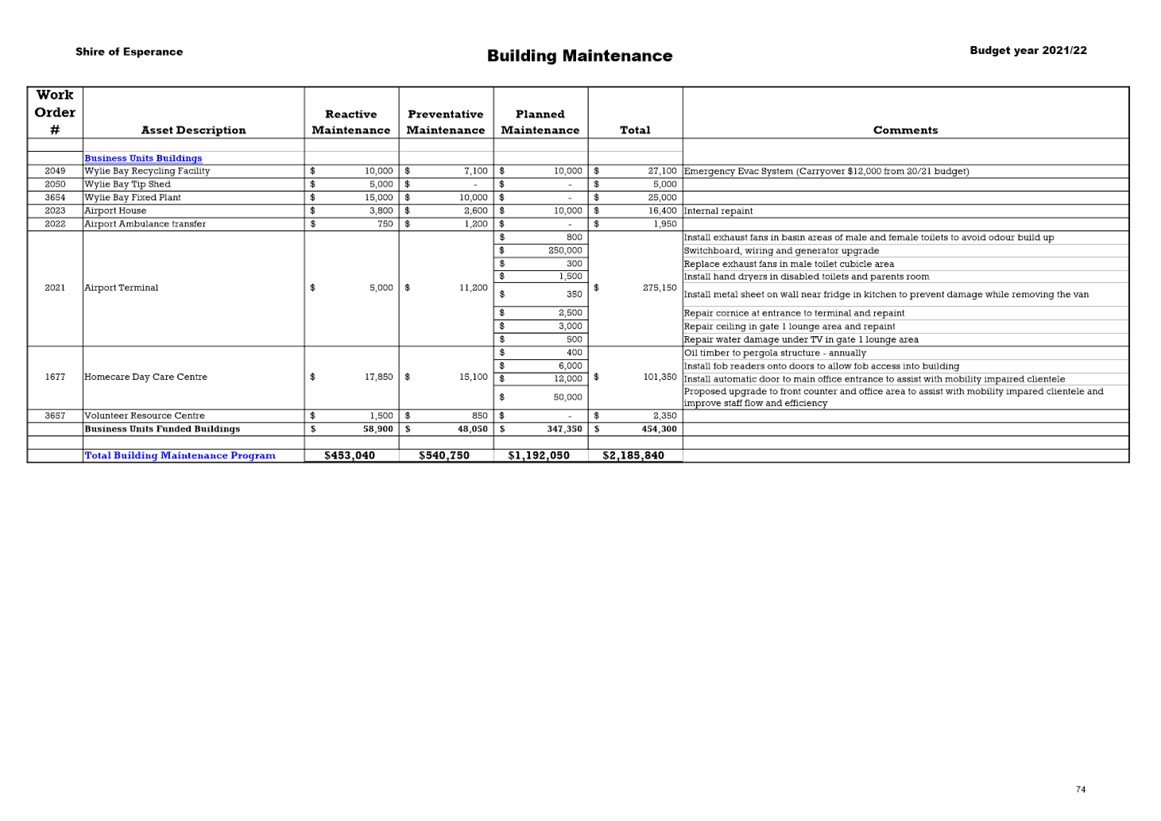

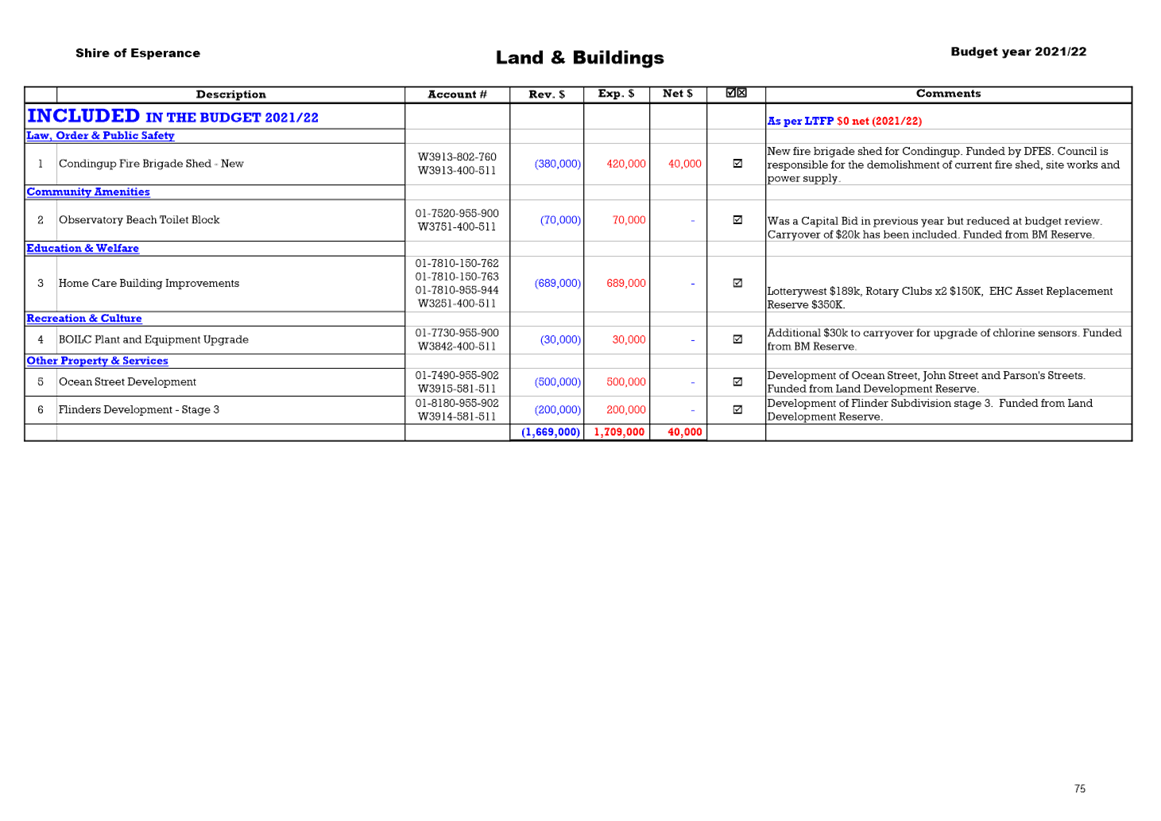

· Building Maintenance Program $1,192,050

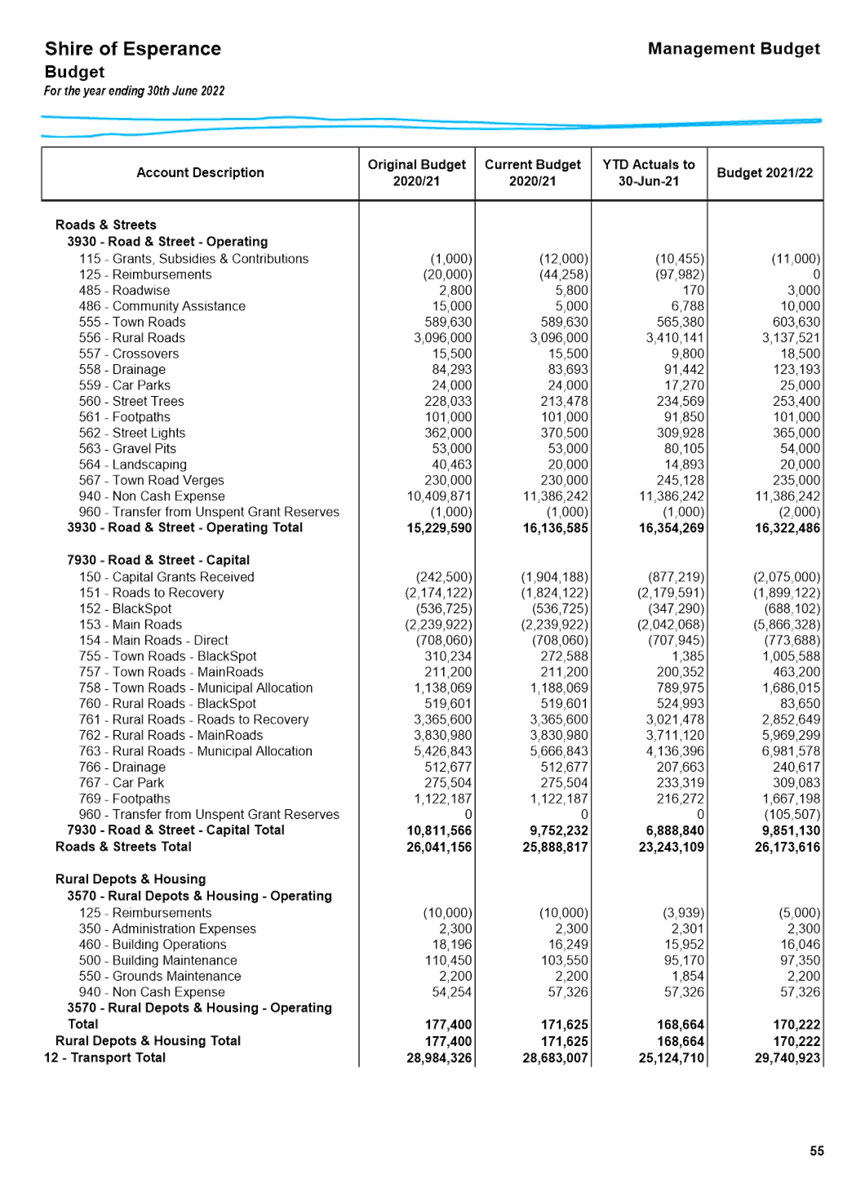

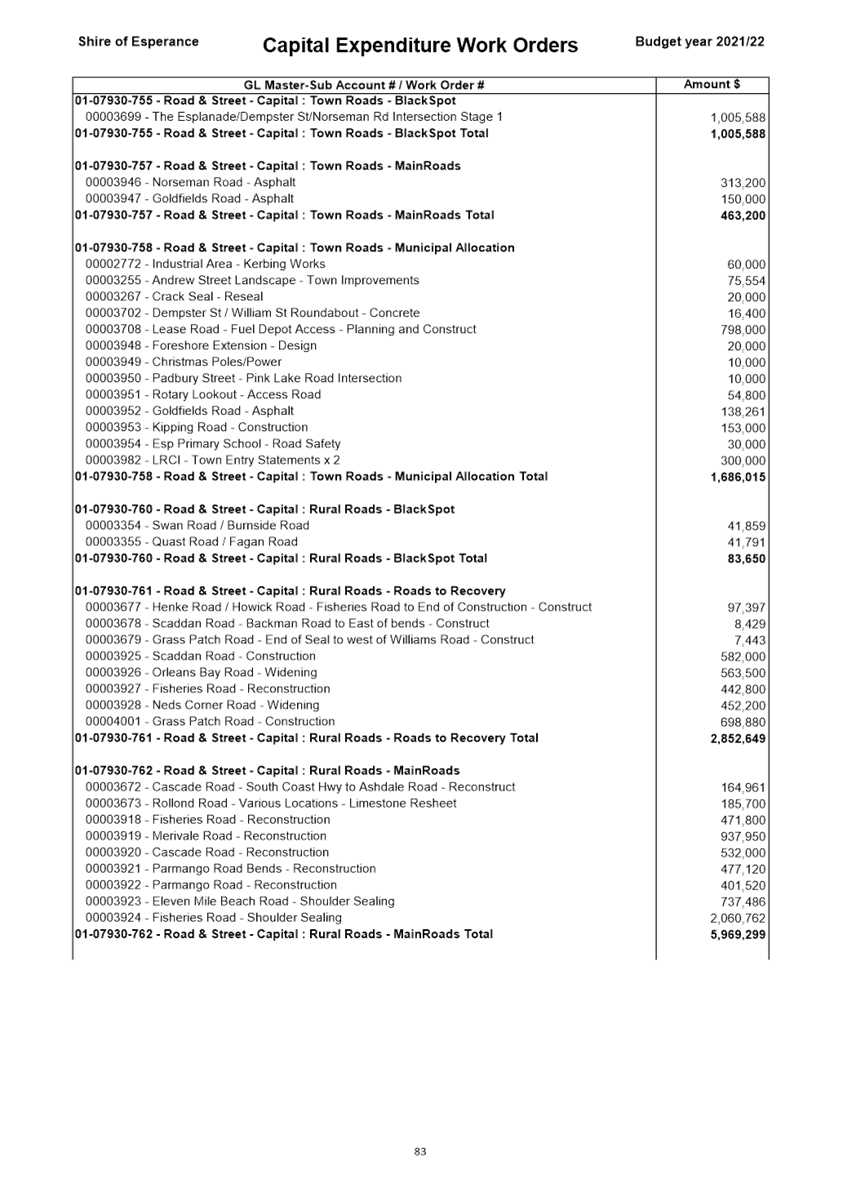

· Road Upgrades and Improvements $17,458,758

(inc LRCI Cascade Rd $1.4m)

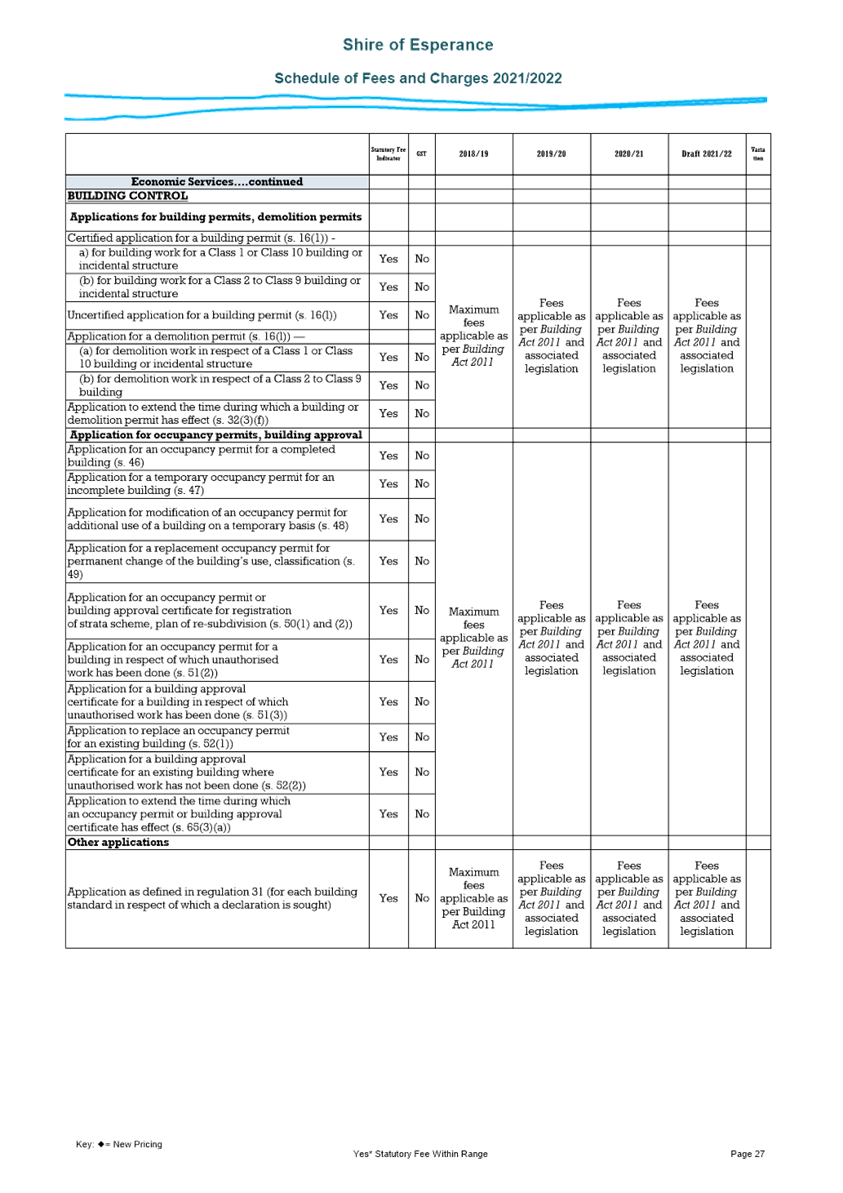

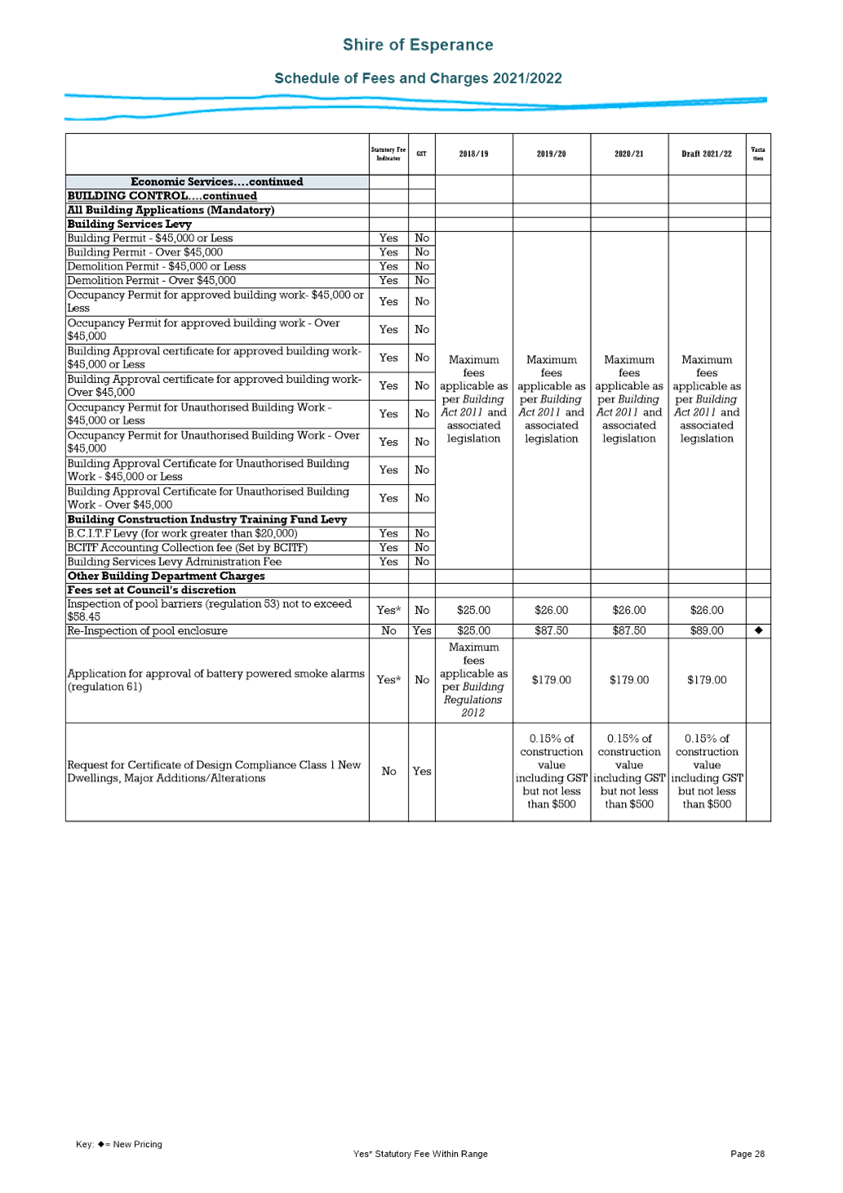

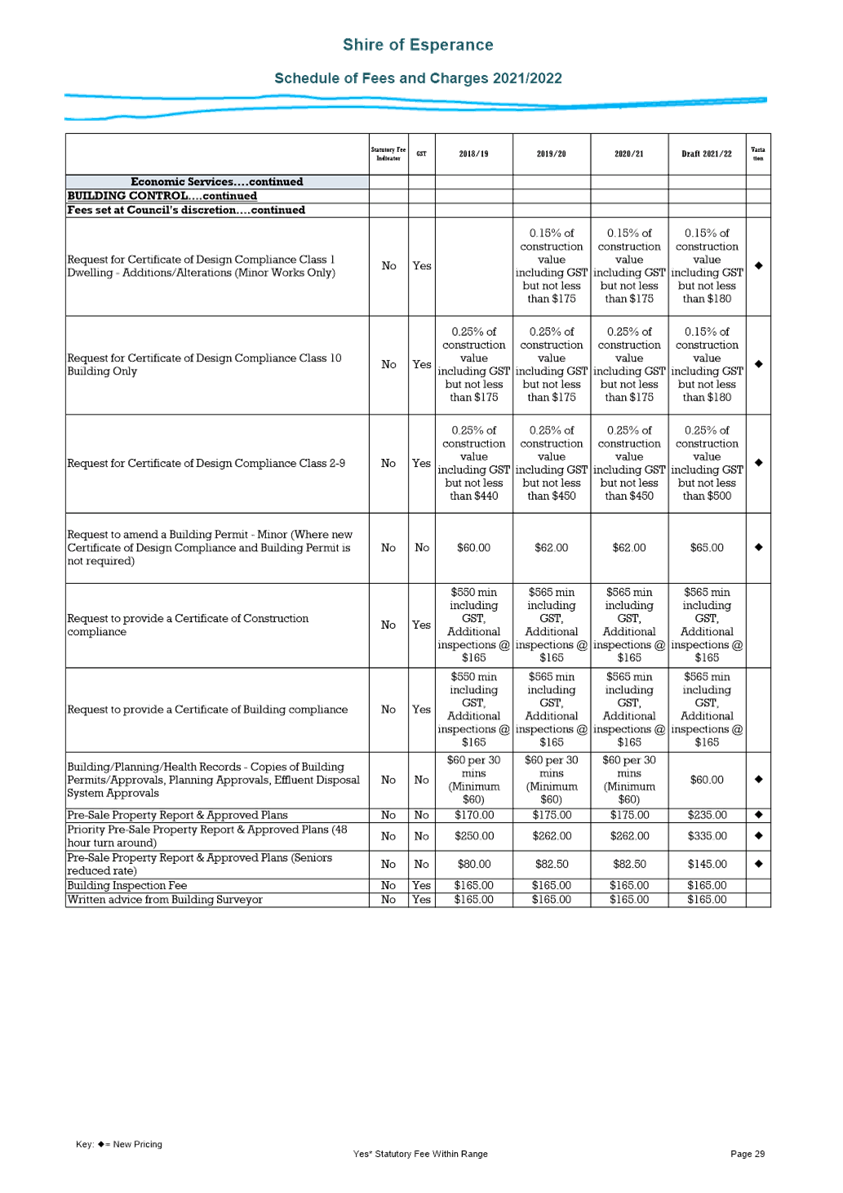

Local Government

(Financial Management) Regulation 34 (5) requires that each financial year a local

government adopts a percentage or value, calculated in accordance with AAS5

(Australian Accounting Standards), to be used in the monthly statement of

financial activity for reporting material variances. AAS5 provides

some guidance as to what may be regarded as a material amount when dealing with

the balance sheet, operating statement and statement of cash flow when it

states an amount which is equal to or greater than 10% of the base amount may

be considered to be material while an amount less than or equal to 5% may not

be material, unless in both cases there is a convincing argument to the

contrary.

On the basis of this guidance, historical reference

and having regard to the fact that the users of this financial information are

management and Council requiring assistance with making management decisions,

the 10% variance would be reasonable lower limit for highlighting material

variances, however this limit could be adjusted in the future if necessary. The

use of this limit also does not preclude reporting lesser variances if it is

considered their disclosure would be of benefit to the user of the monthly financial

report. The proposed material reporting variance is proposed to remain the same

as previous years.

Consultation

The budget is presented in accordance

with the directions provided by Council at the Draft Budget Workshops that were

held in late June based on the base of the 2020/21 Revised Budget.

Financial Implications

As presented within the budget document.

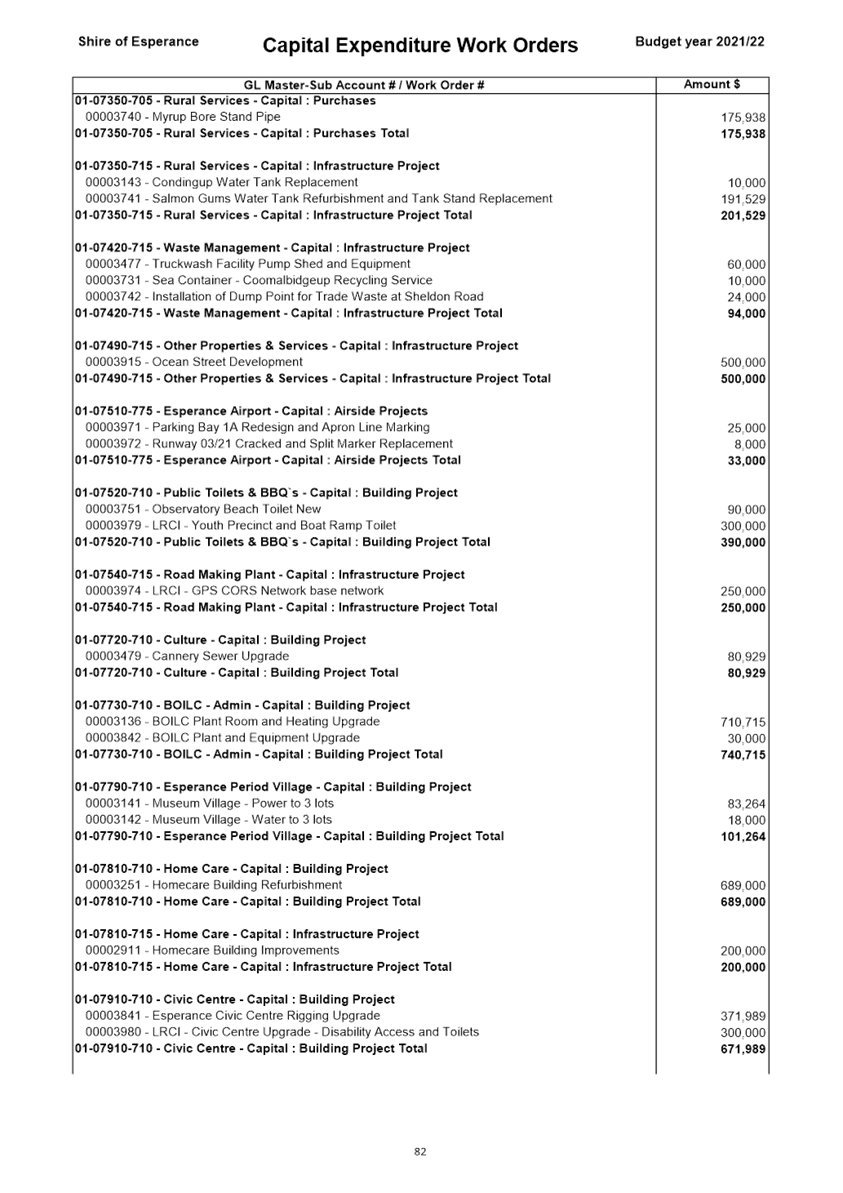

Asset Management Implications

A significant amount of the budget is directed towards

addressing asset management issues. A large road and infrastructure

construction program that totals $26.5m is predominantly focused on asset

renewal/improvements and improving road safety.

Statutory Implications

The statutory implications associated

with this item are the Local Government Act 1995 Section 6.2 and the Local

Government (Financial Management) Regulations 1996 Part 3 prescribes the

requirement of the annual budget.

As discussed with Council, a forecast

2% increase to salaries and wages has been included for staff within the

2021/22 year. Due to updates in federal superannuation legislation, a

further 0.5% increase from 9.5% to 10% has been included.

Determinations by the Salary and

Allowances Tribunal in relation to elected member allowances has also been

taken into account within the budget. The Councillors allowances have again

remained unchanged from the previous year for the 2021/22

budget.

Integrated planning and reporting documents such as the

Strategic Community Plan, Corporate Business Plan, Long Term Financial Plan,

Asset Management Plan and Workforce Plan have all been referenced and utilised

in the preparation of the 2021/22 budget.

Policy Implications

The policy implications arising from this report are is the

Enterprise Agreement 2019 (Amended) and a number of Council Policies that

relate to staff entitlements.

Strategic Implications

Strategic Community Plan 2017-2027

Community Leadership

L2- Provide responsible

resource and planning management for now and the future.

Corporate Business Plan

L2.6 - Manage Finance

Environmental Considerations

The budget has a number of items that deal with environmental

issues to either improve the environmental outcomes, seek approvals or reduce

the Shire’s risk with environmental issues.

Attachments

|

a⇩.

|

Statutory Budget 2021/22

|

|

|

Officer’s Recommendation

That Council

1. AUTHORISE,

by absolute majority, the income and expenditure contained within the

Municipal Fund Budget pursuant to the provisions of Section 6.2 of the Local

Government Act (1995) and Part 3 of the Local Government (Financial

Management) Regulations 1996 and adopt the Statutory Budget 2020/2021.

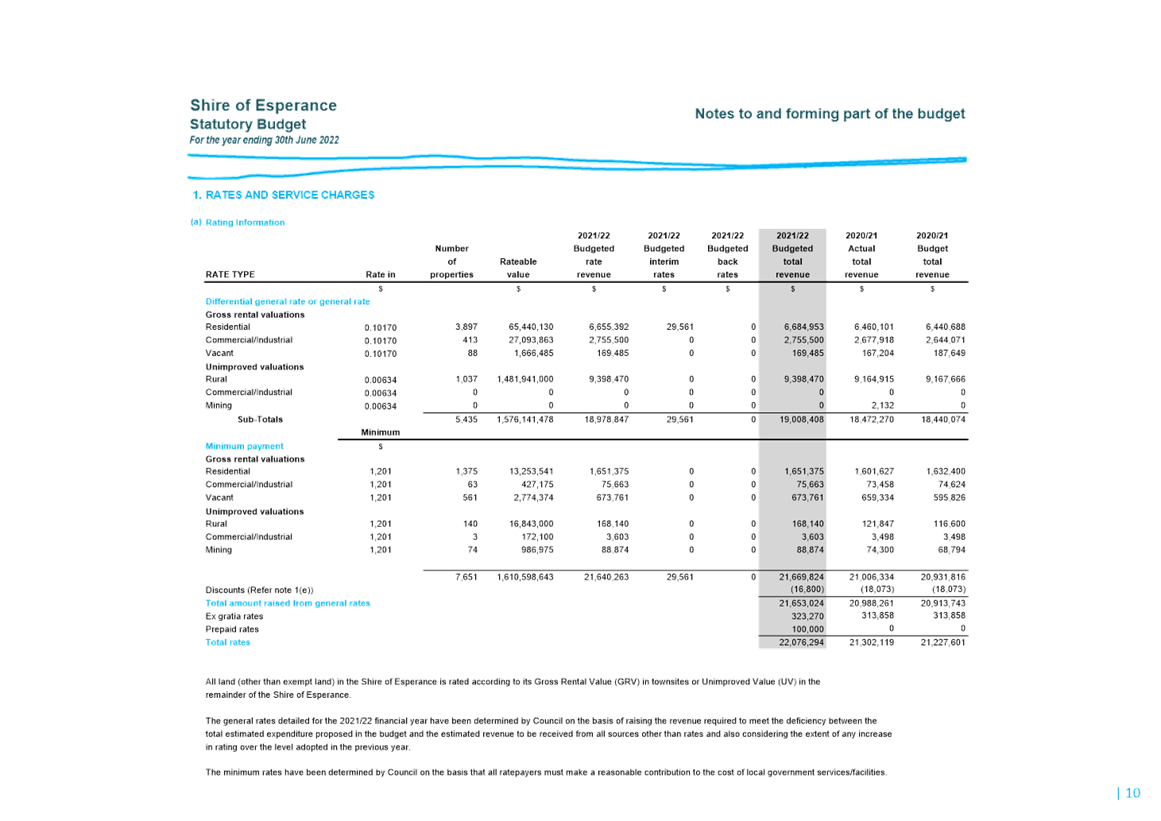

2. IMPOSE

for the purpose of yielding the deficiency disclosed by the Municipal Fund

Budget that Council pursuant to Sections 6.32 and 6.35 of the Local

Government Act (1995) the following general and minimum rates on Gross

Rental and Unimproved Values

General

Rates

Residential

(GRV) 10.170

rate in the dollar (cents)

Commercial

/ Industrial (GRV) 10.170

rate in the dollar (cents)

Vacant

Land (GRV) 10.170

rate in the dollar (cents)

Rural

(UV)

0.634 rate in the dollar (cents)

Commercial

/ Industrial (UV)

0.634 rate in the dollar (cents)

Mining

(UV)

0.634 rate in the dollar (cents)

Minimum

Rates

Residential

(GRV) $1,201.00

Commercial

/ Industrial (GRV) $1,201.00

Vacant Land

(GRV)

$1,201.00

Rural

(UV) $1,201.00

Commercial

/ Industrial (UV) $1,201.00

Mining

(UV) $1,201.00

3. IMPOSES,

by absolute majority, in accordance with section 6.51(1) of the Local Government

Act 1995 and clause 5 of the Local Government (COVID-19 Response) Amendment

Order 2021, gazetted on 2 June 2021, an interest rate of 7% applicable to

overdue and unpaid rate and service charges, subject to:

a. This

interest rate cannot be applied to an excluded person, as defined in the

Local Government (COVID-19 Response) Amendment Order 2021, gazetted on 2 June

2021, that has been determined by the Shire Of Esperance as suffering

financial hardship as a consequence of the COVID-19 pandemic.

4. IMPOSES,

in accordance with section 6.45(3) of the Local Government Act 1995 and

clause 6 of the Local Government (COVID-19 Response) Amendment Order 2021,

gazetted on 2 June 2021, , an interest rate of 2% applicable to rate and

service charge instalment arrangements, subject to:

a. This

interest rate cannot be applied to an excluded person, as defined in the

Local Government (COVID-19 Response) Amendment Order 2021, gazetted on 2 June

2021 that has been determined as suffering financial hardship as a consequence

of the COVID-19 pandemic in accordance with Council Policy COR 019 Financial

Hardship Policy.

5. That

for those ratepayers not paying by instalments, the penalty interest will

commence to be calculated no earlier than 35 days after the rates notice

issue date and after the rates due date.

6. Pursuant

to Section 6.45 of the Local Government Act (1995) and Regulation 64(2) of

the Local Government (Financial Management) Regulations 1996, Council

nominates the following due dates for the payment in full or by instalment:

Full

payment and 1st Instalment due date 29th

September 2021

2nd

Instalment due date 24th

November 2021

3rd

Instalment due date 19th

January 2022

4th

and final quarterly instalment due date 16th

March 2022

7. Pursuant

to Section 66 of the Waste Avoidance and Resource Recovery Act (2007),

Council adopt a Waste Rate of 0.000001 cents in the dollar for both GRV and

UV property categories, with a minimum of $80 for all GRV and UV rateable

properties.

8. Pursuant

to Section 67 of the Waste Avoidance and Resource Recovery Act (2007), and

section 6.16 of the Local Government Act 1995 Council adopts the

following charges for the removal and deposit of domestic and commercial

waste:

140ltr

bin waste collection

$173.00

240ltr

bin waste collection

$255.00

360ltr

bin waste collection

$357.00

140ltr

recycling collection- Domestic Fortnightly

$132.50

240ltr

recycling collection- Domestic Fortnightly

$170.00

240ltr

recycling collection- Commercial Fortnightly

$170.00

240ltr

recycling collection- Commercial Weekly

$315.00

360ltr

recycling collection- Domestic Fortnightly

$175.00

360ltr

recycling collection- Commercial Fortnightly

$225.00

360ltr

recycling collection- Commercial Weekly

$425.00

1100ltr

recycling collection- Commercial Weekly $1,405.00

Residential

and Commercial Premises

Additional

waste bin collection

(140,

240 & 360ltr bins) $31.00

Additional

recycling bin collection

(140,

240 & 360ltr bins) $31.00

Additional

recycling bin collection

(1100ltr

bin for Commercial only) $55.00

9. Every

rateable assessment be issued with 4 free, up to 1m³ domestic waste

vouchers.

10. Authorise

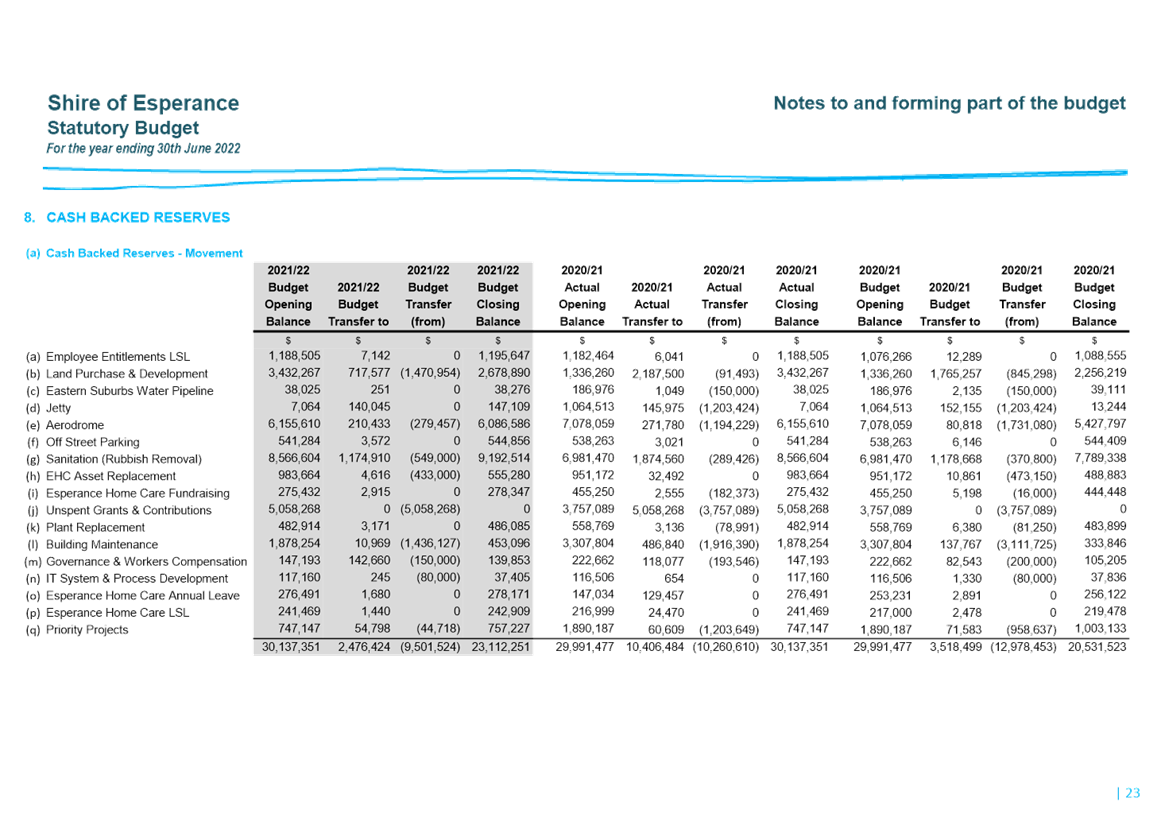

the transfers/movements to and from the Reserve Accounts, as detailed within

the Statutory Budget document.

11. Pursuant

to Section 6.20 of the Local Government Act (1995), approve the following

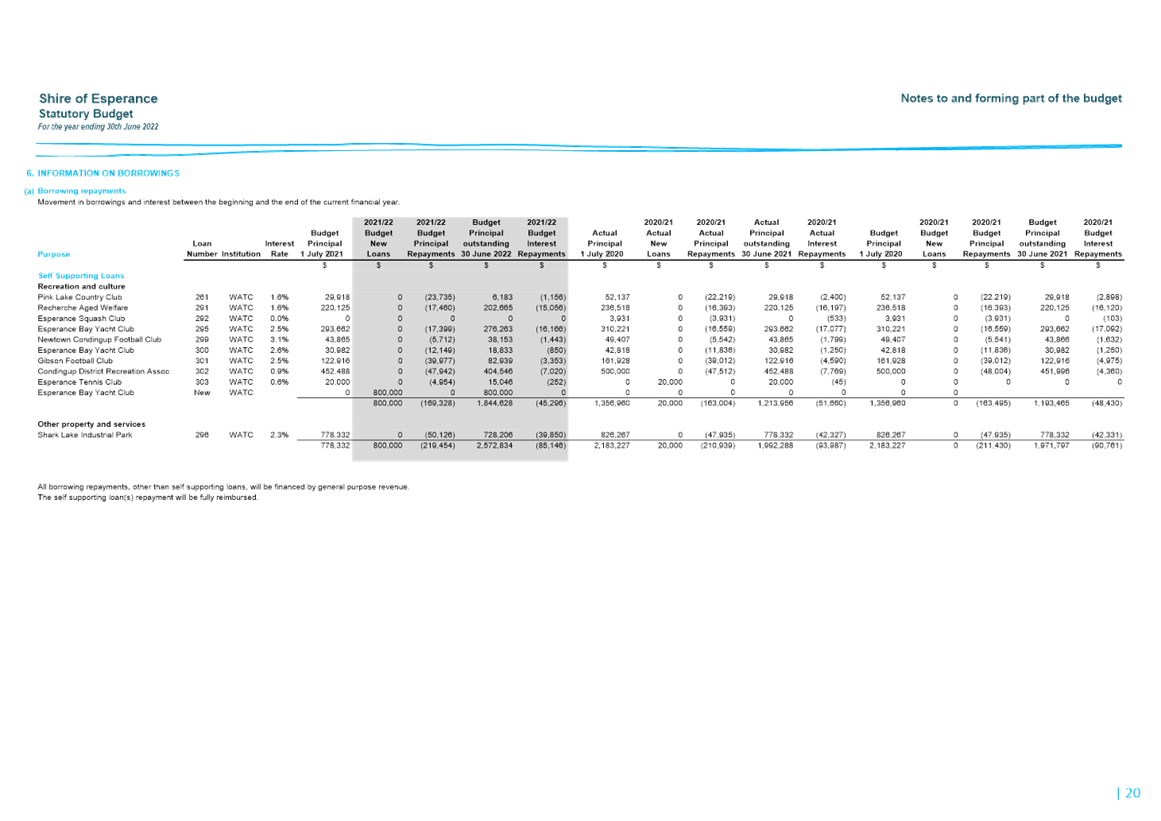

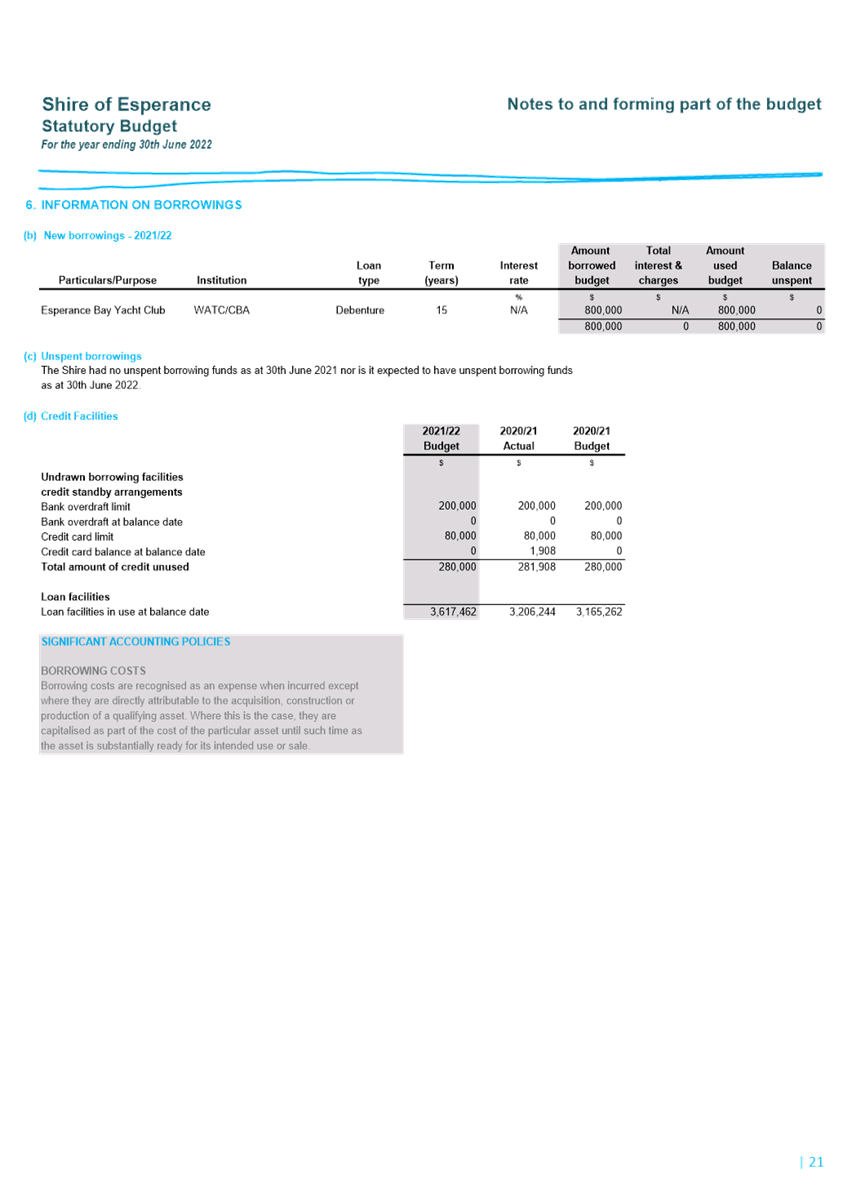

borrowings as per Note 6 (b) of the Statutory Budget for 2021/2022-

Esperance

Bay Yacht Club – Marina Upgrade $800,000

12. ADOPT,

pursuant to Section 6.16 of the Local Government Act (1995), the Fees and

Charges, as included in the Statutory Budget for the 2021/2022 year with all

fees and charges becoming effective immediately except those for the BOILC

which will become effective from 1 September 2021.

13. Pursuant to section 5.99 of the Local

Government Act 1995 and regulation 34 of the Local Government

(Administration) Regulations 1996, council adopts the following annual

fees for payment of elected members in lieu of individual meeting attendance

fees:

President $22,000

Councillors $18,000

Pursuant to

section 5.99A of the Local Government Act 1995 and regulations 34A and

34AA of the Local Government

(Administration) Regulations 1996, council adopts the following

annual allowances for elected members:

Telecommunications

Allowance $2,000

Pursuant to

section 5.98(5) of the Local Government Act 1995 and regulation 33 of

the Local Government

(Administration) Regulations 1996, council adopts the following annual

local government allowance to be paid in addition to the annual meeting allowance:

President $34,500

Pursuant to

section 5.98A of the Local Government Act 1995 and regulations 33A of the

Local Government (Administration) Regulations 1996, council adopts the

following annual local government allowance to be paid in

addition of the annual meeting allowance:

Deputy President $8,625

14. ADOPT,

for the 2021/22 financial year a variance in the Statement of Financial

Activity of $100,000 or 10% (whichever is lesser) for the reporting of

material variances between the year to date budget and year to date actual

information for disclosure purposes.

15. Allocate

an additional $25,000 towards the Ports Lighting Project, funded by a

transfer from the Priority Projects Reserve, to allow higher lighting towers

to be installed and agree that the Community Grant Allocation to the Ports

Football Club of $65,336 be no longer conditional on CSRFF

approval.

Voting Requirement Absolute Majority

|